This is the fourth post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome back to our introduction to U.S. equity market structure. Now that we’ve discussed the rules of the game, the playing field, and the “ball” (the stocks), let’s dive into how trading really happens by focusing on the key players: broker-dealers and investors.

Investors

Investors are the ultimate stakeholders in the market—the ones the SEC is designed to protect. Investors provide the capital that companies use to grow and fuel the economy. They can be individual investors, like people buying stocks or contributing to a 401(k), or institutional investors, like asset managers handling pension funds or mutual funds on behalf of individuals.

If you invest in a company or have a retirement account, you’re considered an investor. Approximately half of Americans are invested in the stock market in some form. Investors play a key role by researching companies, making decisions on whether to buy or sell, and holding stocks whose value fluctuates with market performance.

While investors are central to the market, they often can’t execute trades directly. When you place a trade on your brokerage account, you’re not submitting that order directly to the exchange. Instead, you rely on a registered broker-dealer to execute the trade on your behalf.

Broker-Dealers

In many ways, broker-dealers are the actual “players” on the field. These firms are licensed to buy and sell securities, playing both the role of agent (when trading on behalf of clients) and principal (when trading for their own account). Broker-dealers provide the crucial bridge between investors and the stock exchanges.

Broker (or agency broker) refers to firms or individuals that execute trades for clients.

Dealer (or principal trader) refers to those who trade on their own account.

Prime brokerage is a term for brokers that offer additional services like securities lending, leveraged trade executions, and cash management, which large investors often require.

Proprietary traders trade mostly for their own accounts, and they tend to have more flexibility because they don’t handle client orders. High-frequency traders (HFTs) are often proprietary traders.

Retail broker-dealers serve individual investors, helping them buy and sell stocks.

Responsibilities of Brokers

Brokers have certain responsibilities to their clients, particularly regarding “best execution” and “order routing.”

Best Execution Brokers are legally required to seek the best execution for their clients’ orders. This means they must strive to achieve the best price reasonably available at the time of the trade. At a minimum, this means they can’t execute an order at a price worse than what’s being displayed in the market elsewhere. However, brokers are also encouraged to seek “price improvement,” aiming for a price better than the current market quote if possible.

Order Routing When you place a trade, brokers must decide where to send your order for execution. This is called order routing. If you don’t specify where to route your trade, brokers have discretion over the decision. According to Rule 606 of Regulation NMS, brokers must report where they send orders that don’t have specific instructions. You can find these reports online by searching for a broker’s “606 report.”

Brokers balance different priorities depending on whether they represent themselves or their clients. The strategies and tactics they use will vary based on the instructions or goals of their clients.

In the next lesson, we’ll explore the strategies and tactics that broker-dealers use when trading in the U.S. equity market.

This is the third post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome back to our introductory course on U.S. equity markets. In our previous lessons, we talked about the rules and regulators of the game, as well as the playing field and referees—the trading venues. Now that we have the structure set up, it’s time to dig into what we mean when we say U.S. equities and what we’re actually trading—the ball in the game of trading.

As you know, when you buy stock in a company, you aren’t buying a concrete object. For example, if you buy a share in a pencil-making company, you can’t go to their factory and demand a bunch of pencils or one of their pencil-making machines. Instead, the stock represents an ownership stake in the company, giving you certain rights. For instance, if the company is sold, you generally get part of the purchase price, and you usually get a vote on certain decisions.

What Are U.S. Equities?

In general, when we talk about U.S. equities, we are referring to stocks that are registered with the SEC and listed on one of the U.S. stock exchanges. These stocks are publicly traded, meaning that pretty much anyone can go to their broker and buy a share. This is in contrast to private companies, which often sell shares to private investors, but those shares aren’t available to everyone.

There are also some public company stocks that trade only over-the-counter (OTC), usually because they are too small to qualify to list on one of the major exchanges. Those stocks are not considered part of the National Market System (NMS), so we’ll set them aside for now.

Most U.S. equities are often called single stocks, meaning they represent an ownership stake in a particular company. There are also equities called exchange-traded products (ETPs) that allow buyers to purchase a share in a set of stocks, often an index, rather than just one company. For instance, if you buy a share of an S&P 500 ETF (SPY), you are really buying fractions of each of the S&P 500 stocks.

Where Stocks Trade

We know from the previous lesson that stocks trade on exchanges and other trading venues. But one thing to keep in mind is that NMS stocks actually trade on all of these exchanges and usually across all other trading venues too. This is a result of Regulation NMS, which we discussed in the first lesson, the regulation that tied all of the exchanges together.

In many cases, people assume that stocks only or predominantly trade on the exchange where they are listed, and in fact, this was the case until a few decades ago. But today, during regular trading days, stocks can be traded across all different venues.

Listings Explained

If stocks can be traded across all of these trading venues, what does it mean to be “listed” on an exchange? Well, a company’s listing exchange has three main responsibilities.

First, the listing exchange handles a company’s auctions. The most high-profile auction for a company is usually its Initial Public Offering (IPO). Most companies become public through an IPO, which occurs when a private company decides it wants to become publicly traded. There are several advantages to being a publicly listed company: it allows owners to more easily sell their shares, making them more liquid, and it gives the company the option to sell more shares, raising capital that they can invest in the business. It also provides the company with a more liquid currency to acquire other companies or for mergers and acquisitions (M&A).

An IPO allows a company to become publicly traded and raise capital by selling new shares at the same time. In an IPO, the company offers a large number of new shares for sale through a group of brokers known as a syndicate. The night before the stock starts trading publicly, those shares are priced and sold to a set of large investors. The next morning, a big auction is held on the company’s listing exchange, and the company’s stock becomes available for trading moving forward. The listing exchange is responsible for the technology and rules to ensure that the auction is handled fairly and smoothly.

Recently, a few companies, including Spotify and Slack, opted to become public through what is called a “direct listing.” In a direct listing, the company still holds a big auction on its first day of trading, but the auction only includes existing shares that shareholders choose to sell, rather than new shares that the company makes available.

But the IPO auction isn’t the only one. Every weekday, there’s an opening auction (typically at 9:30 a.m. Eastern Time) and a closing auction (typically at 4:00 p.m. Eastern Time) for every stock. Before those auctions, brokers submit their orders to the listing exchange, detailing how many shares they want and what price they are willing to pay. The exchange gathers that information and, at the time of the auction, matches buyers and sellers at a single price that allows the most shares to be exchanged.

Second, the listing exchange is responsible for surveillance of its listed stocks. The exchange monitors trading in that stock and refers cases to regulators if there seems to be manipulative activity. The listing exchange can also halt trading in its listed stocks if needed and is in charge of disseminating important data, such as dividend information.

Lastly, the listing exchange provides services to companies to help them navigate the public market. This isn’t required by regulation, but it’s an expected practice in the industry. These services vary depending on the exchange’s particular strengths and the fees they charge for listing.

In our next episode, we’ll talk about who actually trades in the U.S. equity market and how investors and brokers operate.

This is the second post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Thanks for coming back for lesson two in our course on equity market structure. In our last lesson, we talked about the US equity market’s rulebook and the regulators—the laws, regulations, and regulators that govern the broad structures for trading. Today, we’re talking about the exchanges and other trading venues.

These entities, which are for-profit in the U.S., play two roles: trading venues act as the playing field and referees for trading. They have rules and technology that set up the basic boundaries for how they will match buyers and sellers. Their playing fields must be set up within the confines of the Exchange Act, but beyond that, they have some leeway with how trading works on their particular exchange.

For instance, IEX is known for its “speed bump”—a coil of cable that delays all messages coming in and out of the exchange by 350 microseconds. Trading venues are also responsible for monitoring trading on their venue for, among other things, potentially manipulative activity.

So, where are these entities that have so much power over how trading happens?

Stock Exchanges: Three Exchange Families Plus IEX

Stock exchanges are the main places where trading gets done. As of the recording of this lesson, there are 13 stock exchanges in the US, but that number makes it sound more complicated than it is. There are actually only four stock exchange operators currently in the market.

The New York Stock Exchange (NYSE) was the first US equities exchange. It still exists today and is often called “NYSE Classic” as shorthand. It’s the exchange that lists companies like GE and DuPont. However, NYSE also owns four other stock exchanges: NYSE Arca, which mainly lists ETFs, and three smaller exchanges with less than 1% market share: NYSE Chicago (the former Chicago Stock Exchange), NYSE American (the former American Stock Exchange), and NYSE National (the former Cincinnati Stock Exchange).

Next, there’s Nasdaq, which was founded in the 1970s as the first fully electronic stock market and became an exchange in 2006, ahead of Regulation NMS, which we discussed in the previous lesson. Nasdaq’s main exchange, just called Nasdaq, currently handles the most trading of any exchange and lists companies like Microsoft and Apple. Nasdaq also owns Nasdaq BX (the former Boston Stock Exchange) and Nasdaq PSX (the former Philadelphia Stock Exchange).

Then there’s Cboe Global Markets, the company that bought Bats Global Markets. Bats was founded in 2005 and started two exchanges. In 2014, it merged with Direct Edge, which also had two exchanges. Those four exchanges, which are now part of Cboe, are called Cboe BYX, Cboe BZX, Cboe EDGA, and Cboe EDGX.

Finally, there’s the Investors Exchange (IEX). IEX became an exchange in 2016 and is most well-known for the speed bump mentioned previously, which is designed to help the exchange ensure it has the most up-to-date prices from around the market before executing trades. IEX has also introduced other technology and business practices that are designed to level the playing field for all participants.

All the stock exchanges have applied for and received permission from the SEC to be what is called nationally registered stock exchanges. In this capacity, they are considered self-regulatory organizations (SROs) that have significant power to enforce the rules of their exchanges, acting as referees. However, with that power comes a large amount of scrutiny and regulatory oversight, aimed at ensuring that the exchanges operate with a high degree of integrity, security, and precision.

In addition to these exchanges, there are a number of other companies that may be launching exchanges in the near future, including the Long-Term Stock Exchange, the Members Exchange, and MIAX, which is known for operating multiple options exchanges. It’s a constantly evolving landscape and one that you can follow in the news regularly.

Alternative Trading Systems (ATS) – AKA Dark Pools

In addition to the stock exchanges, trading also occurs on Alternative Trading Systems (ATSs), often referred to as dark pools. These venues have the same fundamental rules but exhibit some critical differences. ATSs are more lightly regulated marketplaces for trading, often run by large banks. For instance, two of the largest dark pools are run by UBS and Morgan Stanley. However, some ATSs are run independently, such as Liquidnet.

ATSs are called dark pools because, in many cases, they only offer non-displayed trading, meaning buyers and sellers don’t publicly post or advertise the prices at which they would be willing to trade. Instead, they submit their orders to the dark pool and wait for another order to match with them. Non-displayed trading is also available on exchanges but tends to be more prevalent on ATSs.

Starting soon, dark pools will have to disclose the rules of how trading works on their venues publicly via a form called ATS-N. This is important because the way dark pools operate is more flexible than exchanges. For example, they can charge more for trading than exchanges. Additionally, after trades occur on dark pools, they are only reported publicly as occurring off-exchange and are not attributed to the specific dark pool where they occurred.

Internalization

Finally, trades can also be executed inside large brokerages, for example, by matching or internalizing two customers’ orders. Large banks often work with a lot of clients across various departments. If they receive one order to buy and one order to sell the same stock, they can match those orders internally rather than sending them to an exchange or dark pool. Brokers prefer this because they get two orders filled immediately without sharing any information with the broader market, and they don’t have to pay another entity to execute the trade.

Additionally, some brokers send orders to market-making firms (also known as wholesalers) who trade against the orders for their own accounts. This process is also referred to as internalization.

In the next lesson, we’ll talk about what is actually traded in the US equity markets: stocks.

This is the first post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome to Introduction to the US Equity Market Structure, presented by the Investors Exchange. In this course, we’ll be providing an overview of how the US equities landscape is structured in order to give you an understanding of how your orders end up being executed in the market.

The image some people have in their minds of a trading floor with humans shouting orders no longer reflects how trading actually works. Our aim is for you to better understand the reality of the US equities market so you can make informed decisions about how you trade.

In this course, we compare the equity markets to a sport, with rules, referees, a playing field, a ball, and players on the field. While it’s not a perfect analogy, it’s a good way to understand many of the dynamics in the market. We hope that this approach will be helpful for you and encourage you to reach out to IEX with your comments and questions after you finish the course. In the meantime, put on your cap, lace up your cleats, and join us on the field.

The most important part of understanding any sport is, of course, the rules. What’s the goal of the game? What’s allowed? And how are the rules enforced?

The Purpose of the Stock Market: The Exchange Act of 1934

The oldest stock exchange in the US, the Philadelphia Stock Exchange, was founded in 1790, followed by a number of other regional exchanges. However, the foundation of our modern US equity market, the way it looks today, was really laid out in a key piece of legislation that came out of the public crisis of faith in the public markets following the stock market crash of 1929: the Exchange Act of 1934.

The Exchange Act of 1934 created the Securities and Exchange Commission, known as the SEC, and regulates the trading of stocks and bonds. In creating the SEC, the Exchange Act gave it broad authority over the securities industry. It is because of this law that the SEC can make rules that govern how brokers, exchanges, and other entities can operate and enforce those rules. It also outlines certain trading activities, like insider trading, as illegal, and established the practice of regular corporate reporting.

This ensures that when investors buy stock in a business, they know that every quarter, they will get an update on the business, which they can then use to make an informed decision on whether they want to continue to own that stock moving forward. It’s like a rule in a sport saying that everyone has to be able to see where the ball is—no one can be forced to wear a blindfold.

The Exchange Act also established the role of stock exchanges, which are known as self-regulatory organizations. We’ll talk more about the exchanges in the next lesson, but what the Exchange Act says about exchanges reveals a lot about the playing field they were putting in place. The Act says the rules of the exchange are designed to prevent fraudulent and manipulative acts and practices, to promote just and equitable principles of trade, to foster cooperation and coordination with persons engaged in regulating, clearing, settling, processing information with respect to, and facilitating transactions in securities, to remove impediments to and perfect the mechanism of a free and open market and a national market system, and in general, to protect investors and the public interest.

The Regulators: SEC and FINRA

We’ve talked a bit about the SEC already through the lens of the Exchange Act of 1934, but what does it really mean that the SEC regulates the securities industry? The SEC is the governing body of the securities space. Their mission is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.

In that capacity, the SEC has the power to make new rules about how trading works, just like an organization like the International Football Association Board can make adjustments to the rules of soccer. For instance, as technology has changed how people trade, the SEC has updated its rules to account for things like computer-based trading.

The SEC also has an enforcement division that brings civil enforcement actions against companies and individuals who violate securities laws. In this capacity, the SEC is like the NBA commissioner who has the power to hand down disciplinary actions to players who break the rules of the game.

The Financial Industry Regulatory Authority, known as FINRA, is an independent nonprofit authorized by Congress to protect investors. It’s not part of the government, but like the exchanges, it’s a self-regulatory organization that has delegated authority. FINRA is focused specifically on the broker-dealer industry and has the power to write and enforce rules that brokers have to follow, examining firms for compliance with those rules and disciplining firms that have violated the rules.

The Regulatory Landscape: Reg NMS, Order Protection Rule, Access Rule, Penny Rule, Market Data Rules

While many aspects of the trading landscape have stayed the same over the years, trading today obviously looks very different than it did 50 years ago. Like virtually all aspects of our lives, trading has been massively changed by the development of technology, and regulation has had to change with it.

The most influential regulation that has shifted the way trading works today is a 2005 consolidation of earlier legislation known as Regulation National Market System (Reg NMS). You can think of this regulation and its impact as similar to when the designated hitter rule was adopted by the American League in baseball in 1973, or when the 24-second shot clock was introduced in basketball.

The period before the institution of Reg NMS was a time of tremendous change for the market. The market had transitioned from being dominated by the New York Stock Exchange to being extremely fragmented, with stocks trading at different prices with no central source of truth. Reg NMS set out to stitch the market together into one national market system. In doing so, it made several changes that have forever altered the dynamics of trading.

First, the Order Protection Rule. This rule requires that you can’t trade at a worse price if a better price is available and accessible in the market. So, if you’re buying a stock and it’s available for $9.99 on one exchange, you can’t buy it for $10 on a different exchange. It’s like an “out of bounds” play.

Second, the Access Rule. The Access Rule ensured that different trading venues were connected to each other and lowered the prices they could charge for trading to make sure people could access them. This rule aimed to prevent gaming of the Order Protection Rule by putting a cap on prices. It ensures that an exchange can’t charge a ridiculous amount to trade and then require that you pay it just because they have the best price.

Next, the Sub-Penny Rule. This rule set the minimum price increment for a stock at one cent for stocks priced over one dollar. This is why you’ll never see a stock for sale at the kinds of prices you see at gas stations, like $3.5999.

Finally, the Market Data Rules. These rules created advisory committees populated by the exchanges that determine how exchanges distribute market data and provided a new mechanism for how they could be paid for this work.

Since 2005, these rules have been applied and interpreted in many ways. We’ll see their impact throughout the rest of this course. In the next lesson, we’ll dig further into the stock exchanges and how they both establish the playing fields for trading and act as its immediate referees.

The three financial statements – balance sheet, income statement, and cash flow statement – reflect two perspectives. The first perspective is what the cash flow statement reflects, which is whether a company can sustain its business in the future, or its risk. The second perspective is what the combination of balance sheet and income statement represent: if the company can sustain its business, what the business will look like. In other words, it is the perspective of returns.

In our previous discussions of the paper manufacturers, we were actually assuming there were no operational risks, meaning that we assumed that these companies had no survival risks. However, we know that this is not true in the real world, so we will discuss the analysis of cash flow statement and learn how to understand the information on cash flow statement.

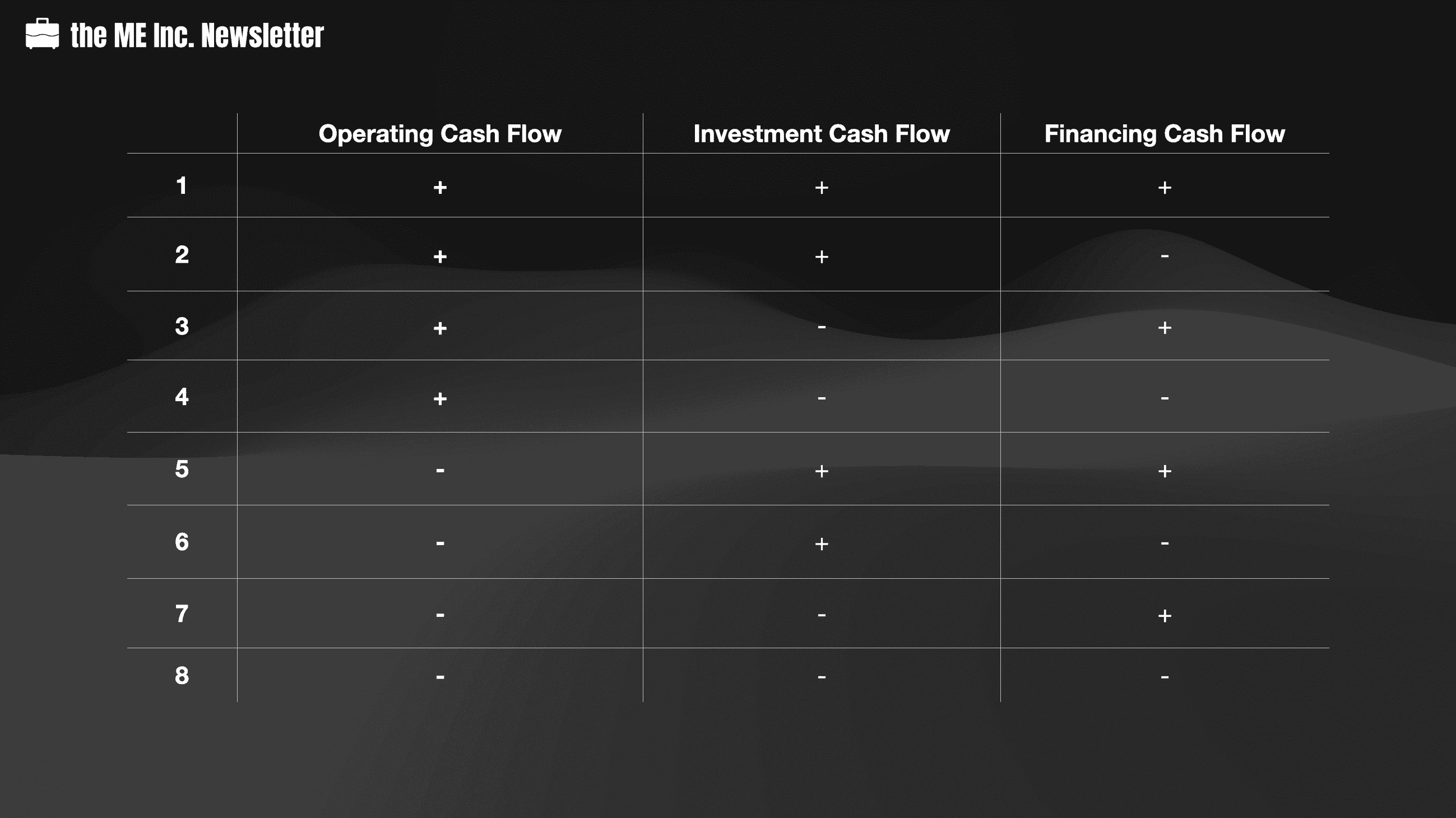

First of all, let’s recall what cash flow statement looks like. As we said, the cash flow statement describes the flow of cash. It is related to three types of activities of a company, or operation, investment, and financing. Under these three types of activities, the statement describes the inflow and outflow of cash. We have covered the detailed concepts of each type of cash flow in a previous episode which can be found here.

For the cash flow statement, the ultimate net cash flow is the total cash inflow minus the total cash outflow.

This table illustrates the possible combinations of a company’s net cash flows for each type of economic activity.

Recall that the reason we want to understand the detailed changes for each type of economic activity is that the final net cash flow of the company is not that important; after all, we can get the same number from the balance sheet alone, i.e. by looking at the cash balance difference between last year and this year. In short, we want to understand the reason for a company’s cash outflow and inflow. So let’s discuss how to interpret components in the cash flow statement.

For each type of cash flow, the net result could either be a net inflow or a net outflow. A net inflow is represented by a plus sign, while a net outflow is represented by a minus sign. All possible combinations are documented in the table above. Now let’s discuss them one by one (not necessarily from the first to the last).

Let’s first look at the second combination. What does a company that has a positive operating cash flow, a positive investment cash flow, and a negative financing cash flow look like?

+ Operating Cash Flow

Having a positive operating cash flow means the money earned from selling products is enough to cover for its procurement, wages and taxes, etc. In other words, the company’s operating activities are self-sufficient, or itcan generate blood for itself.

+ Investment Cash Flow

We see the cash flow of investment of the company is positive. What this means is that the company has net cash inflow from investment.

A company may generate positive investment cash flow from disposal of asset or cash from returns of investment. Generally speaking, it is more likely that such cash comes from returns of investment, considering that the operating activities of the company is also generating positive cash flow itself, so it should not need to dispose of its assets.

– Financing Cash Flow

The company’s financing activities are generating negative cash flow for the reason that the company may be paying back money to banks, or paying dividends to shareholders.

Summary

In short, the company’s cash flow is healthy and normal. The company’s operating activities are quite healthy. Its investment has made some returns, and this company spends some money on paying loans to banks or paying dividends to shareholders. The company might be in a mature stage.

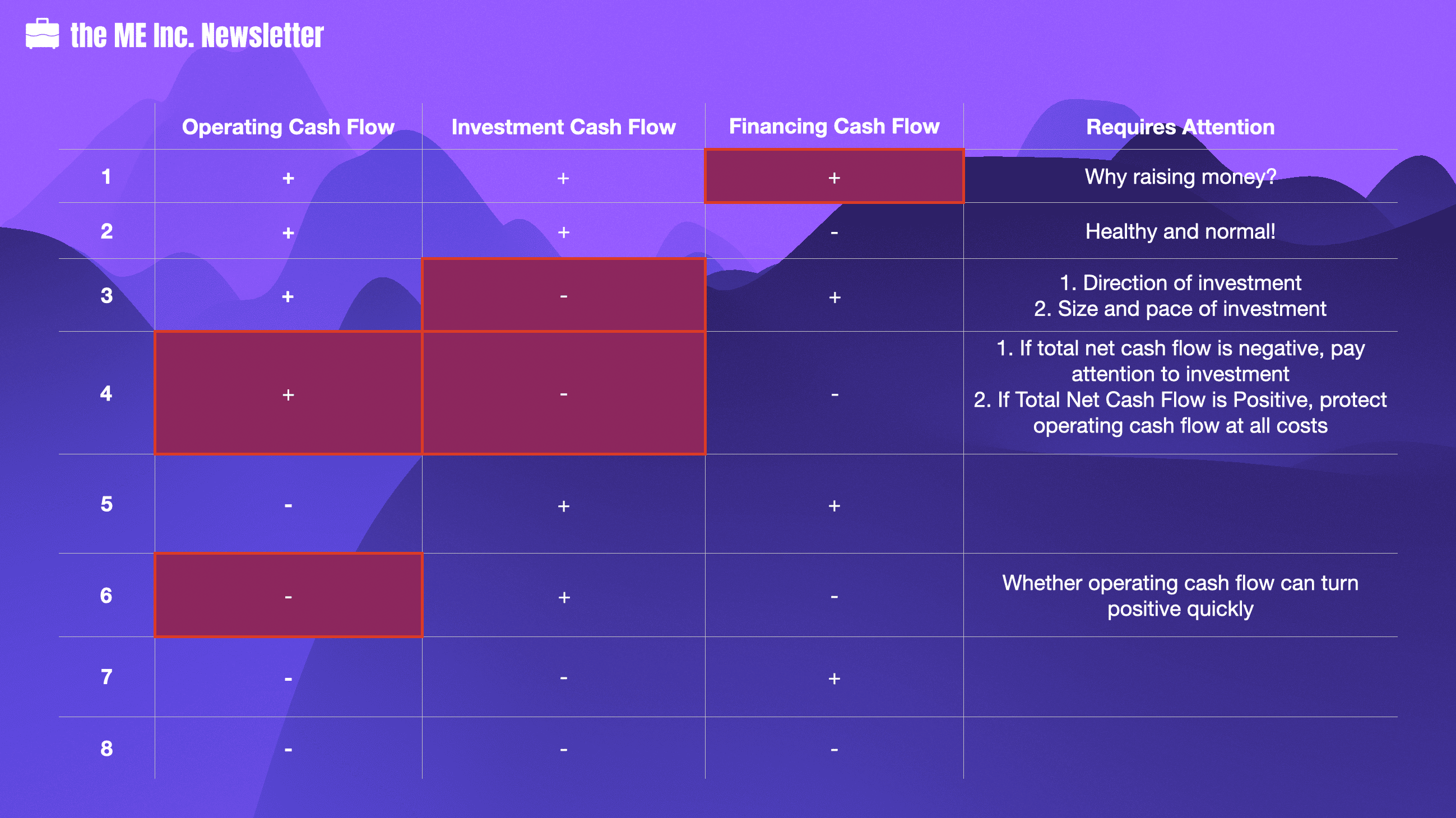

The only difference between the first and the second combination is that the first combination has a positive financing cash flow.

What this means is that the company is taking in financing money, or raising money.

Why should a mature, healthy company with normal operations be raising money? And where could the company spend such money?

One possibility is that the company plans to invest in a certain area, so it needs money. But if we look at this company, the company actually has a positive investment cash flow. What it means is that at least at this stage, the company hasn’t made large-scale investments, which will cause large cash outflows. As soon as the company starts to make such large investments, its investment cash flow will turn from positive to negative, which is represented in the third combination.

But what if the company has no such investment plans? Why should such a mature company be financing? If it doesn’t have a big plan of investment, there is no reason that it should need more money.

In reality, however, companies do raise money even when they don’t have investment plans. The reason could be multifaceted. For example, in China private companies’ financing methods are quite limited. So when a company is running smoothly and has enough money, it actually is in a better position to get loans from banks. The company will seize such opportunity to secure as much loans from the banks as possible, since such opportunity is hard to encounter. Of course, we cannot rule out the possibility that some companies have bad motives when raising money without specific investment options. For example, it may want to transfer such money to some affiliated companies.

Overall, a company with positive cash flows in all three types of economic activities requires more attention. We should at least ask the purpose of it financing, and how the company expects such financing to impact the future of the company. Regardless of whether the company is raising money because its financing channels are limited, or because it has ill reasons, such financing activity will dilute the profitability of the company.

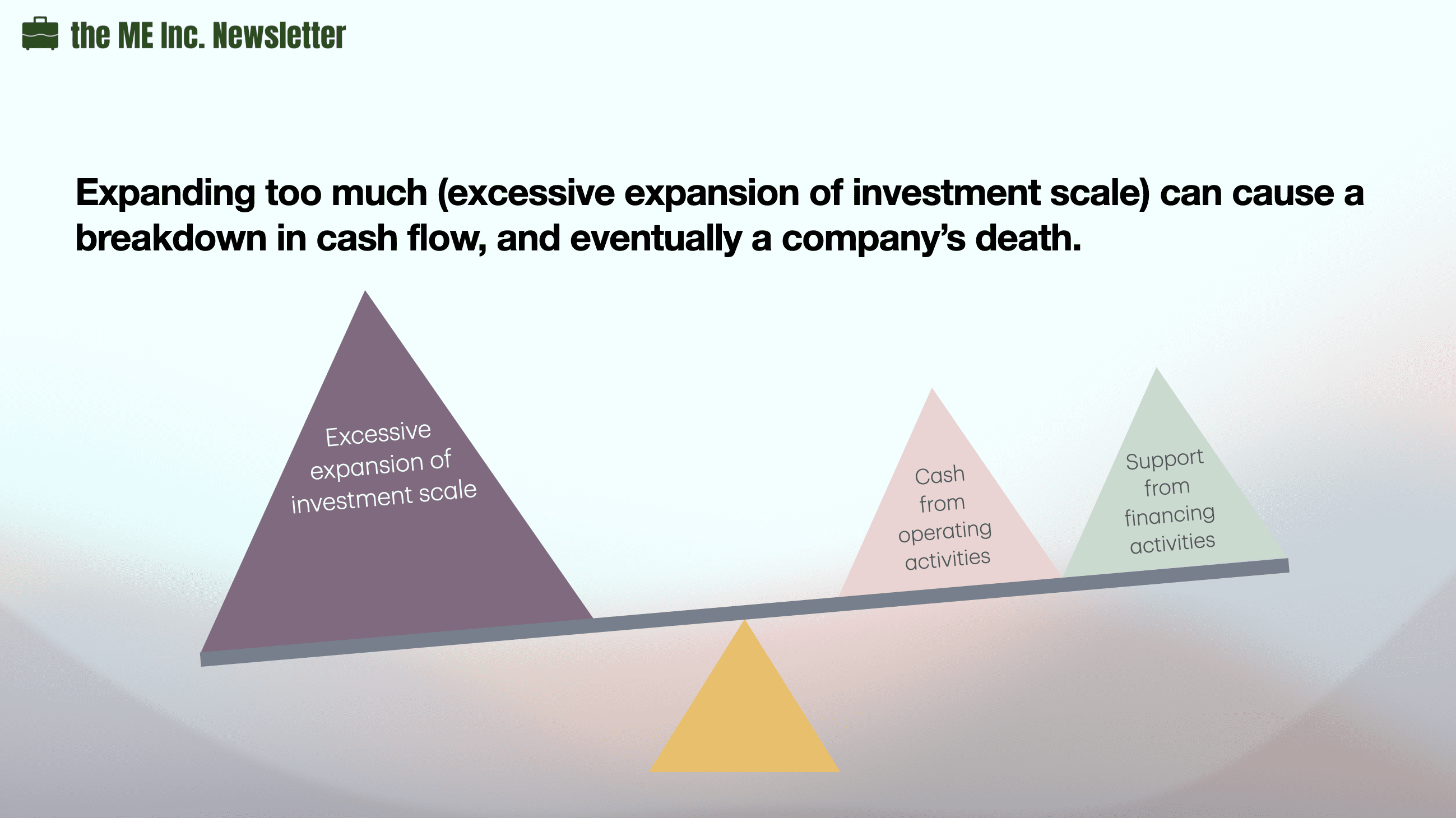

Like we said, the company with the 1st combination of cash flows could soon become one with the third after it executes on its investment plan. The company’s operating activities are completely self-sufficient; at the same time, it needs more money for investment.

What do you think is the biggest concern of this company?

Investment. Why?

Well this company is likely using money from operating and financing activities for investment. The success of investment could literally make or break this company. There have been numerous cases where a healthy and successful company goes into bankruptcy because of just one investment failure.

The first thing off the top of our minds is when a company decides to invest in unrelated businesses, fails, and never recovers from such failure. However, even when a company stays in its main business and invest, the success of investments is no guarantee. For instance, there was a very famous company in the instant noodle business. This company created the concept of non-fried instant noodles, which are thought of as more healthy. Because of such a healthy concept, the company quickly became one of the five largest instant noodle makers in China.

To maintain such level of success, the company began to invest heavily in production capacity expansions. Its investment was made in its main business, not diversified lines of businesses. Considering that its main business is going so well, such investment can actually be considered as low-risk.

However, the final result was pretty sad. When the company went bankrupt because of a breakdown of cash flow, there was only 3,000 CNY in its bank account. Apparently the company’s cash flow completely broke down. How could such a situation happen?

As a matter of fact, even when the company went bankrupt, its main line of business was still doing quite well. Its market share was well maintained, and the accounts receivable were still being collected. Then why does such a company end up like this?

The reason is quite simple. The company expanded too fast by putting too much cash into investments. We know that investments will take time before they can generate returns. Before that, there is only cash outflow. Such cash outflow relies on cash flow from its own operating activities and its financing capability. If its investment expands too fast, it may lead to a situation where both operating and financing cannot generate enough cash to support such investment. The rapid outflow of cash could lead to a shortage of cash, and even drive an otherwise promising company into bankruptcy.

Therefore for a company with positive operating cash flow, negative investment cash flow, and positive financing cash flow, we should pay special attention to the company’s risk of investment. Such risk not only lies in the direction of investment, but also in how to effectively control the size and pace of the investment so that the company’s cash reserve can be kept within a reasonable range.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.

There is only one combination between the 4th and the 3rd combination, which is that this combination has a negative financing cash flow. In this case, the company is still paying back money.

Compared to a company with the 3rd type of cash flow, do you think this company has a higher or lower risk?

Well, it could go either way. It might have a higher risk because it has more areas to invest, in addition to paying back dividends or loan interests. It might have a lower risk, considering that it is already controling its leverage by paying back interests.

However, let’s think from the aspect of net cash flow.

If Total Net Cash Flow is Negative, Pay Attention to Investment

If at this moment, the company has a negative net cash flow, it means its cash is decreasing. Because an othewise healthy company can be driven to the edge of bankruptcy by cash flow breakdown, we should pay special attention to whether the company’s investments are growing too large too fast.

If Total Net Cash Flow is Positive, It’s All Good…(for the time being)

If its current net cash flow is positive, it means that the risk is kept within controllable range. Because cash flow from operating activities is the most reliable and stable source of cash, we rely on operating activities to support its investment and financing activities. And since there is extra cash, this company has the means to keep its risk under control.

But is operating activity reliable and stable forever? Well, not necessarily.

In 2008, China’s real estate market experienced such a change. In 2007, the whole market was booming, as the housing prices increased significantly. Despite the soaring price, there was still huge demand, and whenever a new apartment came onto market for sale, it sold out instantaneously.

In 2008, the real estate market suddenly cooled down after the global financial crisis happened. The whole process lasted for less than one and a half year. During this time, most real estate companies experienced slow sales, so their operating activities were negatively affected. The worst case scenario is that cash flow from the operating activities would become negative, and once they do, situations 1, 2, 3, and 4 will become situations 5, 6, 7, and 8.

Obviously, it is the last situation, where a company has a negative cash flow for all three types of economic activities. A company in such a situation will have only outflows of cash. If nothing changes, the company will eventually run out of money and go bankrupt.

A company with this combination of cash flow actually evolves from the 4th situation, where only operating cash flow was positive.

We mentioned that if the company with all negative cash flow in three types of economic activities doesn’t change anything, its cash will eventually run out and the company will be closed. But what kind of changes can it make?

The first option is to turn cash flow of operating activities to positive, or come back to the 4th Combination of cash flow.

The second option is to turn cash flow of investment activities to positive, or the 6th Combination of cash flow.

The third option is to turn the cash flow of financing activities to positive, or the 7th Combination of cash flow.

However, we know the 6th combination is hard to achieve. What this option shows is that even though I’m still making investments, these investments can quickly generate returns, which is a feat very difficult to achieve. A plausible way to achieve this is to sell these investments, which is the last outcome we want to see unless there are no other options.

From 8th to 4th: Turning Operating Cash Flow Positive Again

Then can we go from the 8th to the 4th option, i.e. at least turning our operating cash flow into positive?

Let’s revisit the real estate market downturn in China during the global financial crisis around 2008. During that time, many real estate companies started to heavily discount the houses they built, sometimes to as high as 30% off. The reason is that these companies wanted to collect cash as fast as possible in order to counter their shortage of cash, even at the cost of profitability. But it was only with such drastic discount methods that some real estate companies were able to turn their operating cash flow back to positive, saving them from bankruptcy.

Now that the company has managed to get out of the all negative cash flow situation and at least managed to return to a positive operating cash flow, its operating activities have become the main source of risk. Though we mentioned that its investment activities would still need to be monitored so investments wouldn’t grow too big too fast, the company should definitely protect its operating cash flow at all costs, as this is the only healthy cash flow it has. Without it, the financial situation of the company will soon enter into a downward spiral.

From 8th to 7th: Turning Financing Cash Flow Positive Again

How can it change to situation 7? To do this, we need to finance.

But during that period of time, the Chinese government launched a policy aiming at cooling down the real estate market, preventing banks from giving out loans to real estate companies for development. What this means is that if a real estate company wants to develop a new project, it won’t be able to secure any loans from the banks during that time.

To make matters worse, the China Securities Regulatory Commission also set forth a regulation preventing all real estate companies from going public during a specific period of time. Real estate companies lost all financing channels, either from equity of from debt.

To survive, some real estate companies started to borrow money from non-bank financial institutions such as some trust companies at much higher interest rates. This just shows how desperate some real estate companies were at the time, doing anything they can just to survive, even bearing the extra cost of capital. Of course, this ordeal didn’t last long, and after one year the real estate market became hot again. Although some companies went bankrupt, most of the companies overcame the difficulties after putting in all the efforts. However, we can easily imagine an otherwise different outcome; if the period dragged longer, many companies would need to start selling off their investments. If even after selling off investments, the companies still were unable to come up with enough cash, some might resort to bankruptcy.

As a matter of fact, in 2024 we indeed saw this happen, albeit 15 years later. Most real estate companies have encountered financial troubles, from Evergrande, Vanke, Wanda, Shimao, just to name a few. Evergrande has entered the bankruptcy process.

One major difference between 1 to 4 and 5 to 8 is that the first four combinations have positive operating cash flows. For companies with negative operating cash flows, what do you think would be the stage of lifecycle these companies are in?

Generally speaking, companies in the startup stage are more likely to have a negative operating cash flow. As these startups are still developing products and looking for product market fit, they are more likely to spend more than they make. Another possible scenario is when the market enters into recession. During this period of time, competition becomes so fierce that products just don’t sell.

Let’s first look at startups.

If a startup’s cash flow from operating activities is negative, how about its cash flow from investment? We all know that a start-up company needs to keep investing to grow bigger. After a startup makes investments, its investment cash flow should become negative.

If its cash flows from operating and investment are both negative, how can the company survive? Apparently, it needs financing, i.e. its financing cash flow is positive. This means a startup company normally has the seventh type of cash flow.

A company with this type of cash flow combination is likely one that has earned a large sum of money in the past and has a large cash position. Even though this company’s operating activities are not generating positive cash flows, the company’s past investments are generating positive cash flow, and it can consistently bring in money from the financial market. This company has a strong capacity in mobilizing capital from the financial market.

There are normally two possibilities for companies with this type of cash flow combination. The first possibility is that this company has a good investment project that is generating cash flow. In fact this project is so lucrative that it has enough returns to carry the company. Another possibility, rather an unfortunate one, is that the company is selling off projects. A company facing the second possibility is running out of cash and will likely close doors soon.

We can see that this situation rarely happens.

For this type of company, the key point is whether the company’s operating cash flow can become positive in a short time. When its operating cash flow becomes positive, the 6th combination will become the 2nd.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.