These are all the economic activities that have occurred from the establishment of the company, to the end of its first year of business operations. All activities are related to the increase or decrease of the company’s cash positions.

Next we are going to define each activity as operating activity, investment activity, or financing activity, and mark it as either inflow or outflow.

Cash Flow Item Categorization

Shareholder investment: shareholders invested 32 million dollars to establish the company. This is a financing activity which caused an increase in cash, so it is a cash inflow from financing activity.

Bank loan: the company then borrowed 51 million dolloars from the bank. This is also a financing activity, albeit a debt financing activity, which caused the cash inflows as well. So it is also a cash inflow from financing activity.

Fixed asset procurement: the company then spent 57 million to purchase fixed assets like buildings, equipments and so on. Since fixed assets can have long-term economic impact on the company, this economic activity belongs to the investing category. And since the company is spending money to procure such fixed assets, it should be a cash outflow from investing activity.

Land usage rights procurement: the company then paid 1.5 million for the right to use the land for a period of time. We know that the acquisition of land usage rights is an intangible asset, and it does not belong to our daily operations. So it is also a cash outflow from investing activity.

Raw material procurement: this activitiy belongs to daily operations, and it causes a decrease in cash, so it is a cash outflow from operating activity.

Manufacturing expenses: the company needs to hire staff and put the fixed assets – plant and quipment – to work in order to produce final products. This caused another 8 million dollars of cash decrease. (Recall that we didn’t have enough cash to pay our fees and our electricity company generously granted us a six-month grace period, pushing the payment term to the next year.) This economic activity is a cash outflow from operating activity.

Sales of products: the company then makes its first sales from all the products it produced. This is a cash inflow from operating activity.

Prepayment for raw materials: the company then pays 1.5 million to buy raw materials for the next year. Since the company is paying money out for raw materials, this economic activity is a cash outflow from operating activity.

Expenses: the company paid 4 million for various types of expenses, including the salary of sales personnel, expense of sales department, salary of management personnel, and expense for management, etc. All of these belong to the daily operation of the company. This is still a cash outflow from operating activities.

R&D: research and development can often be confused as an investment into intangible assets, but because of the conservative nature of accountants and the highly uncertain and risky nature of R&D activities, it is actually considered management expenses. As a result, R&D is a cash outflow from operating activity (NOT investing activity).

Interest payment to bank loans: at the very beginning we have secured a loan from the bank, which has interests. Our company is then liable to pay 1.3 million dollars of interest to the bank. This is obviously a cash outflow from financing activities.

Income tax: the company still makes profits after deducting all costs, expenses and interests. Since paying such income tax is an activity happening in the process of operations, it should be a cash outflow from operating activities.

Profit distribution: the company then allocates 1 million profits to the shareholder and keeps the other 4.2 million in the company. This is money flowing out of the company from its bank account to the shareholder’s bank account, so it is a cash outflow from financing activities.

The 13 economic activities showed us how cash goes in and out of our company, making this table essentially our cash flow statement. Now let’s take a look at the final result by further digging one step deep.

Further Analysis

Net Cash Flow from Financing Activities: the company was created by the shareholder’s initial investment o 32 million dollars, and it further borrowed 51 million dollars from the bank. Even though it paid some interests (1.3 million) and dividends (1 million) to the above two parties, the company still nets 80.7 million dollars from such financing activities as cash inflow.

Net Cash Flow from Investing Activities: the company has a negative 58.5 million dollars of investment,meaning that the company has made investment of this amount. If this number is positive, it means that the company has generated positive returns from its investments. To emphasize, investing activities can not only mean investment outside of the company, but also inside the company, such as investment in fixed assets and equipment, etc.

Net Cash Flow from Operating Activities: finally what is the net cash flow of its operating activities? After putting all the numbers together, we get a nagative 1 million dollars. Somebody might say that the company has netted losses in its operating activities, but we all know that the company actually made a net profit of 5.2 million dollars and distributed 1 million to the shareholders. So the company actually didn’t lose money.

Then what actually happened here from operating activities? The company made money only from its sales and spent money everywhere, from raw material purchases, operating expenses, to R&D, etc. The fact that the net cash flow from operating activities is negative means the money it generates from sales is insufficient to cover all the raw material costs, staff salaries, and taxes, etc. In other words, the company cannot make ends meet and it needs to find cash from other places.

That other place for our company is financing. Without financing activities, the company will not have enough money to support its operating and investing activities, both of which netted negative cash flows.

Does the company “have money”?

Before we answer this, we should all agree that the company “makes money” – after all, it has generated 5.2 million dollars of net profit in its first year of operations.

However, can we come to the conclusion that it “has money“?

Considering that it has a negative net cash flow from operating activities, we cannot arrive at this conclusion. The company actually relies on financing to sustain its operations.

How is it possible that a profitable company doesn’t have money?

In fact, this is entirely possible. It actually is also possible for a company to have money and not make money, i.e. making a profit, at the same time, making the situation all more confusing.

Making Money or Having Money: which would you rather be?

We can probably all agree that a company that makes money and has money is in the best situation. We can also agree that a company that doesn’t make money and has no money is in the worst situation. But if you had to choose between making money and having money, which situation would you rather be in?

For this question, different people have different ideas. You might say earning money is more important, because a company’s purpose is to make a profit. But you might say that having money is more important, since a company cannot survive without sufficient cash in the bank. Let’s leave this question for now and we will revisit when we have acquired more knowledge in the future.

Let’s go back to our company. The cash flow for its financing activities, investing activities, and operating activities are 80.7 million, -58.5 million, and -1 million respectively. We can easily get its net cash flow by adding the above three, making it 21.2 million dollars.

The number might be familiar to us because it has appeared somewhere else; in fact, this is our final cash position after one year operation of the business!

How does this “coincidence” happen?

Well there is actually no coincidence. If you recall, we actually covered that the net cash flow can be calculated from subtracting this year’s cash by last year’s cash. However, since our company was just established, the difference between the two is actually this year’s cash position.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.

Learn. Grow. Build. Now.

function ml_webform_success_14362251() { var $ = ml_jQuery || jQuery; $(‘.ml-subscribe-form-14362251 .row-success’).show(); $(‘.ml-subscribe-form-14362251 .row-form’).hide(); } fetch(“https://assets.mailerlite.com/jsonp/918262/forms/119753320103413631/takel”)

We know that a cash flow statement is in fact the description of our cash inflows and outflows. Both inflows and outflows are further categorized into operating, investing, and financing activities.

Why is this important?

We all know that cash inflows make our cash increase, and cash outflows make our cash decrease. Obviously, if I add up all my cash inflows and all my cash outflows respectively and then subtract the latter by the former, I will get a number representative of my net cash flow – the actual increase or decrease in the company’s cash.

But we actually can get this number from another place that we have covered before: the balance sheet. In the balance sheet, our first asset item is cash. If we use our cash position of this year and subtract that of last year, we will get the net cash flow of this year.

Then what is the purpose of creating a separate financial statement, i.e. cash flow statement, considering that we’ve already arrived at the same number from our balance sheet?

Let’s look at an example.

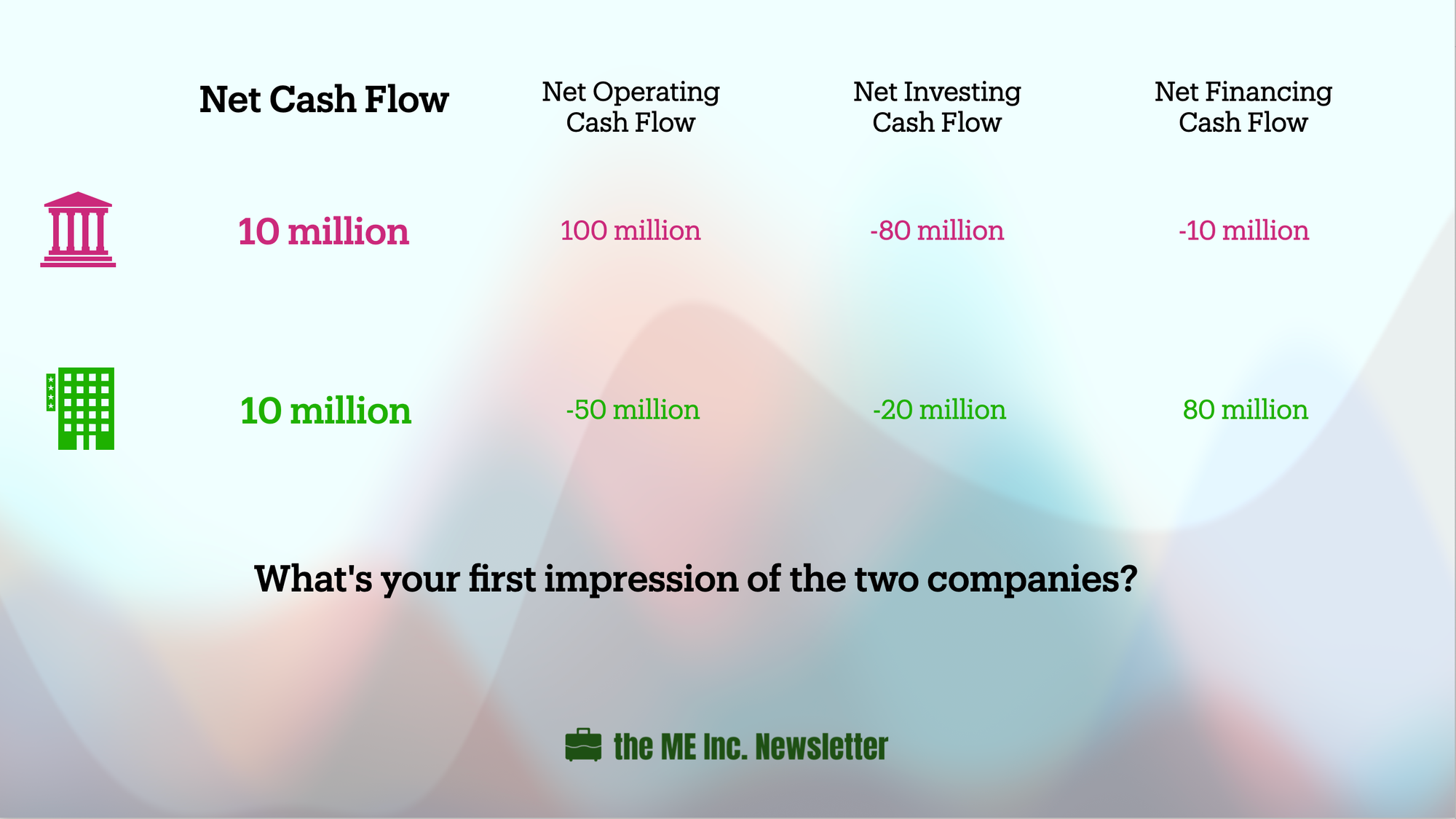

Say there are two companies, both of which has a net cash flow of 10 million dollars for the past year.

For Company A, the cash flow for operating activities is 100 million dollars. They spent 80 million on investing activities and 10 million on financing activities, making the net cash flow 10 million dollars.

For Company B, the cash flow for operating activities is negative 50 million dollars. They spent 20 million on investing activities, and raised 80 million dollars from financing activities, making their net cash flow 10 million dollars as well.

What’s your first impression of the two companies?

Well, Company A might appear more appealing to most people because it creates positive operating cash flow, and since operating activities are the most predictable, the company might create similar cash flow from operating activities in the future.

But for Company B, where does its money come from? It comes from financing activities. Its operating activities and investing activities don’t create cash, but consume cash. In this situation, the future of the company is rather uncertain, as we don’t know if the company will be able to raise money next year.

This example shows us why we should not only know the amount of increase or decrease in cash, but also explore the reason for the change. Different reasons could mean very different things to us.

For example, we always want most of our inflows from operating activities, because they are more predictable and likely to last for a long time. Meanwhile, for outflows, we’d want our money spent on investment. Why? Because investments might create future returns for the company.

Therefore, only knowing if the cash flow is net positive or negative is insufficient; we also need to know the reason behind, and that is (one of) the reasons why we need the cash flow statement.

In fact, let’s try dig a little deeper.

If you think about it, CASH is really just one asset item on the balance sheet. Why do we make a fuss about this one item, and not the rest of asset items?

In other words, what makes CASH so special that it deserves this special treatment?

Well you already know the answer from your everyday life, and that is:

Cash can be used to buy other assets almost instantaneously, but it’d take much longer time to turn other assets into cash. The company will be doomed if without sufficient cash and might go bankrupt.

In other words, having cash is closely related to the survival of a company.

From this point, we can come up with another reason why we need cash flow statement: we care about the survival of the company. In other words, we care about the risks of failure in our company’s continuing operation.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.

Learn. Grow. Build. Now.

function ml_webform_success_14362251() { var $ = ml_jQuery || jQuery; $(‘.ml-subscribe-form-14362251 .row-success’).show(); $(‘.ml-subscribe-form-14362251 .row-form’).hide(); } fetch(“https://assets.mailerlite.com/jsonp/918262/forms/119753320103413631/takel”)

At the very beginning of this journey we mentioned that there are three financial statements – balance sheet, income statement, and cash flow statement. We have covered the first two, and now let’s look at their relationships between we go into the third statement.

A balance sheet has two sides. On the left side, it shows the assets; on the right side, it shows the liabilities and stockholder’s equity. An income statement functions like a funnel where at the very top we have the revenue of the company, and by deducting all costs, expenses, and taxes from the revenue, we will arrive at the net profit of the company.

For our fictional company, it has a 5.2 million dollars net profit for its first year of operations. The shareholders have decided to distribute 1 million dollars as dividends, and keep the other 4.2 million dollars as retained earnings in the company. If our company makes another 5.8 million dollars of net profit in the next year and have decided to keep every penny in the company, the company will have a total of 10 million dollars of retained earnings by the end of the second year. Here we can see that balance sheet shows us the current status of the company’s financial situation, while income statement shows the process of a period of time.

Cash Flow Statement

Cash flow statement might look the most daunting amongst the three financial statements. It is long, and includes a primary table and appendix. Both parts have a lot of information. However, even though cash flow statements look the most complex, it is actually the easiest financial report. First, let’s look at what is cash flow.

Definition of Cash Flow

Cash flow is such an simple concept that everyone can understand easily. Just like what the name tells us, Cash Flow is simply cash flowing in and out of the company. Cash inflow means money I receive, and cash outflow means money I spend.

Therefore, cash flow statements tell us the amount of money I receive and spend. That’s it.

For example, sometimes we hears people say they are doing some bookkeeping for themselves. They rarely would make a balance sheet or an income statement. More often than not, bookkeeping is just some sort of financial journaling, detailing every single transaction the person has made. To write down these journal entries, one does not need any accounting skills. All that is needed is simple addition and subtraction.

And that is all you need to do cash flow statements well.

How to Cash Flow

Different from doing a personal financial journal, we categorize business activities into:

operating activities

investing activities

financing activities

Even though a company might have all kinds of business activities, sometimes well over tens of thousands in a year, from an accountant’s perspective, companies only have these three kinds of business activities. So all cash inflows and outflows will be divided in these three categories.

In fact, I can also do my own bookkeeping based on this categorization.

For example, if I get paid today from my company, what kind of cash flow is this?

Put it in another way: if my household is the company, me going out to work every day is the company’s main business operations. In addition, since I’m receiving money from my company, this is a cash inflow from my operating activity.

After I got paid, I bought some groceries on my way home. From the household’s perspective, the action of buying groceries should also be my operating activity, because it happens every day. This is an operating cash outflow. Other than groceries, we can easily come up with other similar operating cash outflows such as the wage I pay to the hourly cleaners, the personal income tax, etc.

Once I have been working a while, I have saved some money and am ready to buy a house and a car. Such purchases don’t happen every day, and from the household’s perspective, both are investing cash outflow since we are paying somebody money. If I sold my house or car and received money, it should be investing cash inflow.

What if I got a loan when I purchase the house or car? Getting a loan is also often called getting “financing”, and it’s easy to conclude that this is financing cash inflow (because I’m receiving money from the bank). On the other hand, when the payment terms kick in for me to pay back interests and principal, the expenses related to the loan are financing cash outflows.

So even as an individual who wants to bookkeep his own expenses, I can still separate the records into the three categories. This classification will not add, but reduce complexity.

Cash Flow Statement for Company

For a company, what cash inflow and outflow are there?

Operating Cash Inflow

Similar to households, a company’s most common operating cash inflow is sales. When we sell something, we will generally receive cash, sooner or later. This is an important operating cash inflow.

One interesting item that might appear on the cash flow statement is a cash inflow tax item. How can tax become a cash inflow?

One possible explanation is that certain companies might receive tax returns for operating in certain industries that are encouraged by the government. An even more common explanation that applies to almost all companies is that since companies will “charge” value-added tax on top of the product price and withhold it on behalf of the tax bureau, it will show up as an operating cash inflow.

Operating Cash Outflow

Next, I might need to buy inventories such as raw materials, pay salaries to my employees, and pay taxes to the tax bureau, etc. All of these business activities will incur operating cash outflow.

Investing Cash Inflow

What will lead to the investing cash inflow? There are two possibilities.

One possibility is when I sold my investment. For example, the sales of buildings, equipments, machines, vehicles (investment in the company), or the sales of stocks or bonds of the companies I invest (investment outside the company), all of which bring in cash inflows.

Another possibility is when my investments pay dividends. For example, a subsidiary may pay me dividends, which is a return on my investment. This return also brings me cash inflow.

Investing Cash Outflow

There are only two kinds of investment for business: investing in the company and investing outside the company. The former will become tangible and intangible assets of the company, while the latter will become stocks, bonds, or other finance products in other companies. No matter the investment is inside or outside of the company, money spent on investment is investing cash outflows.

Financing Cash Inflow

For companies, there are two way to financing money: issuing debt or issuing stock. Whichever option the company selects, it will bring cash inflow.

Financing Cash Outflow

If a company issues debt, it will need to pay interests upon the debt’s maturity. If a company issues stock, it may need to distribute dividends to shareholders. Both debt payments and dividends are financing cash outflows.

These are easy to understand. But there is actually another activity that might incur financing cash inflow – leasing.

Not all leasing contracts are the same. From an accounting perspective, we need to differentiate leases by the size of payments and the length of contracts. Short-term and small leases are categorized into operating leases, and long-term and big leases are categorized into capital leases. Even though both are leases, from an accounting perspective, capital leases are actually considered purchases of assets by way of debt, and each term of lease payment will be treated as interest payment, or financing cash outflow. Capital leases actually show up on the balance sheet under liabilities as “long-term payable”.

Now that we’ve gone over the basics of a cash flow statement of a company, we will dig deeper into what the statement shows us in the next few episodes.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.

Learn. Grow. Build. Now.

function ml_webform_success_14362251() { var $ = ml_jQuery || jQuery; $(‘.ml-subscribe-form-14362251 .row-success’).show(); $(‘.ml-subscribe-form-14362251 .row-form’).hide(); } fetch(“https://assets.mailerlite.com/jsonp/918262/forms/119753320103413631/takel”)

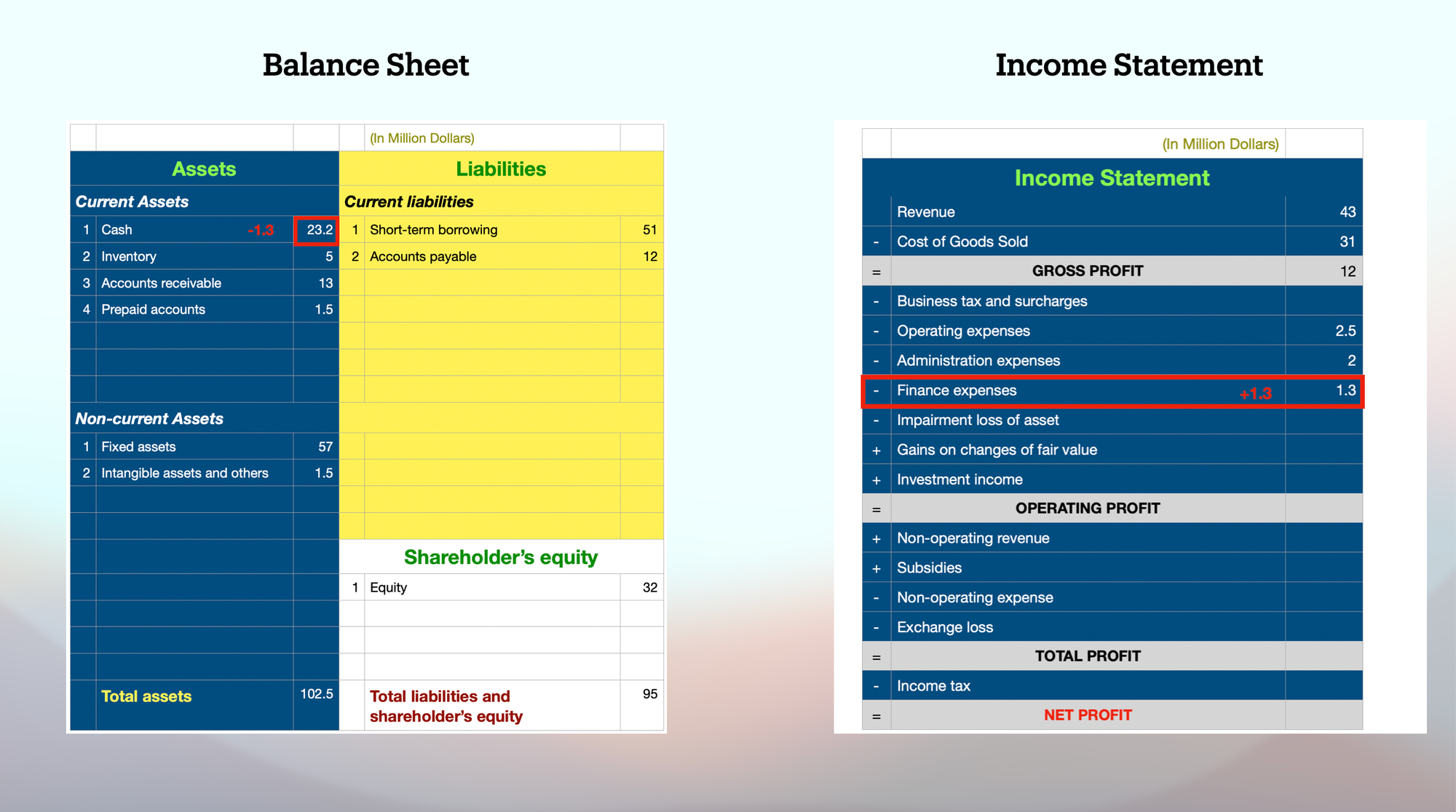

Because we borrowed money from the bank, we now owe the bank 1.3 million dollars of interest expenses in the first year. At the end of the first year, the money is due and we will pay out this amount from our bank account. As a result of this, our cash position is reduced by 1.3 million dollars on the balance sheet, and we also need to record the same amount under financial expenses on the income statement.

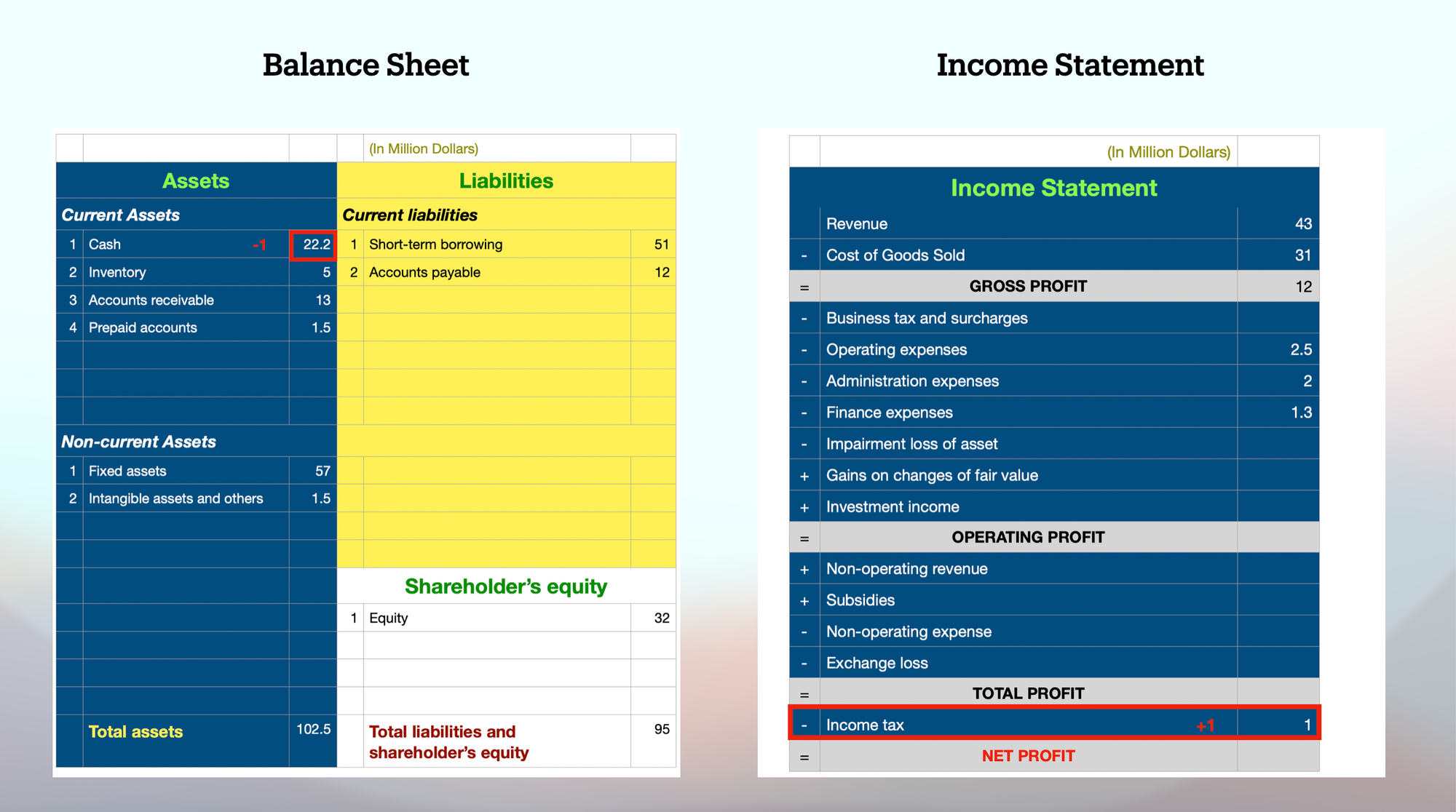

Next, our company accrued 1 million dollars of income tax from our first year’s operations.

Once again, we will need to pay out 1 million dollars from the bank account, so our cash is reduced by this amount. On the income statement, there is a place called income tax and that’s where we put the 1 million dollars in.

Now that we have all the costs and expenses recorded, what is our net profit from this year’s operations?

We can get the number by subtracting all the costs and expenses from our revenue, and we come up with 5.2 million dollars – our first year’s net proft.

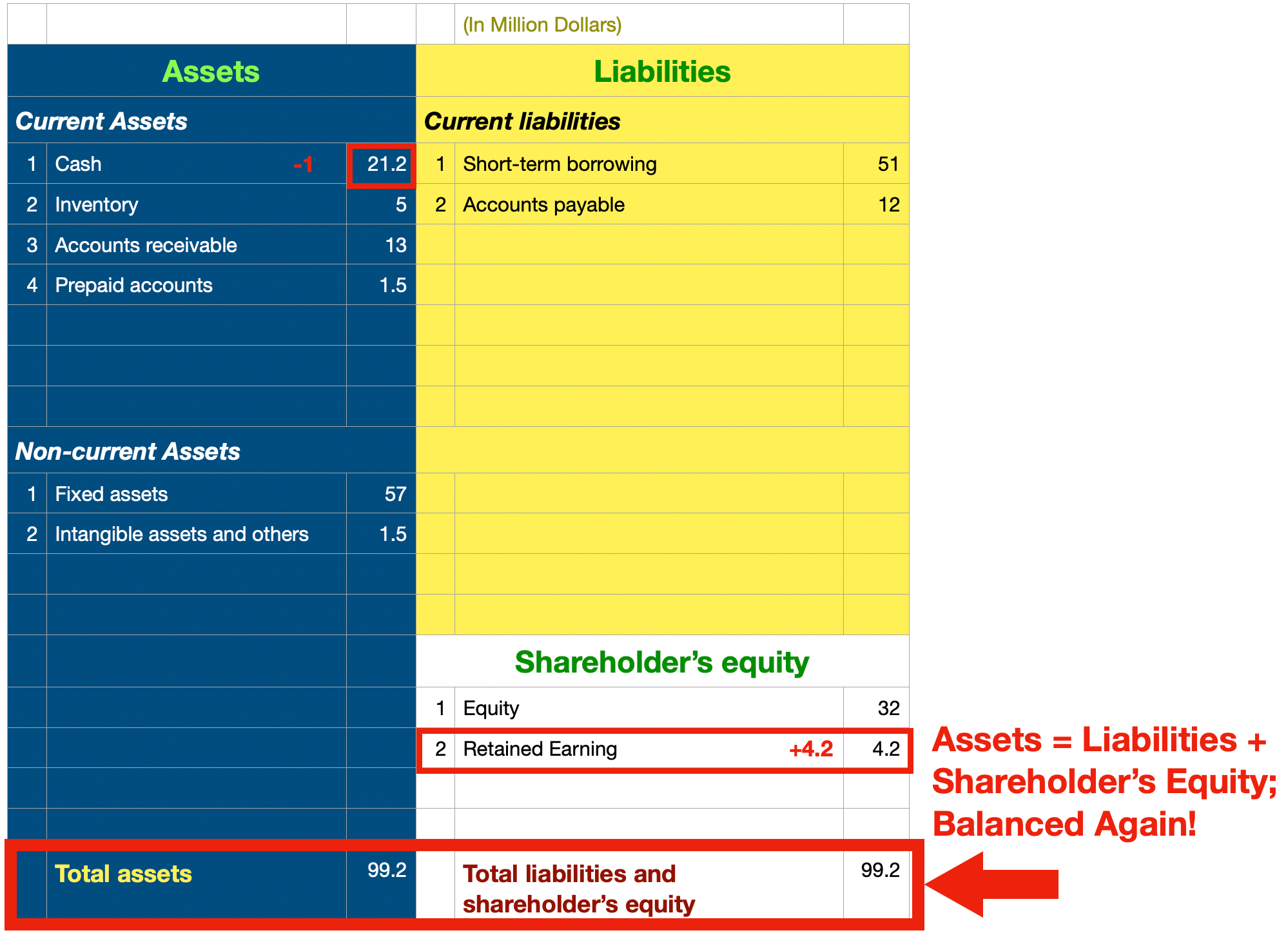

As a shareholder of the company, we have the option to withdraw this money from the company. Let’s assume that instead, we’ve decided to withdraw only 1 million dollars from the company and keep 4.2 million dollars in the company. The 1 million is called cash dividend. The 4.2 million dollars, if you recall, is actually treated as reinvestment into the company by the shareholders, called Retained Earnings.

The total of 4.2 million dollars actually belong to the shareholders, but instead, they choose to put the money back into the company, making this money retained earnings.

Our cash position further decreases by 1 million dollars after we decide to distribute this amount as cash dividends to shareholders. We then put 4.2 million dollars in retained earnings under Shareholder’s Equity. This economic activity does NOT affect income statement, since it stops once the net profit is arrived at.

So far all economic activities occurred to our fictional company are reflected on our statements one by one. That is to say the statements presented before us are the balance sheet and income statement of the Company. Let’s have a look at the statements.

Income Statement

From the income statement we can see that our company made 43 million dollars in the first year, and spent 31 million dollars on costs of those goods sold. The Gross Profit of making the sales is 12 million dollars.

Next, our company incurred 2.5 million dollars of operating expenses, 2 million dollars of administrative expenses, and 1.3 million dollars of financial expenses in the form of interests. We didn’t suffer any impairment loss of asset, and made no investment income. The Operating Profit of the company is 6.2 million dollars. Without non-operating incomes and expenses and subsidy income, the Total Profit is also 6.2 million dollars.

With the deduction of one million dollar income taxes, the Net Profit of 5.2 million dollars.

In summary, our company made 43 million dollars in revenue, which resulted in 5.2 million dollars in net profit in the first year. That is more than 10% net profit ratio! Considering that this is the first year of the company’s operations since establishment, this number is not only good, but great!

Balance Sheet

On the balance sheet we can see that the company has 99.2 million dollars worth of assets, contributed by the bank, shareholders, and supplier. Let’s break it down a little bit and see how this happened.

First, the shareholder invested 32 million dollars and borrowed 51 million dollars from the bank. In the course of operation, we owed the suppliers and various parties 12 million dollars. At last there is another 4.2 million dollars left as an additional investment of the shareholder to the company. This is where the 99.2 million dollars worth of funds came from.

So where has all the money gone?

We can see that theres still 21.2 million dollars of cash in the bank account as cash. We also have 5 million dollars of inventory, 13 million dollars of accounts receivable, and 1.5 million dollars of advanced payments. All of these are current assets, i.e. assets that can be turned into cash easily.

Further down the line, 57 million dollars are turned into the fixed assets and 1.5 million dollars into intangible assets, i.e. land usage rights.

The balance sheet describes a company’s financial condition – what our initially invested money has become. The reason we care about this is that before we make money from our investments, we want to know whether our principal is safe.

Let’s analyze this a little bit before we jump to the conclusion.

Is My Investment Safe?

Our concern is that the value of the assets will be lost somehow. Which project do you think has the biggest risk?

The first thing we see is accounts receivable. There are 13 million dollars of accounts receivable for the company. If there is any reason that part of the 13 million dollars are uncollectible, this asset will need to be reduced. For example, if 2 out of the 13 million dollars are not collectible, we will have to change this asset item into 11 million dollars. If we do not consider the impact on the tax, the net profit of 5.2 million dollars would now shrink to 3.2 million dollars. If there are more than 2 million, say 10 million dollars of the 13 million become uncollectible, this problem would be very serious. The net profit would no longer be 5.2 million dollars; it would be a negative number!

We can see that the guaranteed value of our assets is super important for obtaining reliable profits. Of course, besides the existing risk of uncollectible receivables, our inventory value might decrease; our fixed assets will wear or tear, accruing depreciations. Fixed assets may also encounter sudden decrease in value due to technology advancement, i.e. when there are more advanced technologies in the market, the current value of fixed assets (equipment) will decrease suddenly. Similar things could happen to intangible assets as well.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.

Learn. Grow. Build. Now.

function ml_webform_success_14362251() { var $ = ml_jQuery || jQuery; $(‘.ml-subscribe-form-14362251 .row-success’).show(); $(‘.ml-subscribe-form-14362251 .row-form’).hide(); } fetch(“https://assets.mailerlite.com/jsonp/918262/forms/119753320103413631/takel”)

Next, we are going to take a slightly longer view, and prepare for next year.

To make sure we are ready for next year’s operations, we will prepay 1.5 million dollars to our supplier and secure raw material supplies. Since 1.5 million dollars are prepaid, our cash position is reduced by this amount. At the same time, we should record 1.5 million dollars as prepaid accounts because we have the right to receive goods from the supplier in the future, making it an asset. After this economic activity, we can see that the the total amount of assets is not changed.

During this year while we were selling our products, our company also spent 4 million dollars in cash, 2.5 of which on salaries of sales personnel and sales related expenses, and 1.5 of which on salaries of managers and managerial expenses. Our cash position was further reduced by 4 million dollars on the balance sheet. At the same time, we should put the 2.5 million dollars under operating expenses, and 1.5 million dollars under administrative expenses.

Next, we’ve decided to invest half a million dollars to developing a pollution treatment technology, which is a research and development activity. How does this affect our financial statements?

Well, it’s easy to know that our cash is further reduced by 500,000 dollars on the balance sheet. On the surface, we might be tempted to put 500,000 dollars under intangible asset, since technology appears to be a type of intangible asset. However, this is actually wrong. Let’s see why that is the case.

The accounting principles stipulate that R&D expenses shall be recorded as expenses, specifically, administrative expenses in the Income Statement. If and only if the R&D is in the product development stage and it meets certain criteria could it be recorded under intangible assets. Here research means the true, hardcore development of a new technology, and product development means things like design of packages, etc., that happens after the development of the core tech.

The accounting principles also stipulate that after we successfully developed a technology and applied for a patent, ONLY the application fees for the patent may be recorded in intangible assets. For example, if we spent 500,000 dollars in researching a technology and another 5,000 dollars on the patent application, only the 5,000 can be recorded in intangible assets.

This might seem strange, and unreasonable at first glance. We all think that research and development is actually a thing that impacts long-term development of a company in the future, and because of that, we should record it as an asset item – intangible asset.

The reason it doesn’t work that way is that R&D is an activity with high uncertainty. When a tech is being developed in the lab, it’s very difficult to say whether it will be successfully productized and commercialized. Let us look at some data.

For the American pharmaceutical industry, the average length of drug development is about 14.9 years with the cost of around 500 million dollars, among which 200 million is invested before the clinical experiment stage. However, only 18% of all drugs can actually enter the clinical experiment stage, meaning that 82% of all drug development investments are pure expenses.

This stat shows that R&D activity has crazy high uncertainty. The accounting profession, however, hates uncertainty, and whenever there appears uncertainty, accounting will treat it as – failure, by default, even if there is still chance for it to succeed.

And that is why all R&D activities are treated as expenses, i.e. useless for the future.

Now let’s go back to our company and push the scenario one step further. What if our 500,000 dollars of research investment does succeed, i.e. we have created a successful technology? Can we record it in intangible assets?

Unfortunately, still no.

The reason is that technological success does NOT equal commercial success. We can see lots of examples that a technology creates no commercial value at last. So it still has considerable uncertainty even after the tech is developed.

Lastly, the accounting principles stipulate that technology purchased externally should be recorded in intangible assets. The reason is that our purchase equals our acknowledgment in the commercial value of the tech, so only by then could we record it with a value equal to the purchase price.

From the aforementioned three principles on R&D, we see that research itself will not result in increase of intangible assets. Looking reversely, if there is indeed intangible asserts such as technology in a company’s balance sheet, it almost always means that the company has purchased the tech from external parties.

We can further draw a conclusion that all self-generated intangible assets of the company will not be reflected on the balance sheet. Let’s look at another example.

Say we want to invest in building a brand for our product by investing in advertisements. When we pay for the ads, the ad costs go into operating expenses. We will never record these types of costs as intangible assets for the reason that we have no idea how much value of intangible assets can be created by the ads we make.

This is not to say that self-generated intangible assets are worthless. On the contrary, these assets are at the very core of a company’s competence, but are left off the balance sheet. In other words, a company will have many important off-balance-sheet assets. For example, a company may own important technology, brands as well as other valuable assets that according to accounting principles, must be left off the balance sheet. These “assets” are valuable and important, but because of their uniqueness, their values are hard to determine.

Then what are the intangible assets that we see on the balance sheet? They are all purchased from others by the company.

This unique characteristic of intangible assets being off the statement and valuable at the same time can be used by companies for their own advantages. For example, sometimes a company might need to reflect their R&D investment in the balance sheet, and to do so they might sell the technology and buy it back. But most companies would not do something like this; instead, a more common way is that the company will establish a separate entity – an independent R&D subsidiary – to handle all the R&D. The company will then procure technology from this independent legal entity, resulting in the R&D cost showing up as intangible assets on the company’s balance sheet.

From this example, we see that the accounting principles stay the same. But by using different organizational structures, we can get different results. There is no good or bad in either practice; different companies might pursue different practices to suit their objectives. For some very profitable companies, for instance, they may prefer to record R&D as expenses so they could reduce the tax burdens. For some other companies, e.g. startups, they might want to record R&D as intangible assets so their profits look good.

So coming back to our original case, the 500,000 dollars research expense will cause a corresponding dip of cash in balance sheet. We should also record this amount as administrative expense in the income statement.

Sharing my learnings about the core skills on how to run life like a company in the Me Inc. Newsletter. Topics covered: Copywriting, Finance, Technology, and Productivity. Read my why here or join directly👇. No spams. Ever. – Michael

Welcome to the Me Inc. Newsletter.

Build yourself into a business, before you start one.

Learn. Grow. Build. Now.

function ml_webform_success_14362251() { var $ = ml_jQuery || jQuery; $(‘.ml-subscribe-form-14362251 .row-success’).show(); $(‘.ml-subscribe-form-14362251 .row-form’).hide(); } fetch(“https://assets.mailerlite.com/jsonp/918262/forms/119753320103413631/takel”)