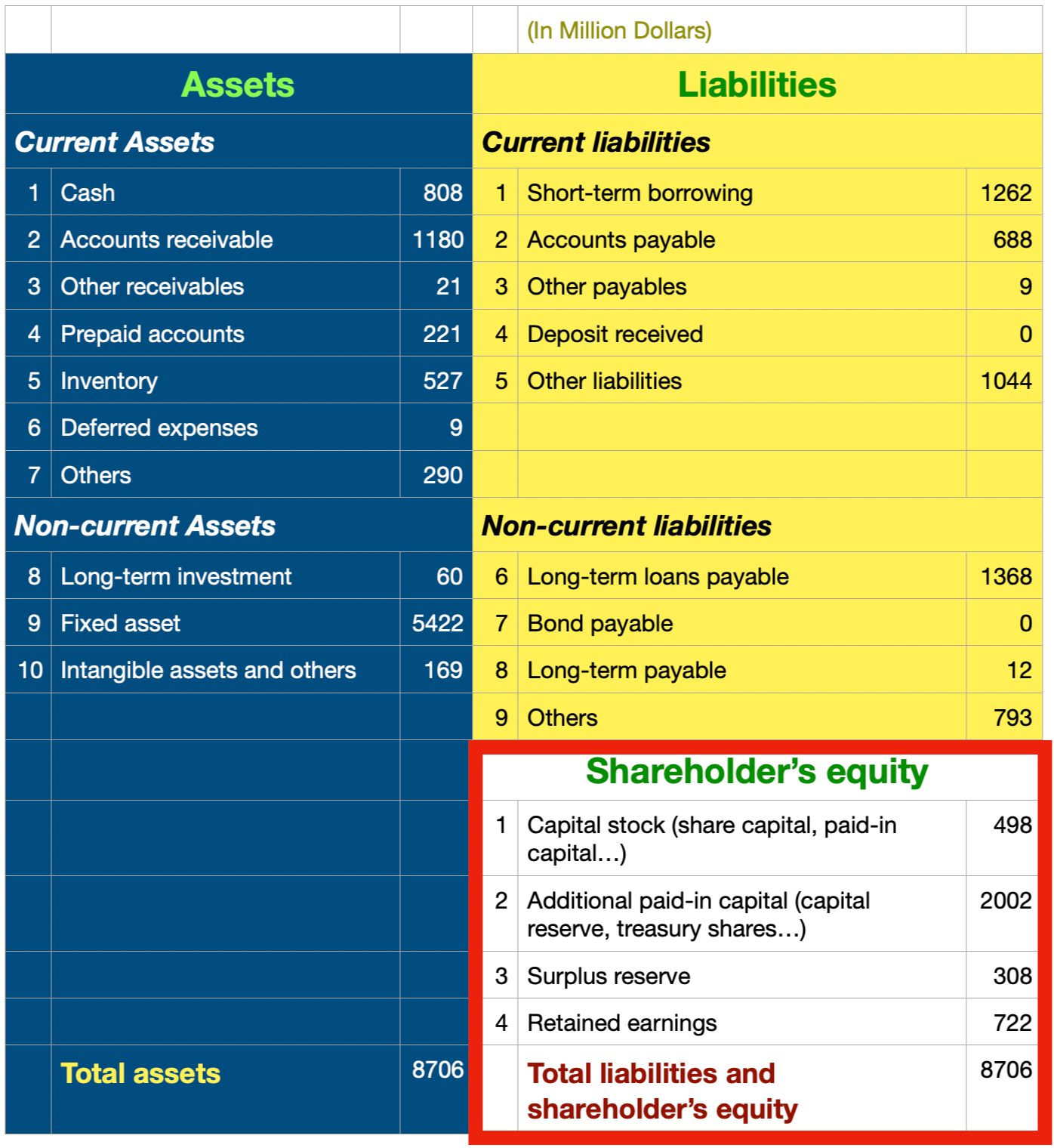

In previous episodes of the Learning Finance series, I’ve learned Basics of Balance Sheet , different types of assets, how to use Balance Sheet to understand how companies work, and the basic rules of asset pricing system . I’ve also learned different types of liabilities. Now we will look at the last section on the Balance Sheet – Shareholder’s Equity.

There are four items in Shareholder’s Equity:

- Capital Stock

- Additional paid-in capital

- Surplus reserve

- Retained earnings

Let’s go over these together.

There are mainly two ways shareholders can invest in a company.

First, shareholders can inject money into the company as their investment. By doing so, the shareholder’s money will become the company’s money, and the shareholder will receive equity, i.e. proof of ownership in the company, in exchange. This is a form of external investment.

Second, when the company makes a profit in its operations, the profit is originally owned by the shareholder. However, the shareholder may decide not to take the profit home but instead keep it in the company. This is also a form of investment, but internal.

For the four items mentioned above, which ones are external, and which internal?

It’s difficult to know the answer just by their names without fully understand what they are, but you can still guess that capital stock might be a form of external investment, and retainied earning is a form of internal investment. If those are your answers, then you guessed them right.

But what about additional paid-in capital and surplus reserve?

Right now, let’s just take note of the answer that additional paid-in capital is external, and surplus reserve is internal. By the end of this article, you will be able to understand what they are, and why.

External Investments

When capital comes in, it’s recorded on the Balance Sheet separately under two lines of items in the Shareholder’s Equity Section, Capital Stock and Additional Paid-in Capital.

Why do we account them in two separate items?

Capital Stock (Share Capital, Paid-in Capital, Equity…)

This is arguably the most important item. At least I think that way.

However, this item can get a little bit confusing, since you may not always see the name Capital Stock on a balance sheet. Different types of companies may use different names for essentially the same thing.

For example, the concept of “stock” only exists in public companies, i.e. only when a company goes public will its stocks be created. So in public companies, you will see this item with the names like Capital Stock, Share Capital, etc. In private companies, or limited liability companies, the same item is called paid-in capital. However, no matter what names are used, the meaning is the same.

In certain countries such as China, every company needs a registered capital required by law. That is, when you form a company, you have to inject money into the new entity. The amount of money that you inject is called registered capital. In China, the value of capital stock (or share capital, paid-in capital) must be equal to the registered capital. In other countries, such registered capital requirements is not necessary, so this item won’t necessarily equal registered capital. All money invested is considered original fund of the company.

However, you might be wondering this:

If the actual money invested is more than the registered capital, where does the extra money go on our Balance Sheet?

The answer is Additional paid-in capital.

Additional Paid-in Capital (Capital Reserve, Treasure Shares…)

There is one type of company that will always have additional paid-in capital on its balance sheet. That type of company is publicly traded company. Why?

We know that publicly listed companies issues shares to the public. For example, when it issues 100 million shares of stock at 20 dollars per share, how should we record this transaction?

By doing some simple math, we know that the company raised 2 billion dollars. Since the nominal value per share is one dollar, we will record 100 million dollars as Capital Stock. The rest 1.9 billion dollars will be kept in Additional Paid-in Capital, as known as Capital Reserve or Treasure Shares.

The above example described how a publicly traded company accumulates capital reserve. But how can private companies generate additional paid-in capital? Let’s look at this example.

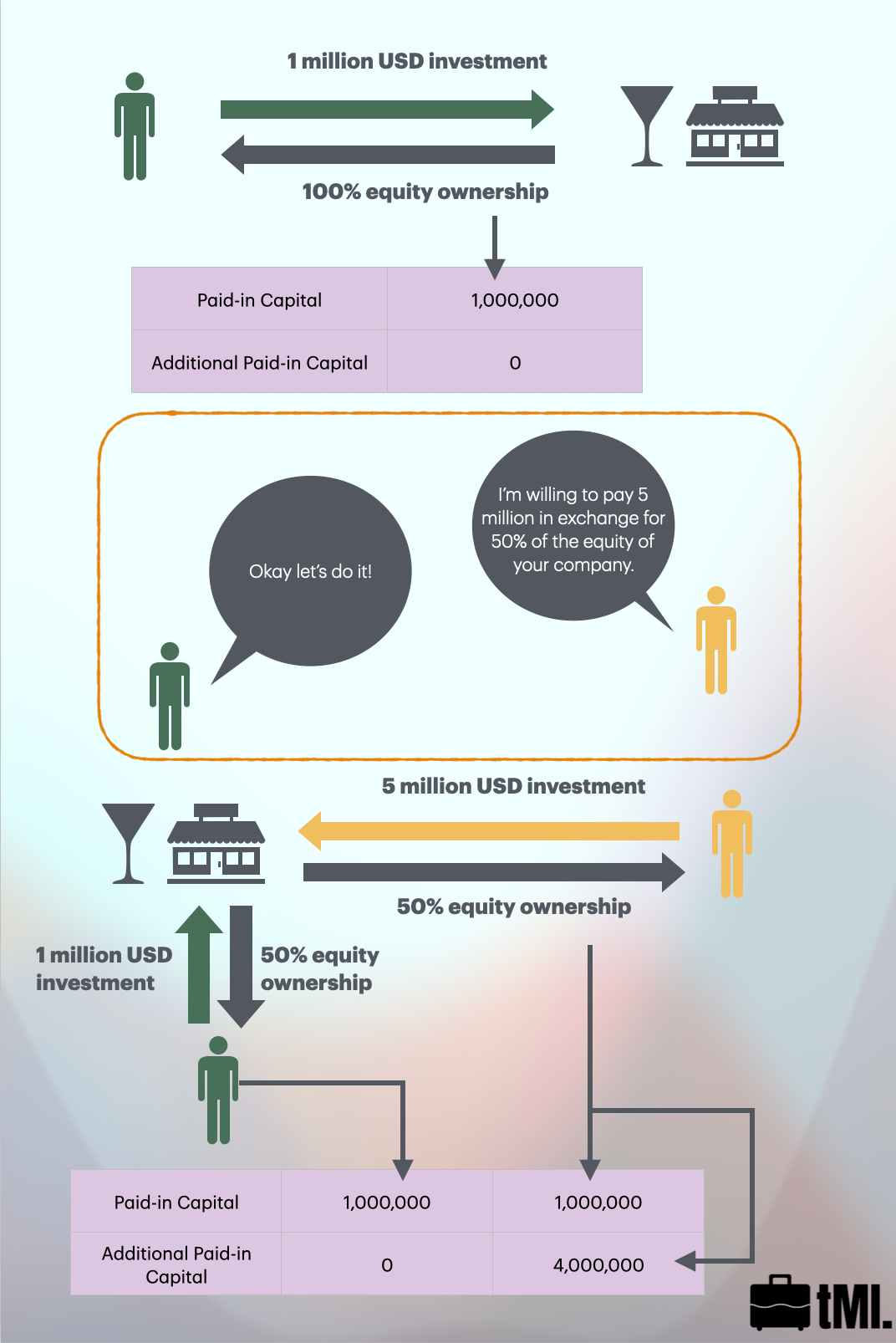

Say I invested one million dollars to start a small company. After a few years, the business runs well, and someone is interested in investing in my company. After some due dilligence and negotiations, we finally reached a deal: I agreed to sell 50% of the company for five million dollars. In other words, we both agreed that the company is worth 10 million dollars now.

But the thing is that I invested one million dollars and my new partner will invest five million dollars. How can I document this investment on the Balance Sheet so the shares are split 50/50, not 5/6 for him and 1/6 for me?

The answer lies in additional paid-in capital.

Out of the five million dollars, one million will go in paid-in capital, matching my initial one million-dollar investment and boosting the total equity to two million. The other four million dollars will go into additional paid-in capital. Since ownership percentage is only calculated by paid-in capital, the company’s ownership is now split equally between the two of us. The other four million dollars in the additional paid-in capital are now owned by all shareholders of the company.

That means I now own two million dollars out of the four. The second this investor invested five million dollars in my company, two million dollars will evaporate instantaneously out of his pocket. Why did he do that?

When I started the company from my own one million dollars, the company was worth just that. But after so many years, I’ve built up the company to a higher level, far more valuable than what it was. From this perspective, the investor exchanged his two million for the 50% of the company income in the future.

— First, at least in China, the total amount of Paid-in Capital is equal to the company’s registered capital, which is the company’s maximum external legal liability should it be subject to bankruptcy.

— Second, the capital structure reflects the division of interest among the company’s shareholders. That is, when the company has more than one shareholder, the division of shares is NOT in accordance with each shareholder’s total capital contributions, but with the proportion of Paid-in Capital.

Internal Investments

When a company makes a profit, the shareholders can choose to either distribute those profits to themselves or keep them in the company. If they choose to keep the profits in the company, those profits essentially become internal investments.

Surplus Reserve (only in certain countries)

Surplus reserve is profit that cannot be distributed by the law. In some countries such as China, the law stipulates that a company must retain some profit as surplus reserve in the company. In other words, if the company earns 10 million dollars this year, I must leave at least one million in the company as surplus reserve.

Shareholders are free to distribute the remaining nine million dollars; for example, they may decide to distribute three million dollars to all shareholders, and leave six million dollars in the company.

Retained Earnings

Where should we put the remaining six million dollars? In the retained earnings.

By far we have gained a more complete understanding about the balance sheet. We’ve already known the meaning and composition of assets, liabilities and shareholders’ equity respectively. Later we will look at how the balance sheet presents a complete picture of a company’s finance.