Bank of America froze me out of my bank account a while ago due to some technicalities and now my account is in danger of being treated as abandoned property because it hadn’t been accessed for some time. Even though I have been calling their customer support consistently – which is outright useless and disrespectful most of the time – the problem persisted. Thanks to Reddit community r/BankofAmerica, I filed a report on Consumer Financial Protection Bureau (CFPB) and within one day, I heard back from Bank of America via email and a phone call. I don’t know if the problem can eventually be resolved, but I do want to document the process of filing the report online on CFPB so more people can know and understand how to do it. In the meantime, will just keep my fingers crossed!

First, find the site – CFPB

CFPB is in charge of consumer financial protection (as its name suggests) and the first step is the locate the right website. You can Google CFPB or click the link here or use the link above to go to the sign up page directly. This is what the website looks like (and the “file a complaint” option is down when you scroll):

cfpb official site: you can see it’s official coz “An official website of the United States government”

Second, sign up

Then there is the sign up process which doesn’t require too much info and is very straightforward. Then you go to the file process which has 5 steps to follow. Do notice that the site doesn’t really have a “save” option so it is better to prepare in advance and file the complaint in one sitting.

Third, the actual filing steps

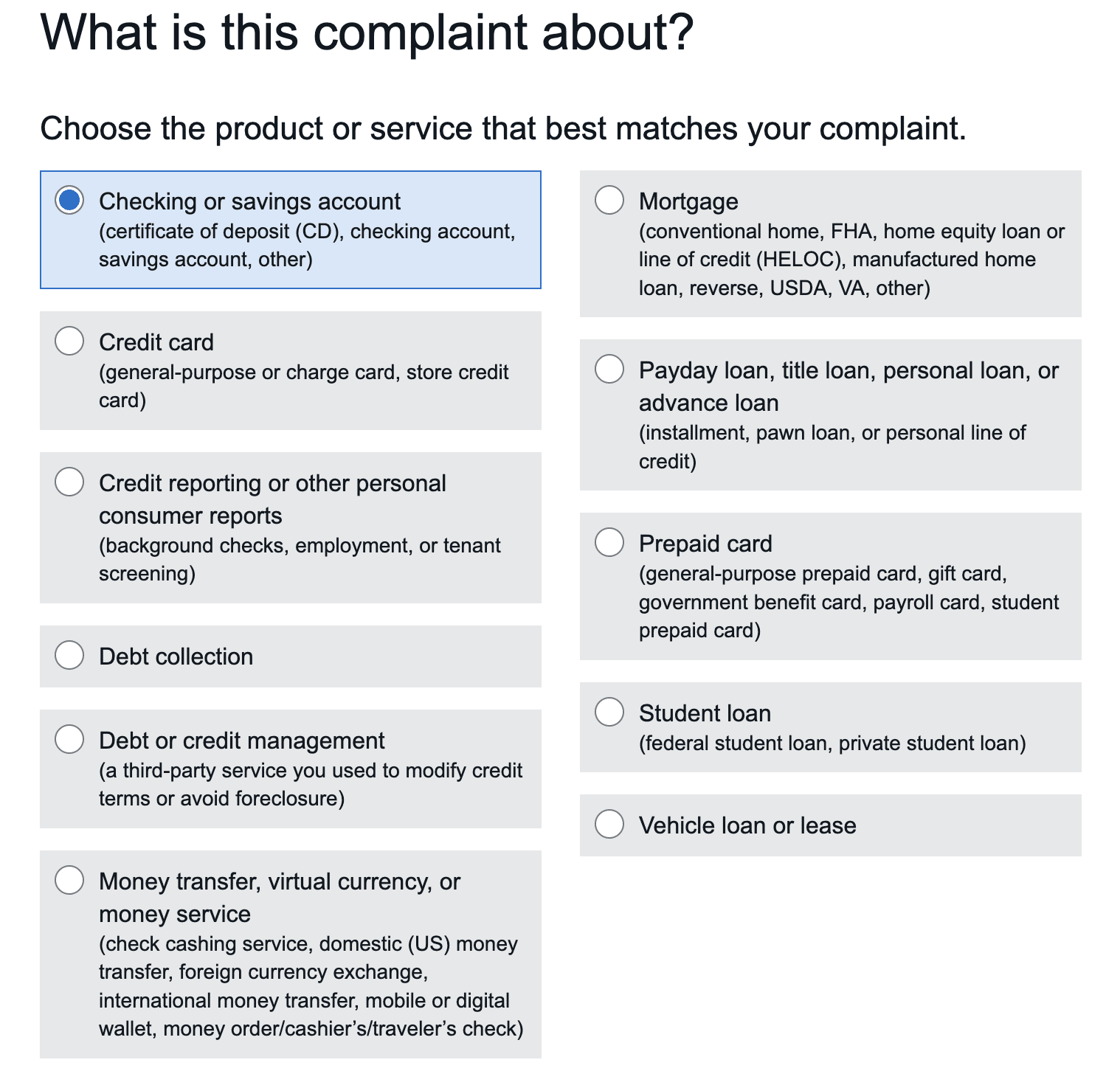

Step 1: what is this complaint about?

Then choose the product or service that best matches your complaint.

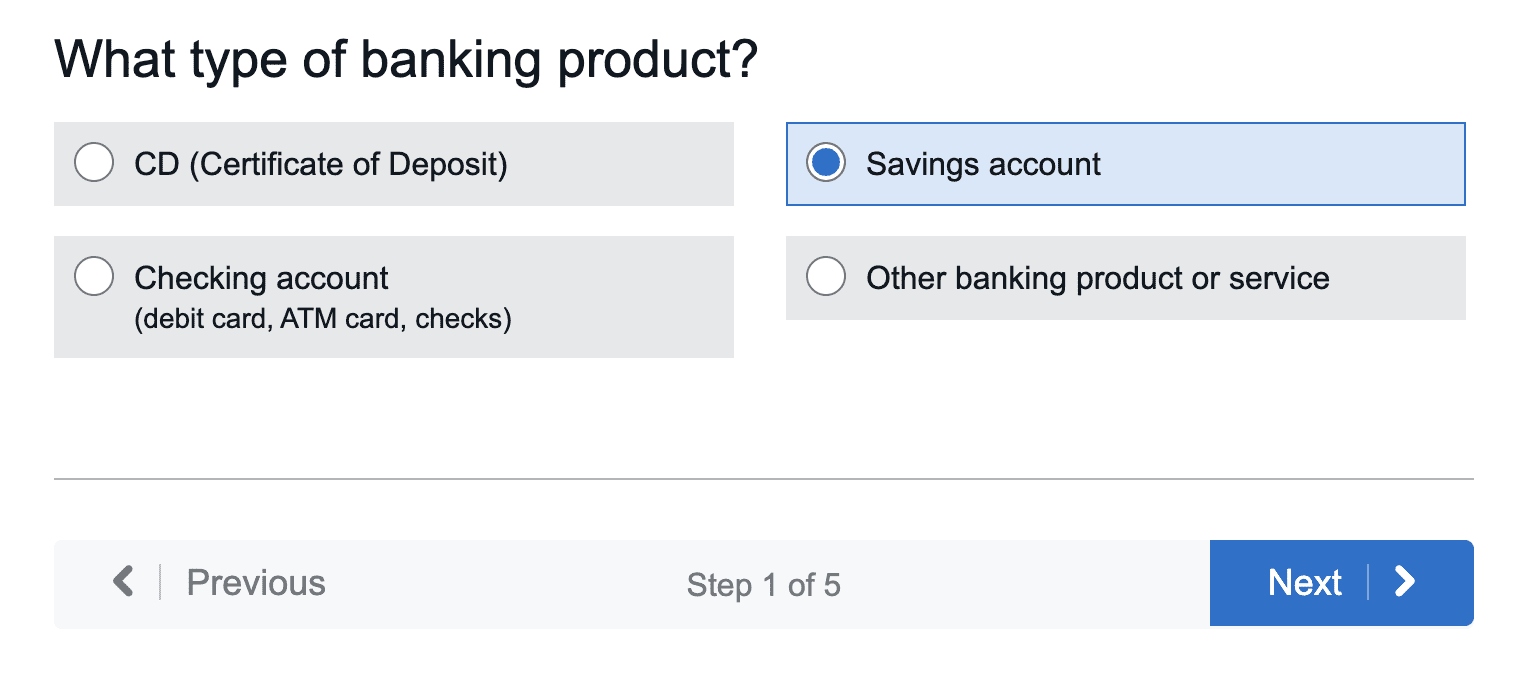

After that, choose what type of banking product.

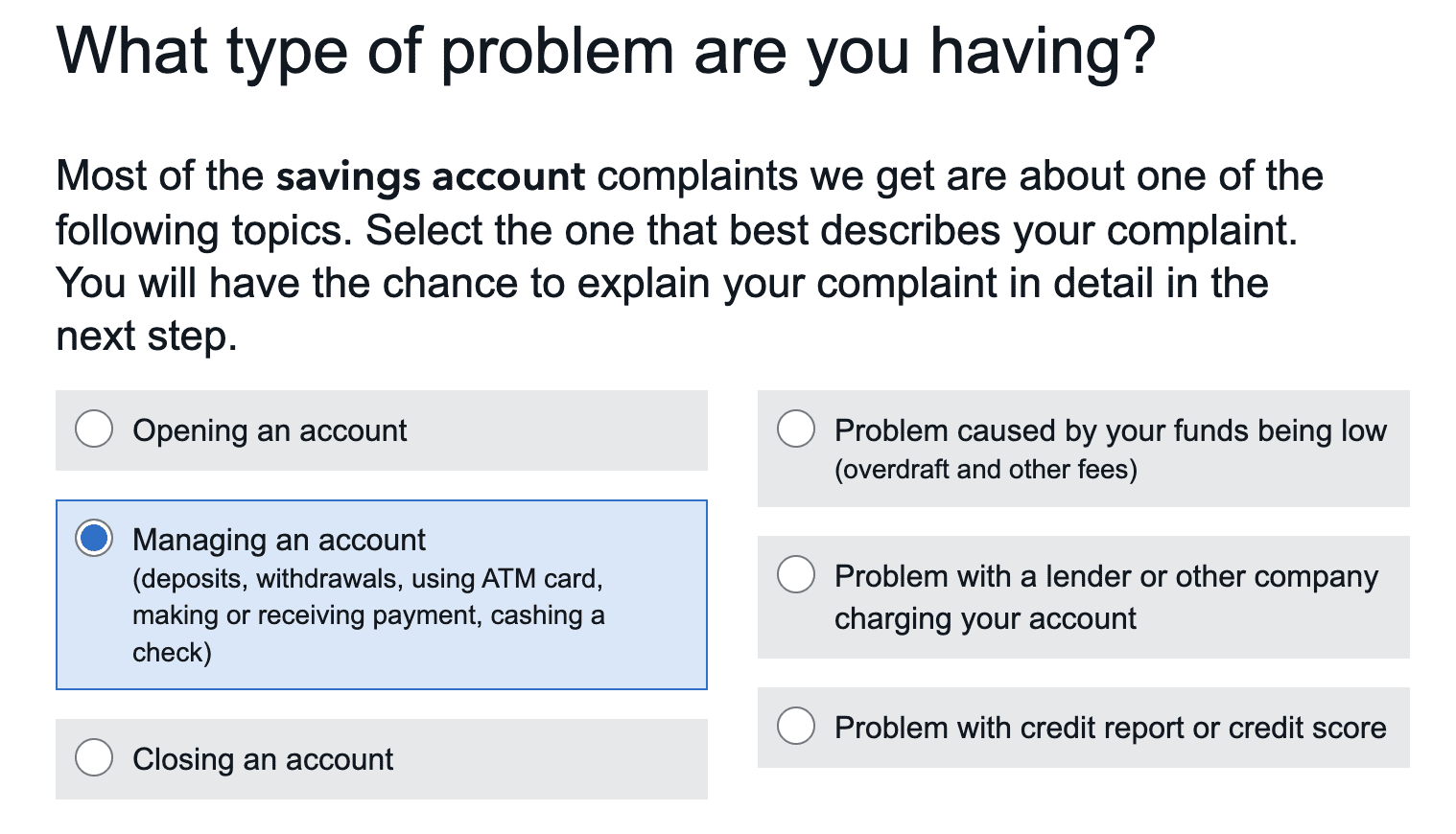

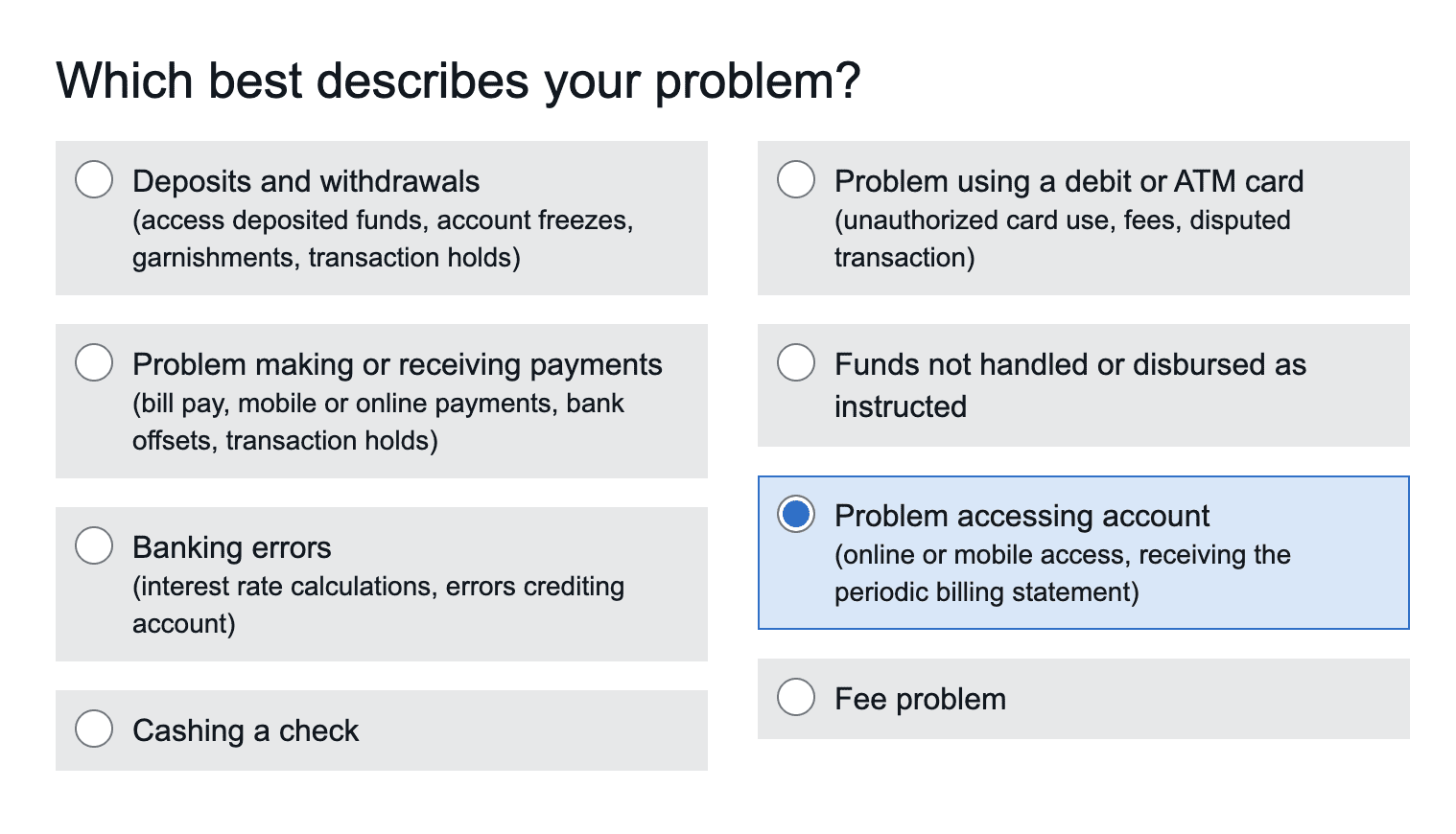

Step 2: What type of problem are you having?

Choose the topic that best fits your complaint.

Choose which option best describes your problem.

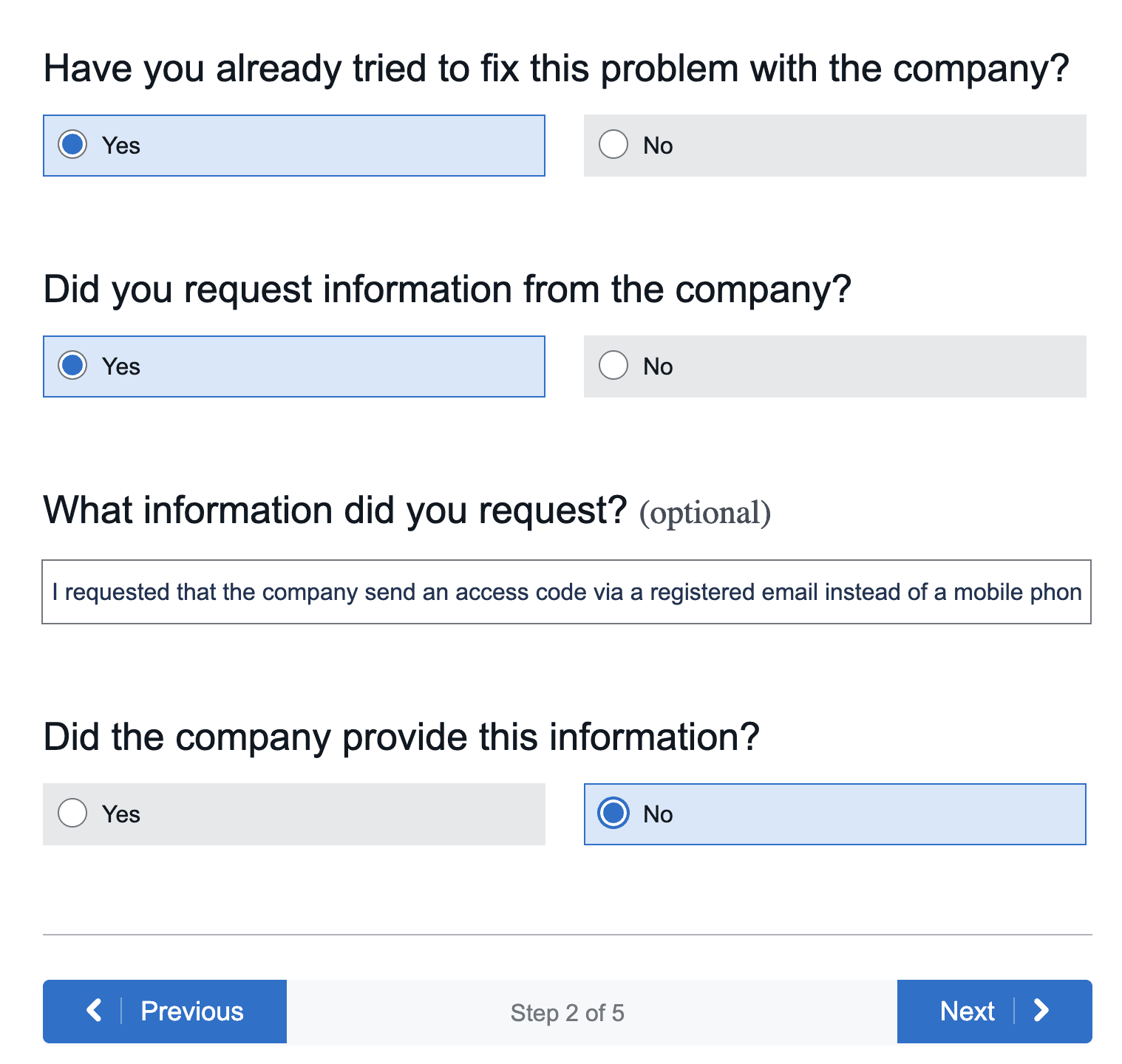

Afterwards, choose actions you have already taken to make things happen (but obviously failed).

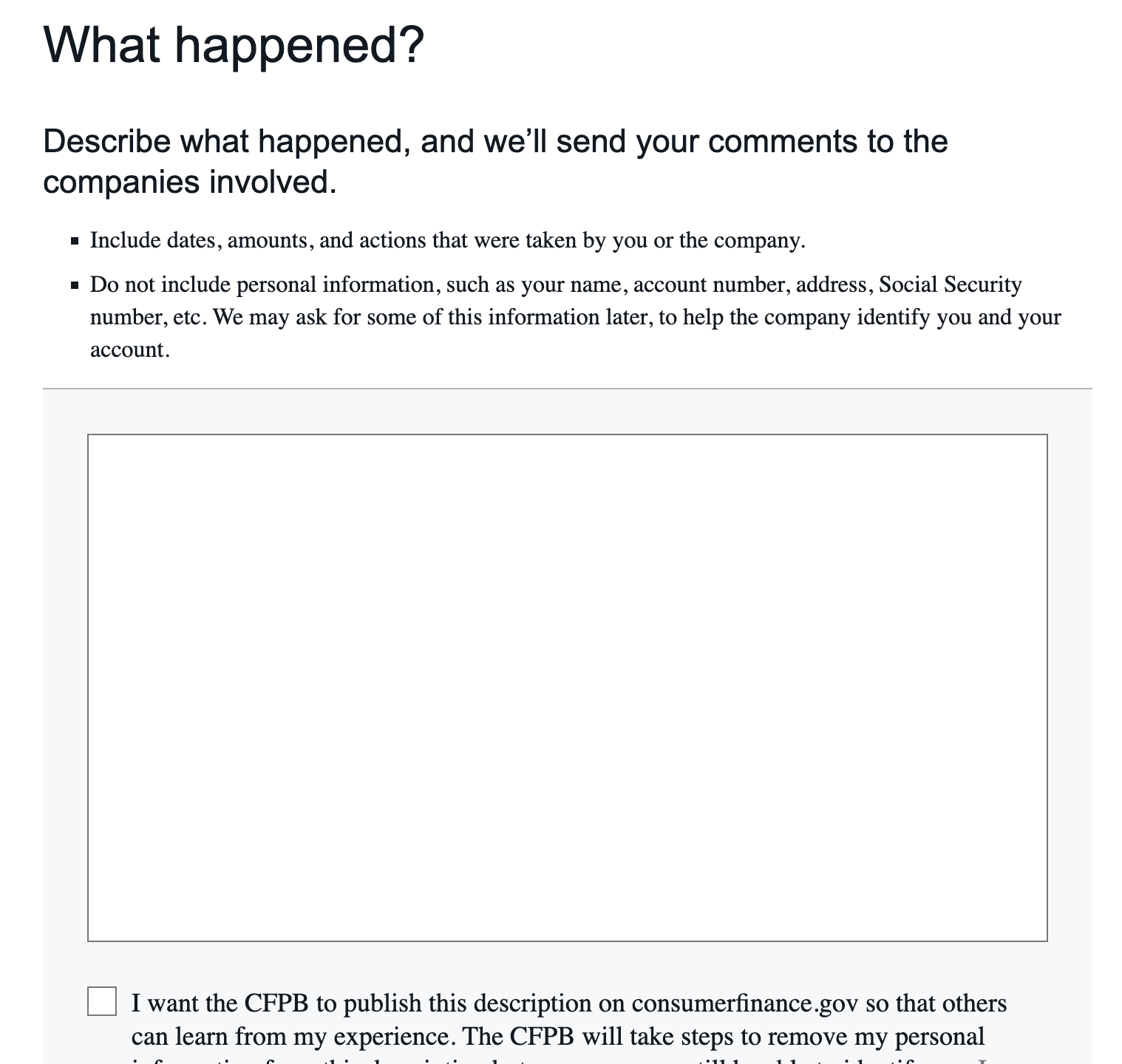

Step 3: What happened?

First, describe what happened, and CFPB will send your comments to the companies involved.

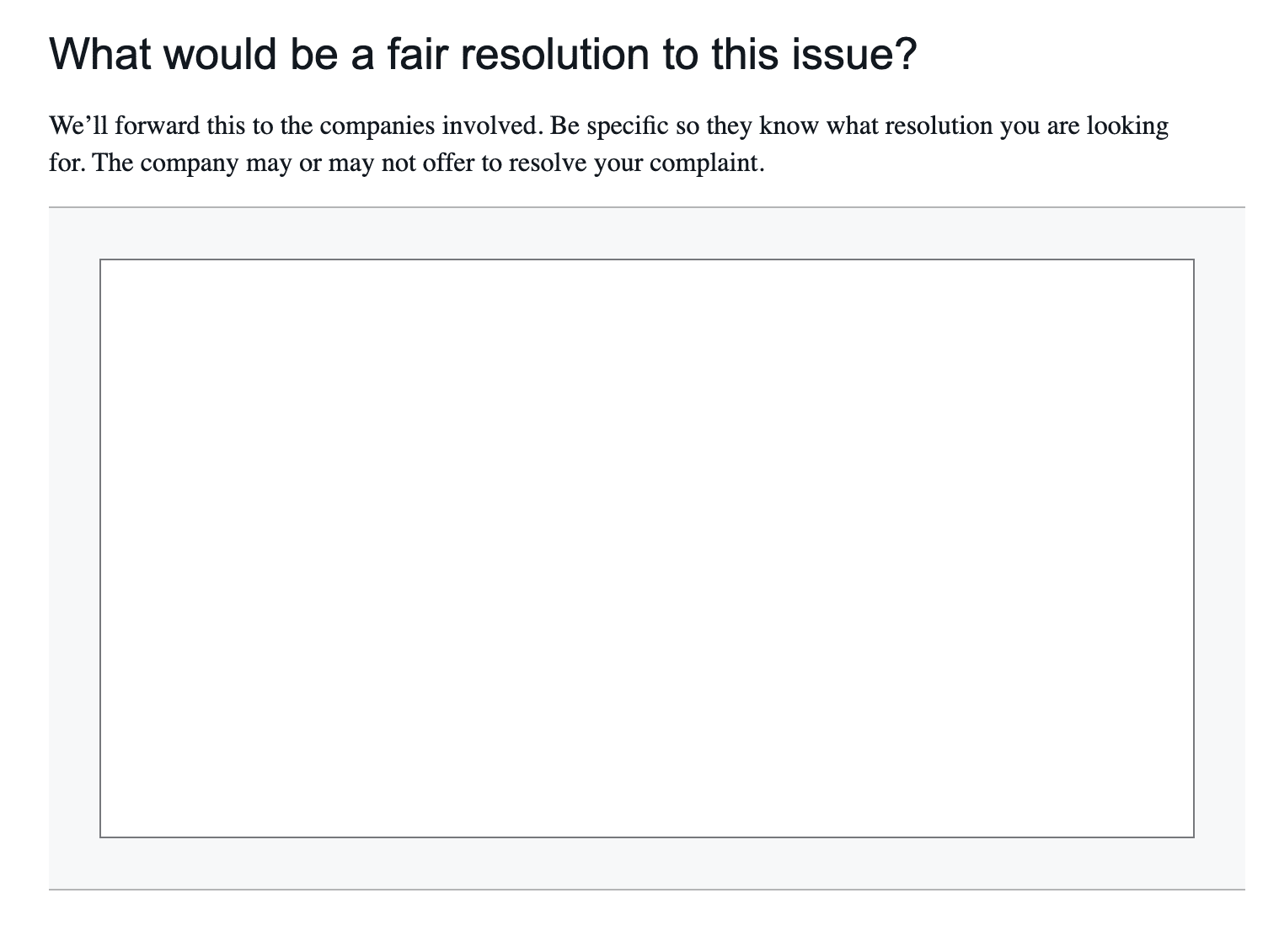

Then you suggest a fair solution to the issue.

Optionally, you can attach any document you think might help.

Step 4: What company is this complaint about?

Step 5: Your contact info and some other demographic related questions (optional)

Basic contact info. You don’t have to fill your demo info if you don’t want to since this is just helping CFPB better understand the people they are serving.

After submission, you will get to this page:

I don’t know why banks still function like this even when so much technology exists (and they still declare they care about tech advancement in their org!). Life is hard enough, and these large corporations are making it harder for the everyday people. Hope everybody can get out of the issues they are facing! And don’t loose faith! (follow me on X if you want for any reason @themichaelshoe.)

This is the final post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome back! In this final lesson of our introduction to U.S. equity market structure, we’ll put everything we’ve learned together and walk through the life cycle of a simple order from start to finish. Let’s follow what happens when you place an order to buy shares.

The Order

Let’s assume you want to buy 1,000 shares of General Electric (GE). The last sale price for GE was $10, and currently, the best bid (the highest price a buyer is willing to pay) is $9.99, while the best offer (the lowest price a seller is willing to accept) is $10.

Your Broker

You have a retail trading account with an online broker. This is where you go to enter your trade. Using your broker’s interface, you enter the following information:

Order Type: You decide to place a limit order at $10. You are comfortable with paying $10, but you don’t want to pay more if the price rises.

Instructions: You fill in the details, review the order, and hit transmit.

Entering the Market

Once your order enters the market, 500 shares are immediately filled at the midpoint price of $9.99 (due to hidden or non-displayed liquidity). This gives you an advantage, saving $2.50 compared to your original limit price of $10.

For the remaining 500 shares, your electronic broker sends your order to the exchanges where the stock is quoted at $10. Fortunately, there’s enough available volume at this price, and the rest of your order is filled at $10.

Final Execution

In total, you bought 1,000 shares of GE. The total cost comes to $9,997.50, thanks to the price improvement on the first 500 shares. This was a successful execution because you paid less than your limit order anticipated.

Other Options

There are many other ways this trade could have played out depending on the order type and additional instructions you could have given. For example, if you were dealing with a larger order that would take more time to execute, you might have chosen an IEX D-Peg order. This order type adjusts the execution price based on market conditions, protecting you from trading when prices are unstable.

These advanced features can help optimize your trading strategies, especially in high-speed environments.

Conclusion

And that’s the life cycle of a simple trade, from your initial idea to the final execution. Thanks for joining this course on U.S. equity market structure. If you’re curious about more advanced topics or want to dive deeper into trading strategies, don’t hesitate to reach out. Happy trading!

This is the fifth post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome back to our introduction to U.S. equity market structure. In the last lesson, we talked about the key players—broker-dealers and investors. Now, let’s explore what happens on the “field” of trading and how broker-dealers execute trades, either for themselves or on behalf of clients.

Speed of Trading

A critical component in today’s market is the speed of trading. Decades ago, the action on the New York Stock Exchange floor was the heartbeat of the market, but today, trading happens in nanoseconds. Stock prices can rise or fall in seconds, far too fast for humans to process. This high-speed trading is a result of technological advancements and fierce competition. The faster a trader can act, the more of an advantage they have, similar to being able to watch the game in slow motion while others are at normal speed.

While this technological evolution has made markets more efficient—allowing prices to quickly reflect new information—it has also raised concerns about fairness. Speed can lead to an uneven playing field, where certain participants profit by trading based on minute price movements over very short time periods.

Order Types

When a broker-dealer is ready to trade, they must use order types—instructions that tell the trading venue how to execute the trade. Order types specify the conditions for buying or selling a stock. Some basic order types include:

Market Orders: These orders instruct the broker to buy or sell immediately at the current market price, prioritizing execution over price.

Limit Orders: These orders set a maximum (for buying) or minimum (for selling) price at which the trader is willing to execute. They are less aggressive than market orders since they wait for the price to reach a specific level.

Beyond these, there are more complex order types. One example is pegged orders, which adjust their price relative to the prevailing market quote. A midpoint peg, for instance, will price itself halfway between the best bid and offer, while a near-touch peg will rest at the best bid (for buying) or best offer (for selling). Pegged orders are often hidden, meaning they don’t display their price to the market until they execute.

There are also instructions that can modify orders, such as specifying the time of day when the order should be executed or setting a minimum number of shares that must be traded at once. These added details help broker-dealers and investors fine-tune their trades to fit specific strategies.

Algorithmic Trading

In today’s market, algorithmic trading plays a dominant role. Algorithms are pre-programmed sets of rules that automatically manage trades based on market conditions. For example, an algorithm designed to buy 10,000 shares of Apple will determine how to split the order, which order types to use, and how to react to changes in the market—all without human intervention.

Algorithms enable trades to happen incredibly quickly, reacting to new market conditions in real time. Just as a sports team follows a defensive strategy without needing to stop and consult the coach, these algorithms follow pre-set rules that allow them to adapt instantly to market movements.

There are many types of trading algorithms, each designed with different goals in mind. Some algorithms aim to minimize market impact, while others are programmed to execute trades at the Volume Weighted Average Price (VWAP) or seek liquidity in dark pools (private trading venues that don’t display order book data). These strategies, like the zone defense in basketball, are built to respond automatically to market changes.

Conclusion

In this lesson, we’ve covered the mechanics of modern trading, from order types to the algorithms that have revolutionized the speed and efficiency of the market. In the next and final lesson, we’ll follow a simple trade from the moment it’s placed to its final execution, tracing the full journey of an order through the U.S. equity market system.

This is the fourth post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome back to our introduction to U.S. equity market structure. Now that we’ve discussed the rules of the game, the playing field, and the “ball” (the stocks), let’s dive into how trading really happens by focusing on the key players: broker-dealers and investors.

Investors

Investors are the ultimate stakeholders in the market—the ones the SEC is designed to protect. Investors provide the capital that companies use to grow and fuel the economy. They can be individual investors, like people buying stocks or contributing to a 401(k), or institutional investors, like asset managers handling pension funds or mutual funds on behalf of individuals.

If you invest in a company or have a retirement account, you’re considered an investor. Approximately half of Americans are invested in the stock market in some form. Investors play a key role by researching companies, making decisions on whether to buy or sell, and holding stocks whose value fluctuates with market performance.

While investors are central to the market, they often can’t execute trades directly. When you place a trade on your brokerage account, you’re not submitting that order directly to the exchange. Instead, you rely on a registered broker-dealer to execute the trade on your behalf.

Broker-Dealers

In many ways, broker-dealers are the actual “players” on the field. These firms are licensed to buy and sell securities, playing both the role of agent (when trading on behalf of clients) and principal (when trading for their own account). Broker-dealers provide the crucial bridge between investors and the stock exchanges.

Broker (or agency broker) refers to firms or individuals that execute trades for clients.

Dealer (or principal trader) refers to those who trade on their own account.

Prime brokerage is a term for brokers that offer additional services like securities lending, leveraged trade executions, and cash management, which large investors often require.

Proprietary traders trade mostly for their own accounts, and they tend to have more flexibility because they don’t handle client orders. High-frequency traders (HFTs) are often proprietary traders.

Retail broker-dealers serve individual investors, helping them buy and sell stocks.

Responsibilities of Brokers

Brokers have certain responsibilities to their clients, particularly regarding “best execution” and “order routing.”

Best Execution Brokers are legally required to seek the best execution for their clients’ orders. This means they must strive to achieve the best price reasonably available at the time of the trade. At a minimum, this means they can’t execute an order at a price worse than what’s being displayed in the market elsewhere. However, brokers are also encouraged to seek “price improvement,” aiming for a price better than the current market quote if possible.

Order Routing When you place a trade, brokers must decide where to send your order for execution. This is called order routing. If you don’t specify where to route your trade, brokers have discretion over the decision. According to Rule 606 of Regulation NMS, brokers must report where they send orders that don’t have specific instructions. You can find these reports online by searching for a broker’s “606 report.”

Brokers balance different priorities depending on whether they represent themselves or their clients. The strategies and tactics they use will vary based on the instructions or goals of their clients.

In the next lesson, we’ll explore the strategies and tactics that broker-dealers use when trading in the U.S. equity market.

This is the third post of a series on US Equity Market Structure (a total of 6).

I didn’t write any of these posts; while I was learning the fundamentals about investment, I came across this series on Interactive Brokers’ IBKRCampus. If you are interested you can go to their site here.

(Disclosure: I’m using Interactive Brokers for my personal investing, but I’m not paid by them to write about it.)

This series is mostly platform-agnostic, meaning that you don’t have to be on Interactive Brokers to find this series useful. Enjoy.

Welcome back to our introductory course on U.S. equity markets. In our previous lessons, we talked about the rules and regulators of the game, as well as the playing field and referees—the trading venues. Now that we have the structure set up, it’s time to dig into what we mean when we say U.S. equities and what we’re actually trading—the ball in the game of trading.

As you know, when you buy stock in a company, you aren’t buying a concrete object. For example, if you buy a share in a pencil-making company, you can’t go to their factory and demand a bunch of pencils or one of their pencil-making machines. Instead, the stock represents an ownership stake in the company, giving you certain rights. For instance, if the company is sold, you generally get part of the purchase price, and you usually get a vote on certain decisions.

What Are U.S. Equities?

In general, when we talk about U.S. equities, we are referring to stocks that are registered with the SEC and listed on one of the U.S. stock exchanges. These stocks are publicly traded, meaning that pretty much anyone can go to their broker and buy a share. This is in contrast to private companies, which often sell shares to private investors, but those shares aren’t available to everyone.

There are also some public company stocks that trade only over-the-counter (OTC), usually because they are too small to qualify to list on one of the major exchanges. Those stocks are not considered part of the National Market System (NMS), so we’ll set them aside for now.

Most U.S. equities are often called single stocks, meaning they represent an ownership stake in a particular company. There are also equities called exchange-traded products (ETPs) that allow buyers to purchase a share in a set of stocks, often an index, rather than just one company. For instance, if you buy a share of an S&P 500 ETF (SPY), you are really buying fractions of each of the S&P 500 stocks.

Where Stocks Trade

We know from the previous lesson that stocks trade on exchanges and other trading venues. But one thing to keep in mind is that NMS stocks actually trade on all of these exchanges and usually across all other trading venues too. This is a result of Regulation NMS, which we discussed in the first lesson, the regulation that tied all of the exchanges together.

In many cases, people assume that stocks only or predominantly trade on the exchange where they are listed, and in fact, this was the case until a few decades ago. But today, during regular trading days, stocks can be traded across all different venues.

Listings Explained

If stocks can be traded across all of these trading venues, what does it mean to be “listed” on an exchange? Well, a company’s listing exchange has three main responsibilities.

First, the listing exchange handles a company’s auctions. The most high-profile auction for a company is usually its Initial Public Offering (IPO). Most companies become public through an IPO, which occurs when a private company decides it wants to become publicly traded. There are several advantages to being a publicly listed company: it allows owners to more easily sell their shares, making them more liquid, and it gives the company the option to sell more shares, raising capital that they can invest in the business. It also provides the company with a more liquid currency to acquire other companies or for mergers and acquisitions (M&A).

An IPO allows a company to become publicly traded and raise capital by selling new shares at the same time. In an IPO, the company offers a large number of new shares for sale through a group of brokers known as a syndicate. The night before the stock starts trading publicly, those shares are priced and sold to a set of large investors. The next morning, a big auction is held on the company’s listing exchange, and the company’s stock becomes available for trading moving forward. The listing exchange is responsible for the technology and rules to ensure that the auction is handled fairly and smoothly.

Recently, a few companies, including Spotify and Slack, opted to become public through what is called a “direct listing.” In a direct listing, the company still holds a big auction on its first day of trading, but the auction only includes existing shares that shareholders choose to sell, rather than new shares that the company makes available.

But the IPO auction isn’t the only one. Every weekday, there’s an opening auction (typically at 9:30 a.m. Eastern Time) and a closing auction (typically at 4:00 p.m. Eastern Time) for every stock. Before those auctions, brokers submit their orders to the listing exchange, detailing how many shares they want and what price they are willing to pay. The exchange gathers that information and, at the time of the auction, matches buyers and sellers at a single price that allows the most shares to be exchanged.

Second, the listing exchange is responsible for surveillance of its listed stocks. The exchange monitors trading in that stock and refers cases to regulators if there seems to be manipulative activity. The listing exchange can also halt trading in its listed stocks if needed and is in charge of disseminating important data, such as dividend information.

Lastly, the listing exchange provides services to companies to help them navigate the public market. This isn’t required by regulation, but it’s an expected practice in the industry. These services vary depending on the exchange’s particular strengths and the fees they charge for listing.

In our next episode, we’ll talk about who actually trades in the U.S. equity market and how investors and brokers operate.