To clearly describe the economic activities of a company, a company first needs a Balance Sheet. The reason is to understand what the initial investment has become, and whether its value is maintained.

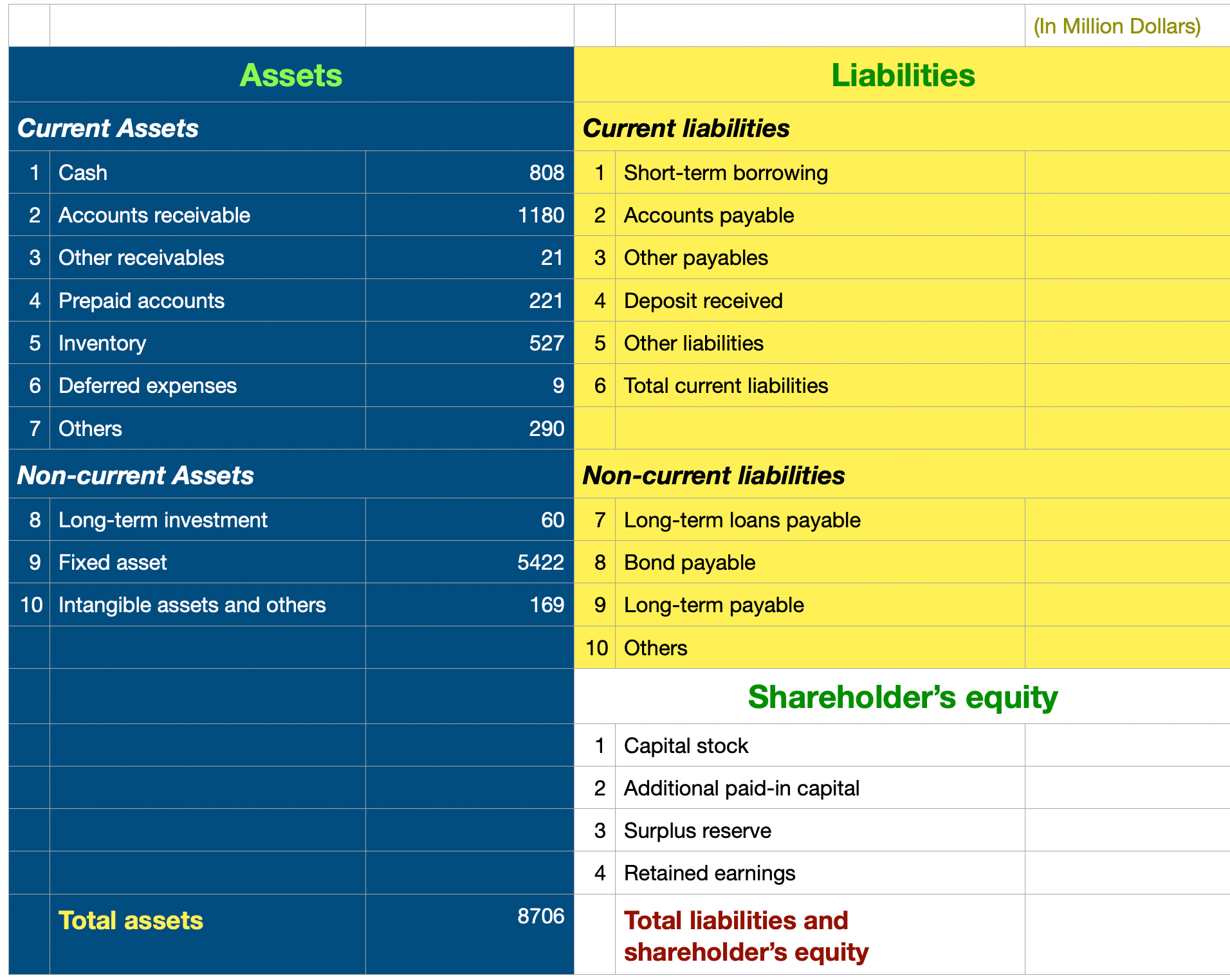

This is what Balance Sheet looks like.

A Balance Sheet is mainly divided into two columns, one on the left and one on the right.

On the left, I got my Assets. On the right there are 2 things listed. The one on the top is called “Liabilities“, the one on the bottom is “Shareholders’ Equity“.

There is a very important equation called Assets = Liabilities + Equity, but we don’t have to worry about it now. First, let’s tackle each item one by one.

Let’s look at Assets first.

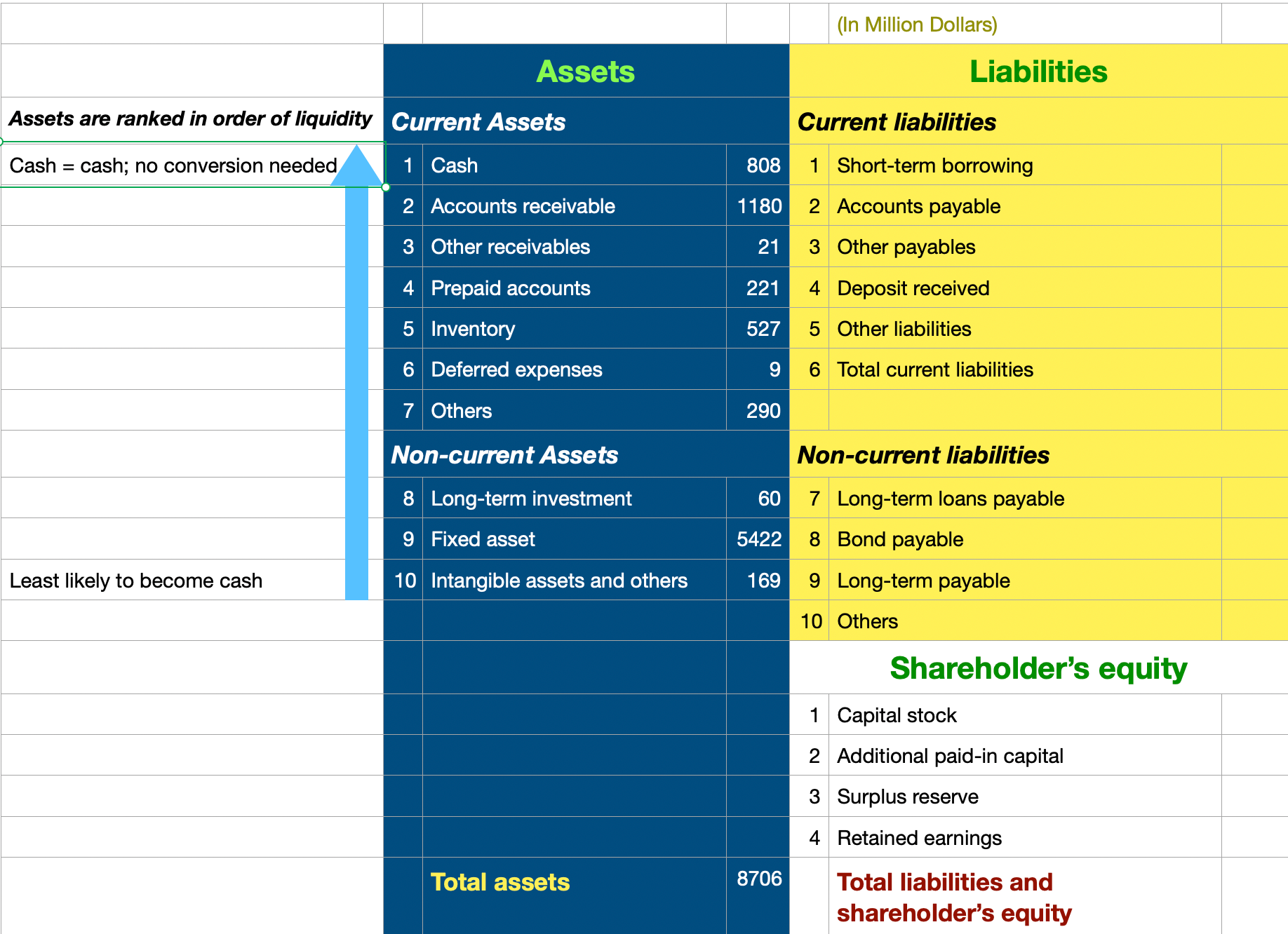

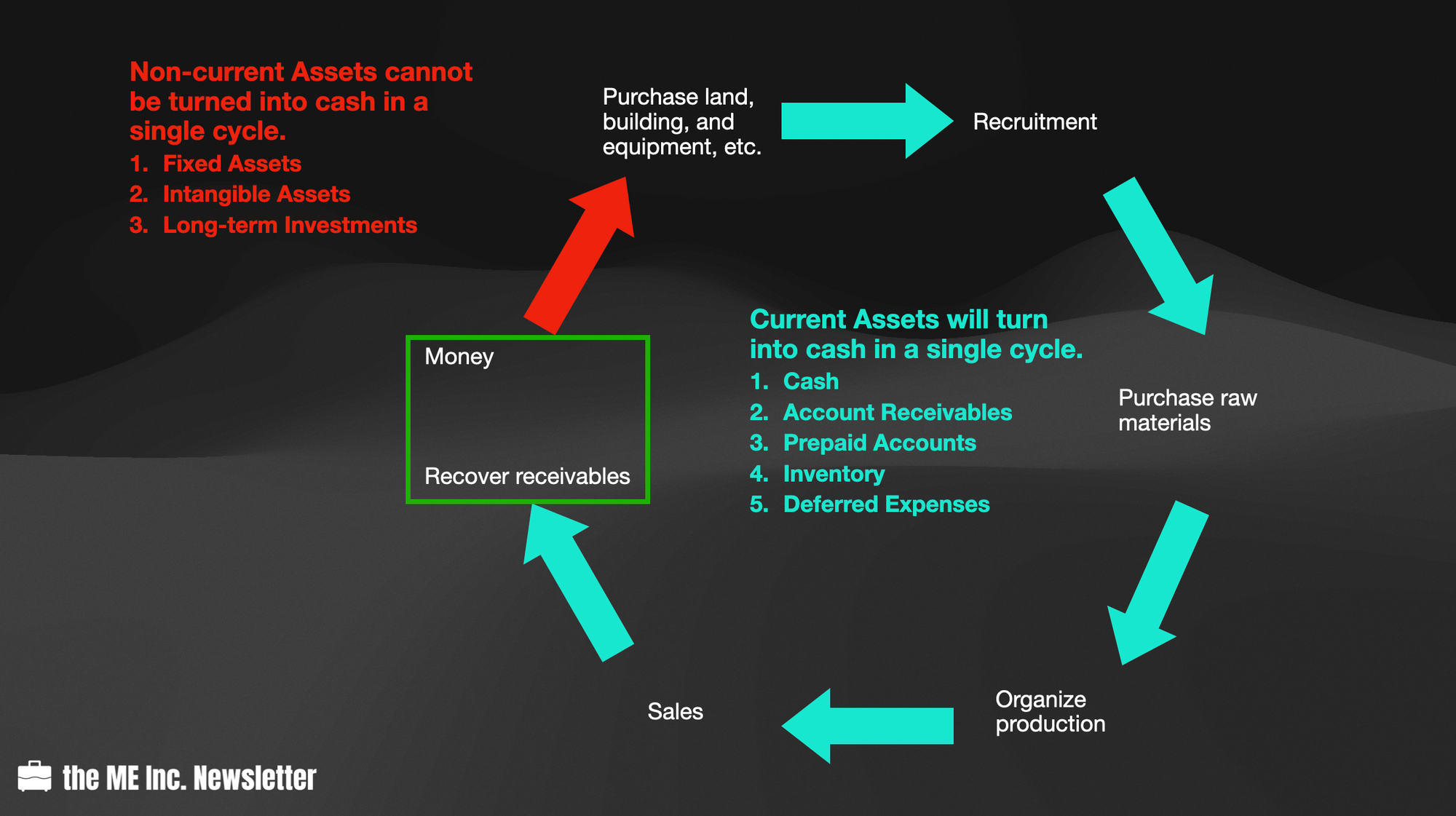

There are two types of assets, Current Assets and Non-current Assets. I will dive into their differences later on, but for now just know that in general, Non-current Assets are more durable and more valuable than Current Assets, and they are less likely to turn into cash. We will dive into Current Assets first.

Current Assets

Cash

The first item we can see is cash and cash equivalents – the good old money. Whether it’s parked in a bank or retained as actual cash in the company, it’s all cash or cash equivalents.

Accounts Receivables

Why do we have Accounts Receivables? When I sell products, the buyer may not pay me right away. This is actually quite common in the business world. Though I may not like it, but because I don’t want to lose this client, I’d rather let him pay later than never, and sometimes I will even bear the risk of not receiving the money at all. A lot of times, I’m doing this out of necessity because of similar terms extended to customers by competitors.

In this case, say I sign a contract stipulating the payment in two months, I have earned the right to receive payment at a later time (two months later). This right is called Accounts Receivable.

Other Receivables

After that there is a special item called Other Receivables. A common type of other receivables is money advanced to employees for specific purposes such as business trips. In normal business operations, a company shouldn’t have a large amount of other receivables.

Prepaid Accounts

The next item of asset is Prepaid Accounts. Unlike Account Receivables, which are money owed to me by customers, prepaid accounts are money prepaid to my suppliers in the form of deposits. For example, if a supplier has products that are very scarce to get, I’d rather pay him in advance so as to secure the materials.

Prepaid accounts give me the right to receive products/services from the supplier at a later time, making them part of the asset items.

Inventory

Inventory is pretty straightforward. It can be raw materials, half-finished products, or finished goods. For example, I might be producing metal cups and steel is the raw material that I will need to purchase. After that, I will cut them into smaller pieces (half-finished products), before I finish them into products ready for shipping (finished goods).

Deferred Expenses

The next item of asset is relatively hard to understand, which is called Deferred Expenses.

Let’s use an example. Considering that my metal cup business is booming, I’ve hired more staff to handle not only production, but also order fulfillment. These staff members will need to use stationary such as pens, pencils, and paper etc. Every time I buy office stationary, I will buy everything for about six months usage.

Now suppose I spent $60,000 on a large batch of office stationary, and then stored them in a warehouse for people to use in the next 6 months. Now the question is this: are the office stationary stored in the warehouse assets or expenses?

We know in fact assets and expenses have one thing in common, which is that both will result in cash outflows, i.e. I pay money for them. However if the cash outflow brings back something useful in the future, that something is considered an asset. If not, it’s simply an expense.

For the $60,000 office stationary stored in the warehouse, obviously they can be used in the next six months. Therefore, it’s serving some future purpose, so they should be considered as asset.

Now let’s consider this: let’s say in a month, my team will use around $10,000 worth of office stationary. By the end of the first month, I will have $50,000 worth of stationary; by the end of the second month, $40,000, etc. In this case, I’d say each month, $10,000 worth of stationary is expended, and the rest in the warehouse are deferred expenses. After six months, all $60,000 of stationary will be expended, and I should delete it from my assets.

Other than office stationary, what else could be considered as deferred expenses?

Well, my cup selling business might be doing extremely well, and I may decide to enter the retail business myself. I will pay a sum of money, say three months rent, for a retail space to display and sell my line of products to consumers. Since I pay the rent at the beginning of the first month, it should be considered deferred expenses. I may engage an advertising agency to help me promote my brand, and I might pay a six-month advertising budget in advance. If you follow this logic, you may find other expenses such as annual software subscriptions, company gym memberships… You get the idea.

Current Assets vs. Non-current Assets

For all of the asset types that we have mentioned so far, there is one thing in common: they are all liquid assets. In accounting liquid assets are called Current Assets.

There is another group of assets called Non-current Assets. What’s the difference then? Let’s pick an example from each of the 2 groups of assets to compare.

From Current Assets, let’s use Inventory as an example. As mentioned, inventory includes raw materials, half-finished products, and finished goods. Let’s take a look at raw materials. Now let’s also pick something from Non-current Assets, say fixed asset. Fixed assets include property, plant, and equipment. Now let’s pick Equipment as an example.

What is the main difference between inventory and equipment that makes the former liquid, or current, and the latter illiquid, or non-current?

Raw materials are turned into finished goods soon after they are received. These finished goods are then sold to bring back cash. In other words, raw materials, which are bought with cash, become cash again within one cycle. Equipment, on the other hand, is not expended immediately, and can take years to deplete its entire value.

If you pay closer attention to Current Assets, you may find out that all items on the current asset list are ranked by their order of liquidity, i.e. how fast they can be turned into cash. For example, why are cash and cash equivalents ranked in the first place?

Well cash is cash, and no conversion is needed. So it obviously is the first. Accounts Receivables will become cash once they are collected, so they are ranked in the second place. Inventory needs to be sold, converted into Accounts Receivables, before it can be converted into cash. So it is ranked after Accounts Receivable. This is how we rank the assets.

Non-current Assets

Now let us take a look at the non-current assets.

Fixed Assets

Fixed assets are a type of non-current assets, among which are properties, cars, computers, and so on. To be considered a fixed asset, the asset must be durable, and must have relatively high value.

Should my five-year old cup be considered a fixed asset?

Say I’m extremely frugal and I use the same cup for the past five years. Is it a fixed asset?

The answer is NO. Even though the time frame is long, the value of a cup is simply too small. A fixed asset must qualify for both standards.

Intangible Assets

Next, let’s look at Intangible Assets.

Intangible Assets include patents, proprietary technologies, copy rights, franchise license, trademark, goodwill, etc., things that are crucial to a company but do not exist in physical forms. In certain countries, it can include land usage rights, mining rights and other types of commercial rights.

Long-term Investments

Last but not least, Long-term Investments also belong to the Non-current Assets family.

For instance, the company may own shares of another company, or it may have bought government bonds. As long as I plan to hold the investment for the long term, they can be called long-term investments.

Learning about accounting is hard, but necessary, as it’s the language of business entities. Next time, let’s look at how assets are valued.