In the previous episodes of the Learning Finance series, I’ve learned the Basics of Balance Sheet, have learned the different types of assets, and how to use Balance Sheet to understand how companies work.

Every asset item is followed by a number, and that number is the value of that asset. How can I determine the value of an asset?

Historical Cost vs. Fair Value

I’m facing two choices:

- I can use the sum of money that I spent when I bought the asset at the time, i.e. the purchasing cost of the asset.

- I can use the current fair value, i.e. market price of the asset.

At first, I’m tempted to use the fair value of the asset because it reflects the real value of the asset. This may work for me personally, but if I want to one day sell the company, this method could potentially be challenged. After all, it is impossible for me to find a selling price for every single asset in the market. For example, if I have a set of equipment in the past five years, I won’t be able to find a fair value for the equipment right away.

I thought about using the price of a new set of equipment with the same model, and I could then apply a discount to the price. However, even this seemingly feasible method contains flaws.

What discount percentage should I use?

10% of the original price?

Or 90% of the original price?

Both are “discounts” applied against the fair value of the equipment, but the gap between them is simply too large, thus rendering the method NOT objective.

Accountant is a profession of prudent and conservative nature. Accountants dislike uncertainty, and when they face them, unwillingly, they’d rather err on the side of conservativeness, i.e. they would rather underestimate revenues and overestimate costs than vice versa.

After eleminating the second option of determination of an asset’s price, I’m left with the first and only option, which is to use the original purchasing price as value of an asset. Because this transaction happened in the past, there is less room for dispute.

However, even though doing so offers me peace of mind, it also creates a new set of challenges. Because the value of many assets have fluctuated over the years, the original price doesn’t reflect the current reality. For instance, if I bought a piece of land 10 years ago for 500,000 USD, the current value of the land can easily go above 50 million USD in certain countries. Yet on the balance sheet, the land is still recorded as 500,000 USD – its original purchase price.

Even though this imperfect dilemma exists, using the original purchasing price to document the value of an asset is still my best option. Most countries on this planet have adopted this method, and in accounting terms, it is called historical cost of an asset. In fact, accountants, with their conservative and prudent nature, will even go further than using historical costs of assets; that is, if there was a value increase of the asset, they would “pretend” the increase never happens, but if there was a value decrease of the asset, they would document this decrease with a deduction (what an a**hole!). So if I want to be specific, the asset pricing system is a historical cost system with deduction on devalued assets.

The goal of a Balance Sheet is to reflect the real value of assets. Because often there lacks a common, objective standard in valuing the market value of an asset, we have to use the historical cost in the asset pricing mechanism as our second-best choice.

Now we have established that in pricing assets, the historical cost system is the way to go. Is there a type of asset with a relatively objective fair value, a price that everyone is likely to agree on at any given time?

There actually is.

Financial Asset – An Exception to Historical Cost

If you think about it, one such type of asset will be public stocks. On any given day, the stock price of any public company is set by the stock market. People all over the world can see and trade on stocks, and there is little argument in the objectiveness of public stocks.

This asset category is called financial asset, among which stocks are part of. Because there exist an active market for most financial assets, people can reach consensus on their fair values. Therefore, there is no need for us (and the accountants!) to use historical costs for financial assets, since we have a better option to value them. We can simply use fair value for financial assets on our balance sheet.

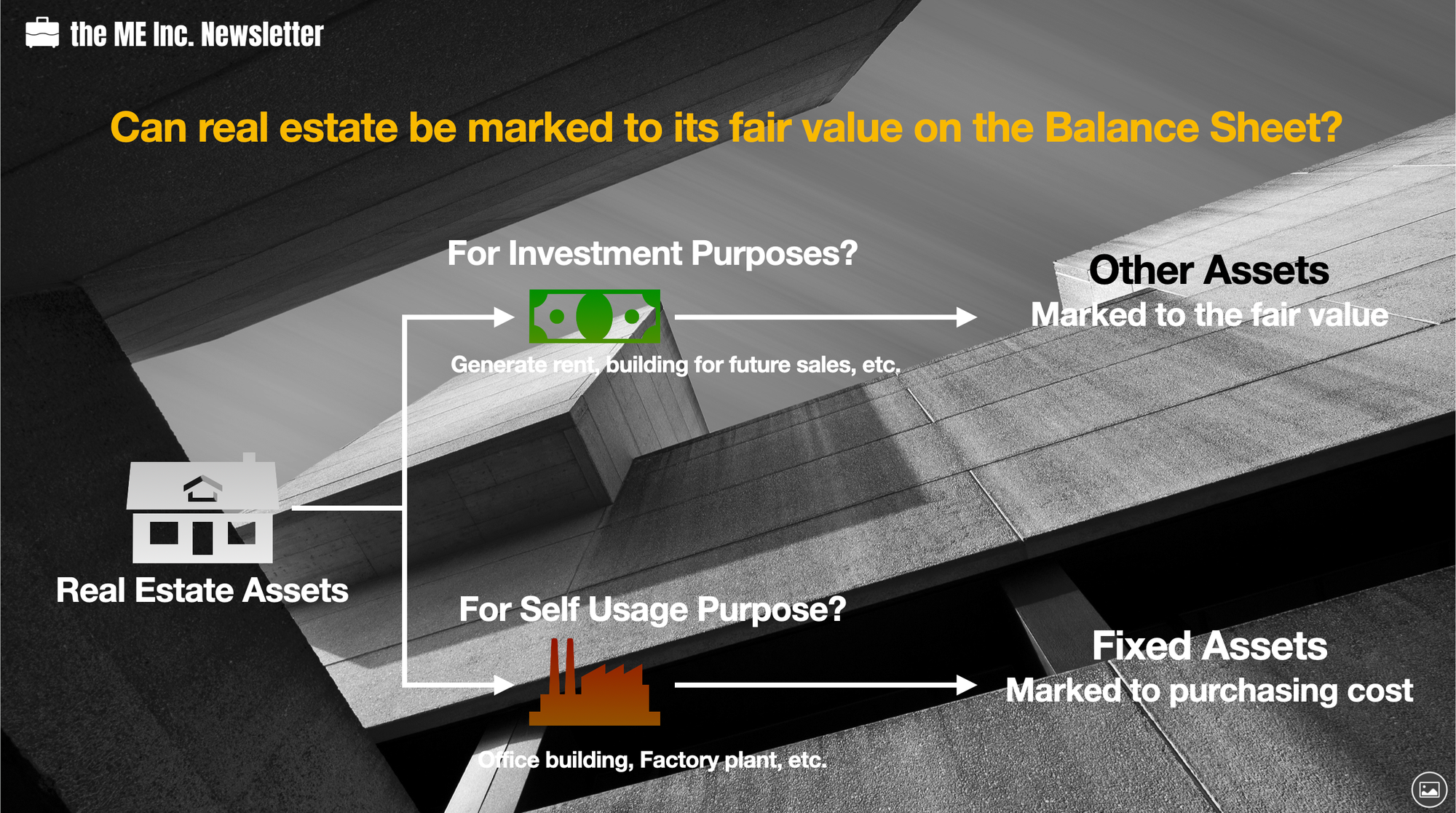

Real Estate – Another Exception (with Caveat)

Other than financial assets, is there any other asset with this character? Well, you guessed it – real estate, but not any type of real estate, only real estate intended for investments.

Next to financial assets, the real estate market is also active, thus its price objective and transparent. However, our intended usage does make a difference here; ONLY if our goal is to lease the property to tenants, or hold and sell at a later stage, etc., i.e. treating the real estate as investment, then we can use the fair value in documenting the value for the real estate. If we intend to use the property as office building or manufacturing plant, we will have to resort to using the purchasing price as its value on the balance sheet.

Understanding Economic Activities

In a nutshell, financial assets and real estate intended for investments are recorded with their fair values on the balance sheet. Other than those, most asset items are measured at historical costs with deduction when they devalue.

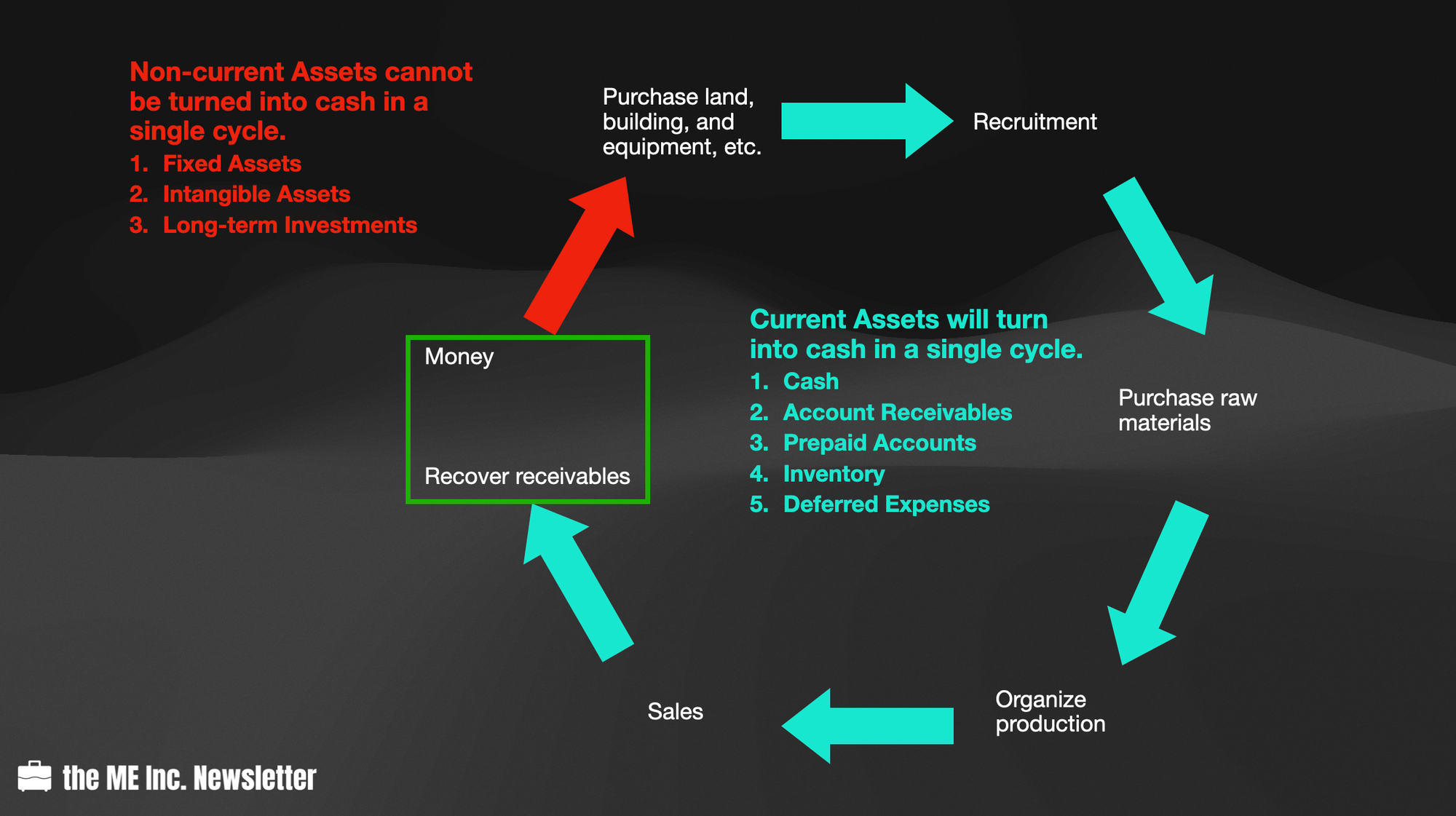

Understanding how asset values are measured can help explain why companies conduct transactions that may appear difficult to understand. For example, a company sells out one of its assets, but buys it back a week later. The asset changes very little during this week; so why does the company even bother to do all of these?

The reason that this company risks all the trouble is related to the concept of historical cost. Because of this rule, the value of this asset on the balance sheet is always equal to the purchasing price, as long as it’s not sold. To increase the value of this asset, the only way is to make a new deal, i.e. selling and buying it back.

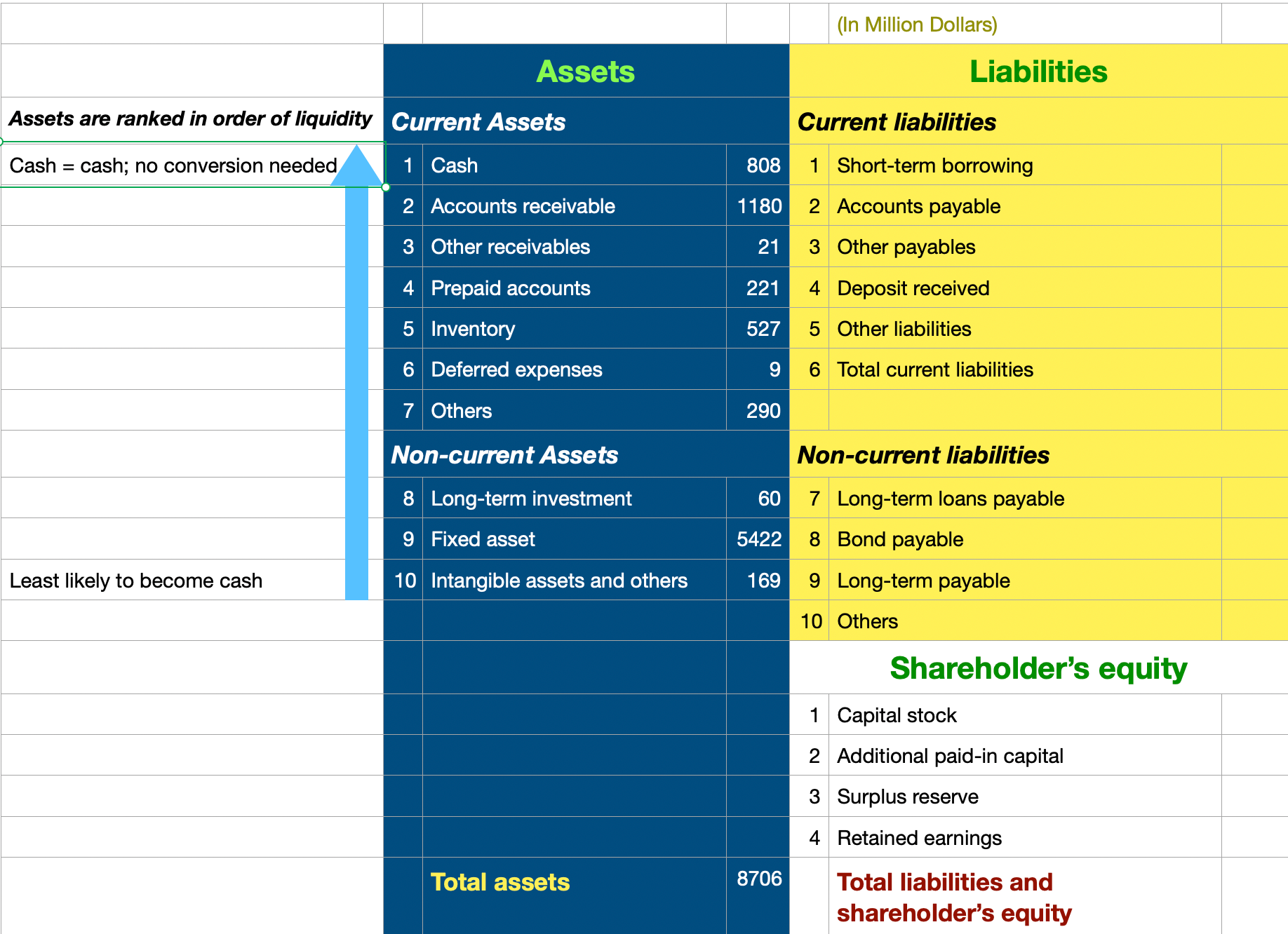

By now, we’ve learned the meaning of each asset items, the structure of assets, and how assets are valued. We have already gained a comprehensive understanding to assets – the left side of Balance Sheet. All definition of terminologies such as cash, fair value, etc. can be found from here. Next we will liabilities and shareholder’s equity – the right side of Balance Sheet.