In previous episodes of the Learning Finance series, We’ve learned Basics of Balance Sheet , different types of assets , how to use Balance Sheet to understand how companies work, and the basic rules of asset pricing system. We’ve also learned different types of liabilities, and the four components of the Shareholder’s Equity. Now we will look at what the balance sheet actually tells us, the information behind the terminologies and numbers.

Understanding Assets

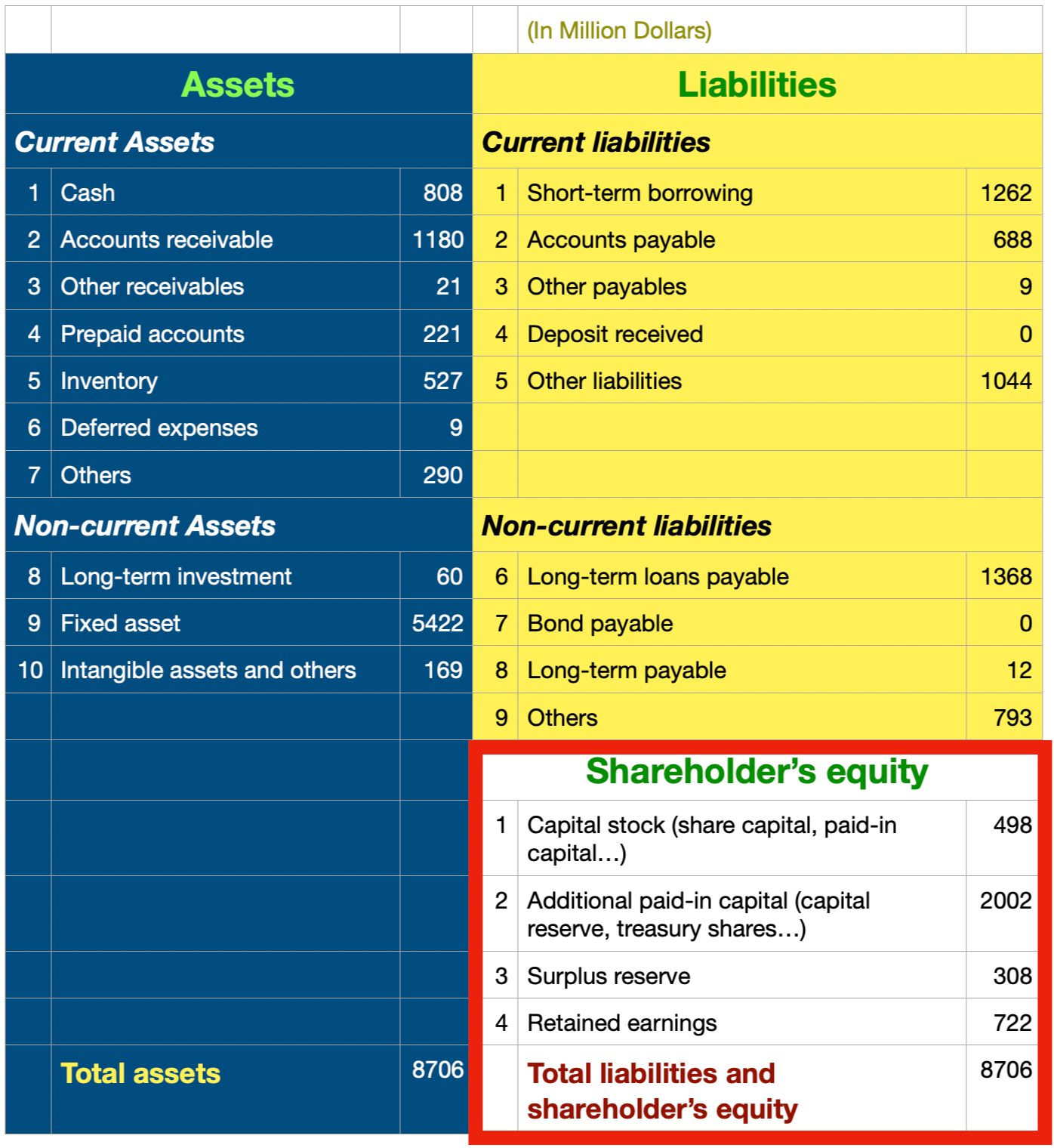

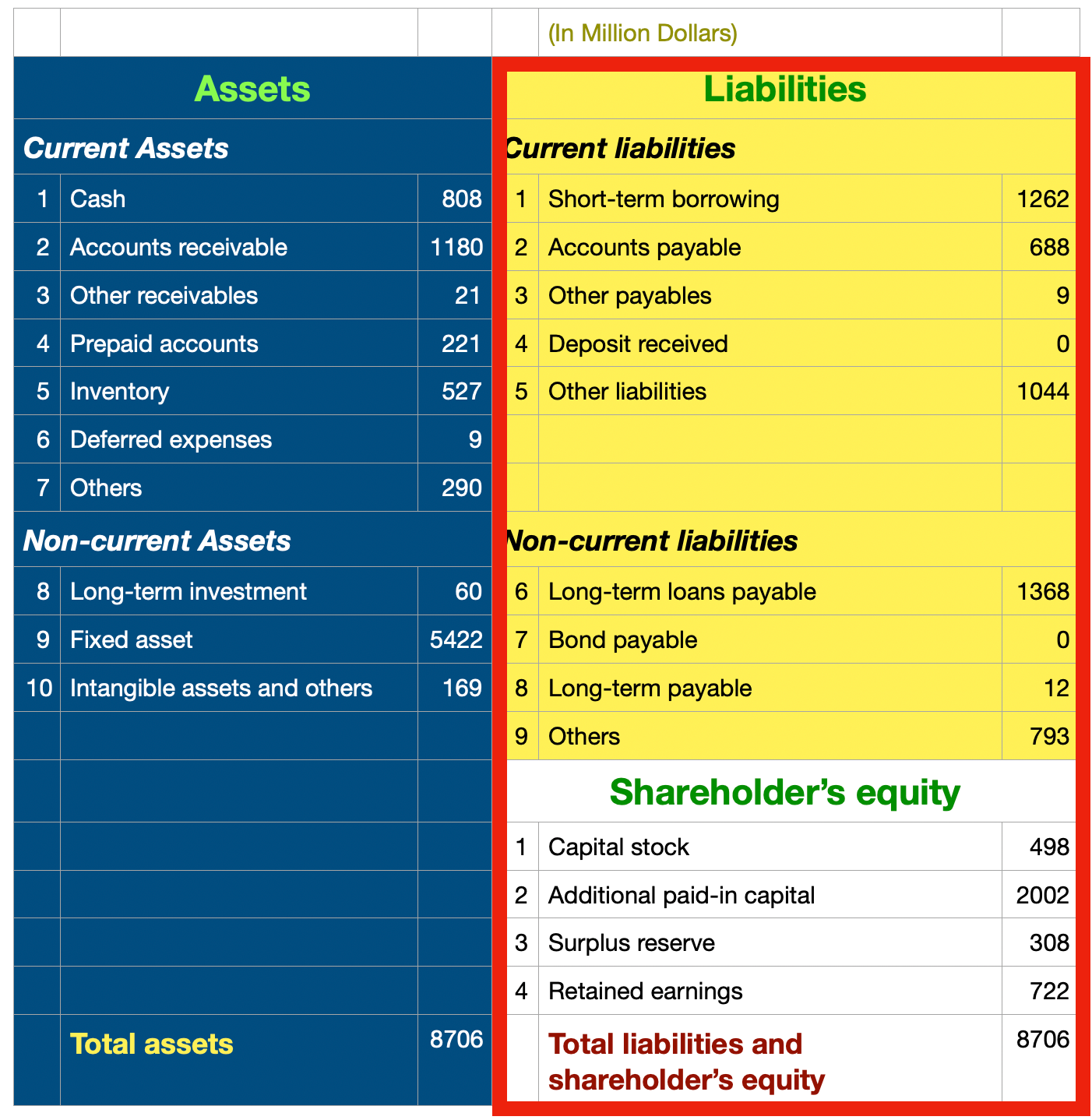

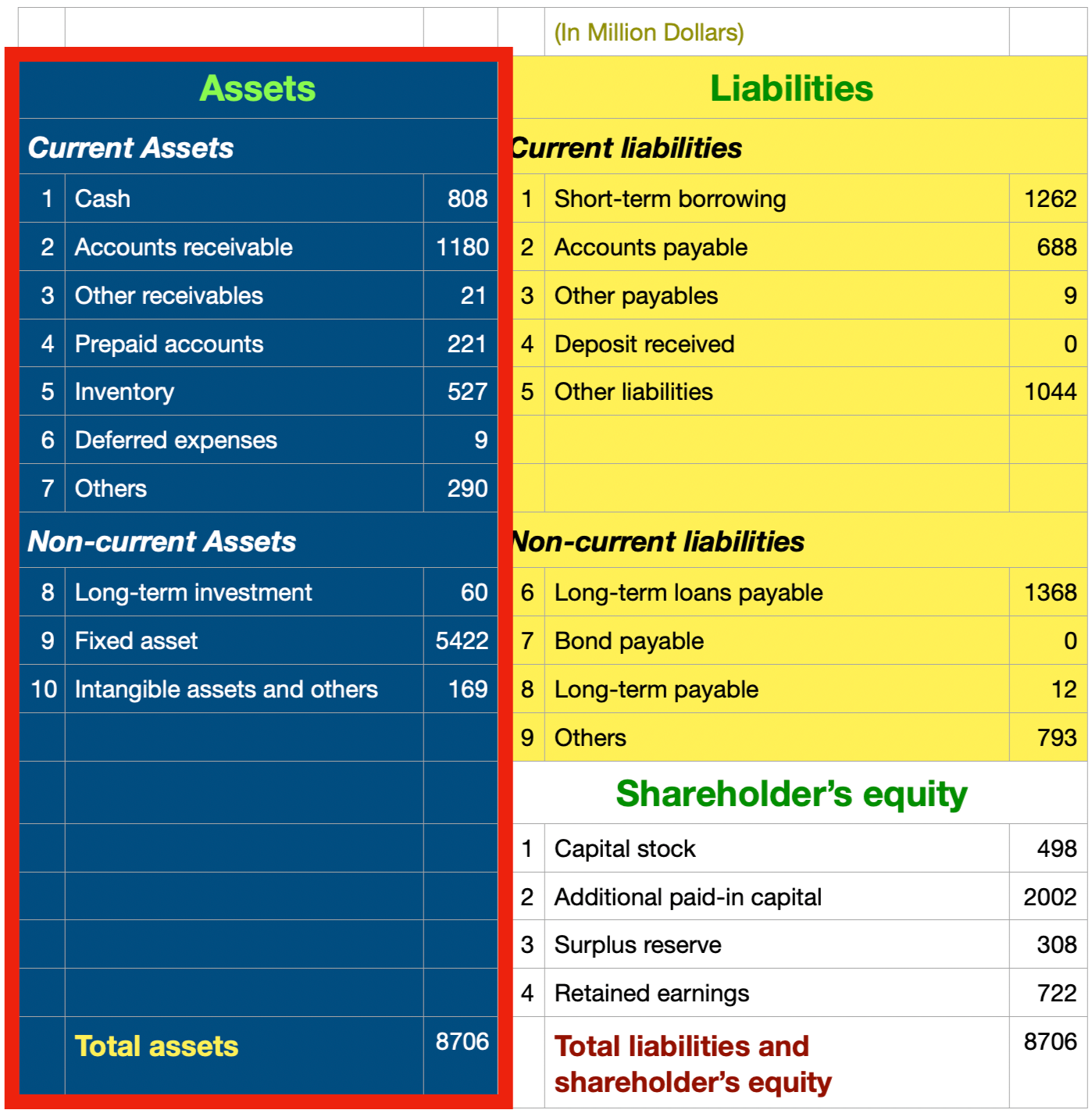

Let’s start from the left side of the balance sheet – Assets.

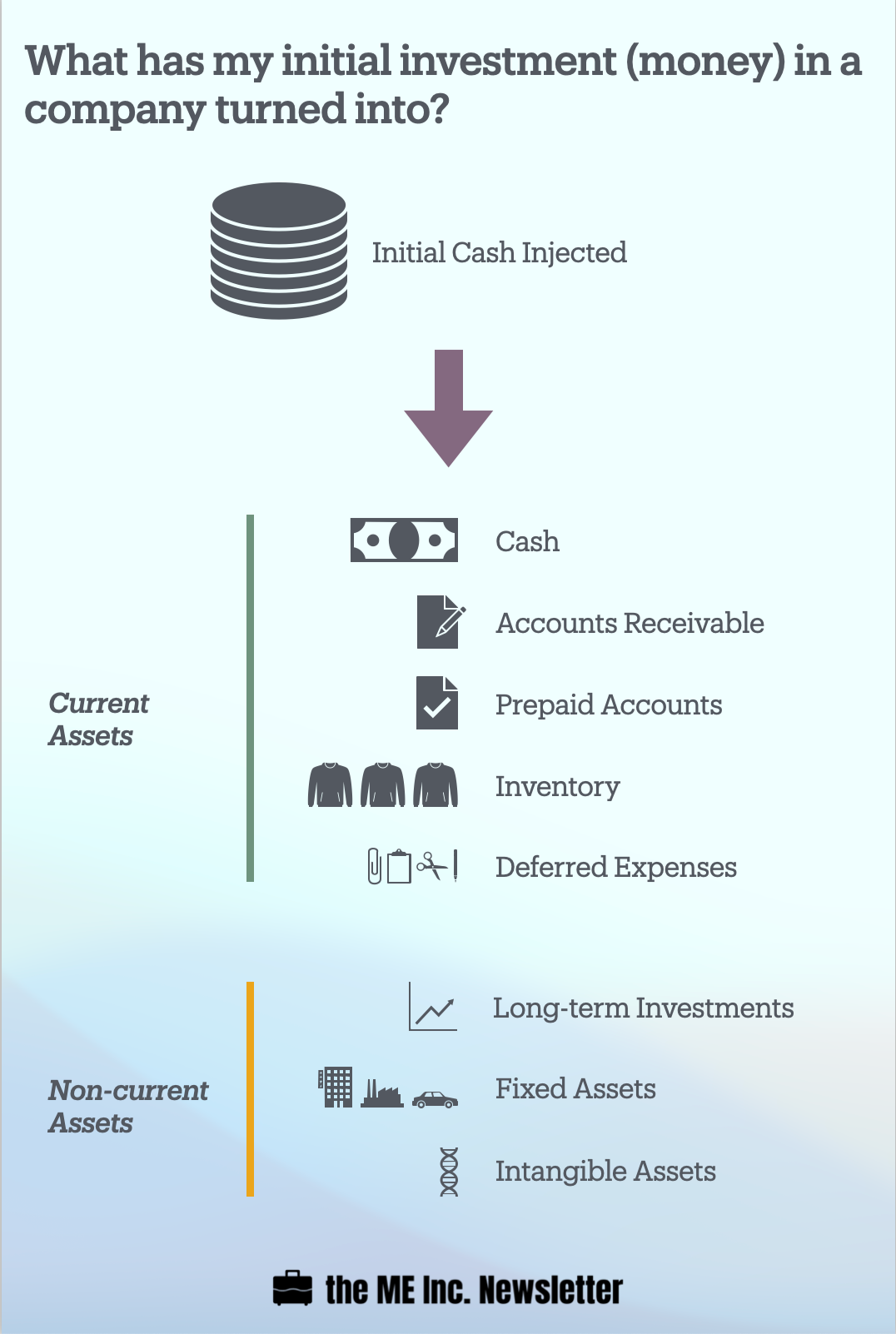

Before we ask the question “how much have I made?”, we want to make sure that the money I put into the company in the first place is safe. In other words, I want to know what the invested money has turned into.

This is what the left side of the Balance Sheet – Assets – tells us. Instead of just a pile of cash lying in the bank, some has become accounts receivable, some raw materials, finished goods , or product in progress, some factory plants, cars, computers, and office buildings, some rights of the land, patents and proprietary technology. And some are still lying in the bank in the form of cash. Essentially the Assets on the Balance Sheet tells us what our originally invested money has been used for.

Understanding Liabilities and Shareholders’ Equity

What does the right side – Liabilities and Shareholder’s Equity – tells us?

The right side tells us where your money comes from. While I might come up with a certain amount of money out of my personal pocket, I might also borrow money from the bank as loans. On top of that, I might also owe money to suppliers, customers, employees, or the Tax Bureau, etc.

Assets = Liabilities + Shareholders’ Equity

Obviously, the money raised (the right side of Balance Sheet) must be equal to the money spent (the left side of Balance Sheet). I cannot spend money I don’t have; or put it in another way, if I want to spend money I don’t have, I will have to borrow it from somebody else, thus owing them debts, and I cannot create assets out of thin air.

Assets equal Liabilities plus Shareholders’ equity is the most basic logic on the Balance Sheet, and it is also the most basic in accounting.

If you see a company’s statements do not conform to this relationship, the only possible explanation is that the statements are wrong. The equation must be obeyed at all times.

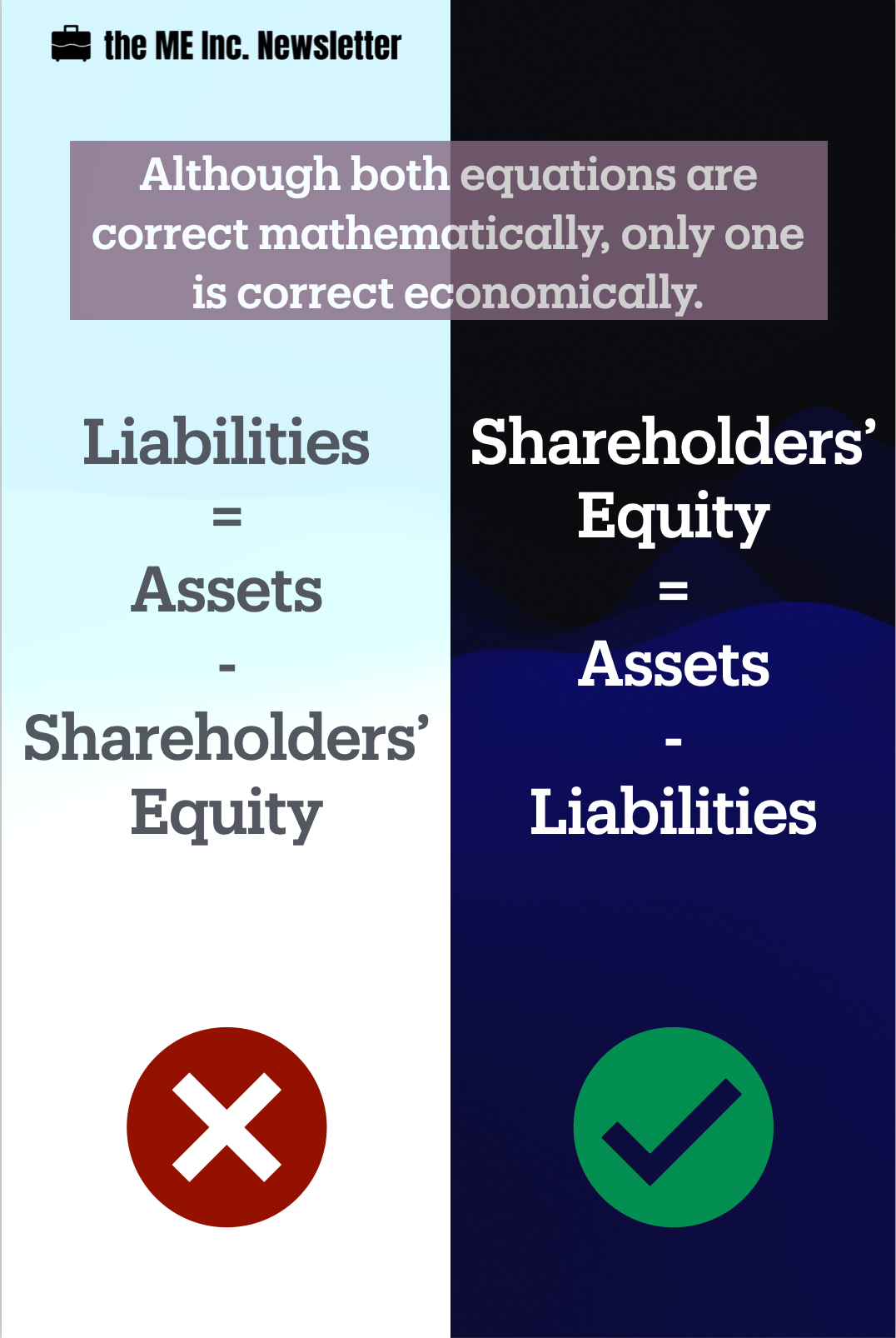

The formula that assets equal liabilities plus equity can be easily restructured into two equations:

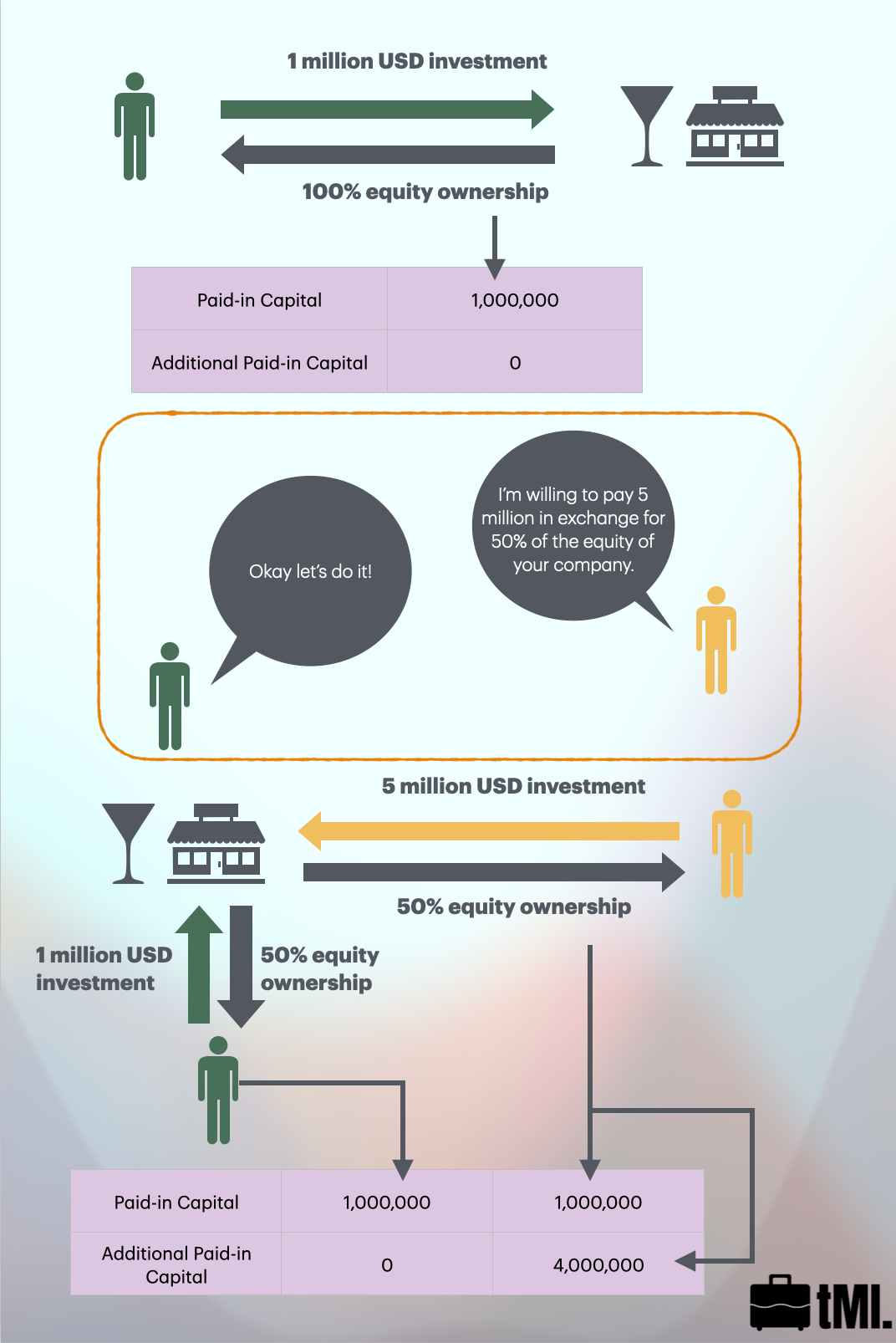

- By moving liabilities to the left, the equation becomes liability equal to the assets minus equity

- By moving equity to the left, the equation becomes equity equal to assets minus liabilities

From a mathematical point, both restructured equations are correct. But from an economic aspect, only one is correct. Which one do you think it is?

Well only the second – shareholders’ equity = assets – liabilities – is correct. Why is that?

Let’s look at the first.

The first equation means that after we allow shareholders to take back the money invested from assets, the remaining amount belongs to the bank. The owner of the company becomes the bank, which is not true.

On the other hand, the second equation means that after the company pays all the debts we owe to the bank and the rest of creditors, the remaining assets belong to shareholders. The shareholders own the company.

In other words, the shareholders own what’s left after the company repays all of the liabilities. This is called residual claims.

What if the company runs well and its assets actually have appreciated over time (great news!)?

Well the bank will not ask you to repay more than your debt for your profitable business, since the debt to the bank is fixed. Therefore, the shareholders own the asset appreciation.

But if the company is running poorly, and its assets actually become devalued over time, the bank will not grant you to repay less debt. Then you might run into a financial crisis. My debt to the bank is always fixed, so the asset depreciation has to be borne by me – the shareholder.

Then what is the ultimate goal for a company? A company should be making money for shareholders.

Recall that at the beginning, I’ve established that before I ask if I’ve made any money from the company, I want to know if my investment, i.e. my principal, is still safe, or what it has become. The balance sheet helps me answer that question. It gives me a breakdown of all items that my money has become, and has put a dollar amount behind each item. The asset items are the resources I have in running the company.

If the balance sheet tells me that the total asset is worth 100 dollars, does it mean that the company has 100 dollars worth of assets now? In the past year, i.e. having this 100 dollars at all times over the past 12 months?

Of course, the first explanation is correct. That is, the company has 100 dollars worth of assets at this particular moment. It’s like I’m taking a photo of the resources of the company, documenting what it has right now, without bothering whether it will change into in the future. Neither do I care what it looks like before the picture is taken.

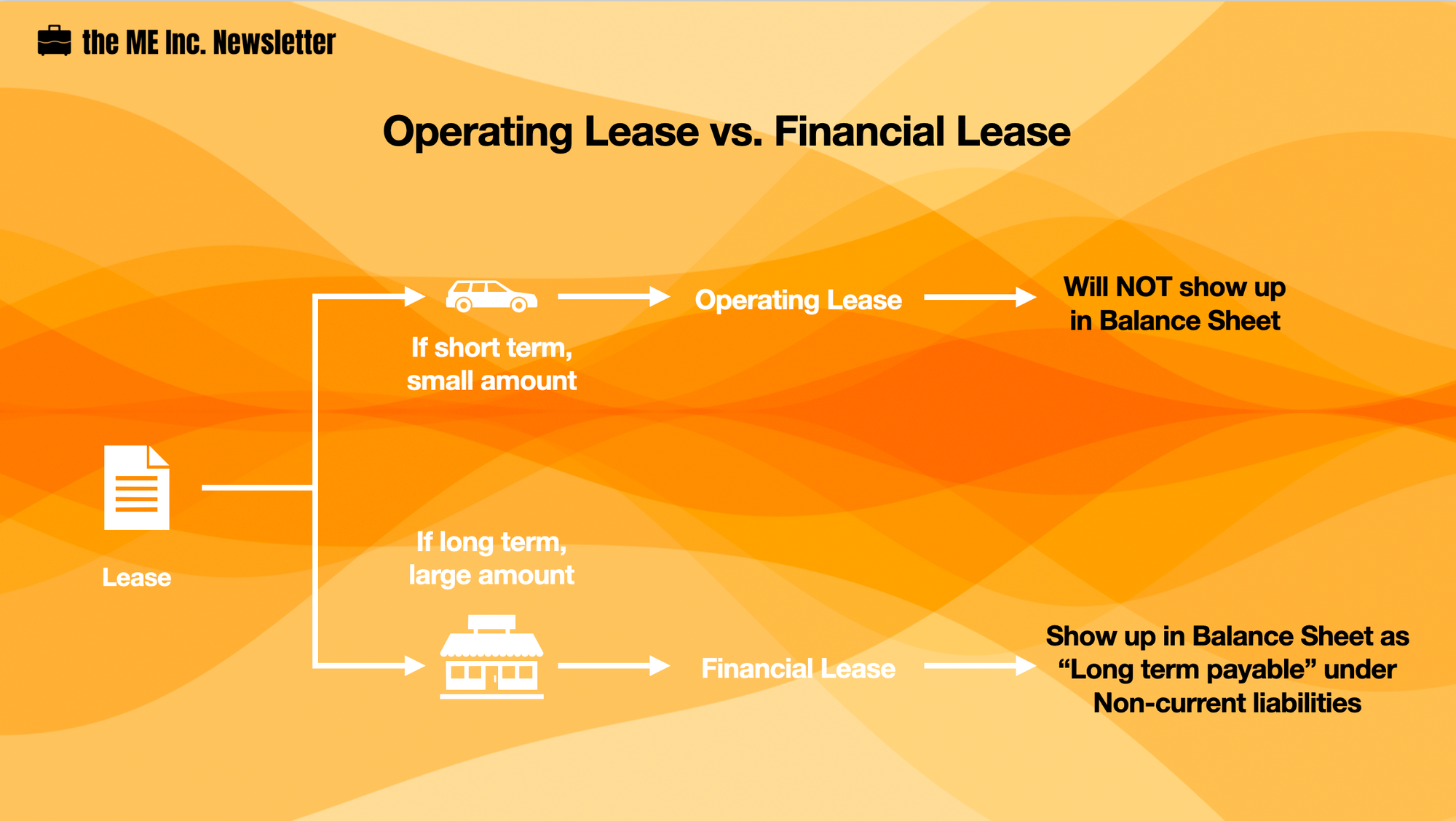

Assets vs. Physical Properties

Asset and physical property are two different concepts.

Here physical property means something tangible, i.e. physical things that I can touch. What could be an asset item that’s not a physical property?

Let’s look at the Assets on the balance sheet.

Among all asset items, we see things such as accounts receivable, prepaid account, etc., that are just my rights. Even though I do own these rights to future claims, I cannot touch such a “right”, since it doesn’t have a physical form. Sometimes I don’t even have a certificate for them like a contract. However, we still say that this is an asset.

On the contrary, sometimes we do have physical properties in presence, but they are NOT our assets.

For example, I may rent someone else’s equipment. Even though I have the right to use it during that time, the equipment is not an asset item on my balance sheet. Another example would be the products I sell as a commissioned agent. Even though these products are stored in my company’s warehouse, they are not my assets.

Relationship between Assets and Costs/ Expenses

If you recall, there is an item called deferred expenses on the Balance Sheet that we discussed previously. Deferred expenses are really assets, but they will partially get expended as time goes by. Same thing happens for fixed assets and long-term deferred expenses. They gradually wear out, and the wear and tear become depreciation.

This depreciation is a kind of cost; put it in other words, assets today are costs tomorrow. They are the same thing in different times.

Now we understand why we need a balance sheet; since our investment in the company has now become a variety of things, we want to know the value of my principal investment. And the Balance Sheet can help us do just that – it describes the financial position of our company at a particular point of time.