If someone says that he can increase the gross profit by just expanding manufacturing without selling more products, would you believe him?

He certainly sounds like a hustler. But before we jump into the conclusion, let’s take a deeper look at what the problem really is here.

What are included in the manufacturing cost?

Manufacturing cost includes raw materials, direct labor and manufacturing expenses. The first two are pretty easy to understand. Manufacturing expenses include water and electricity expenses in the workshops, and the depreciation of the plant and equipment.

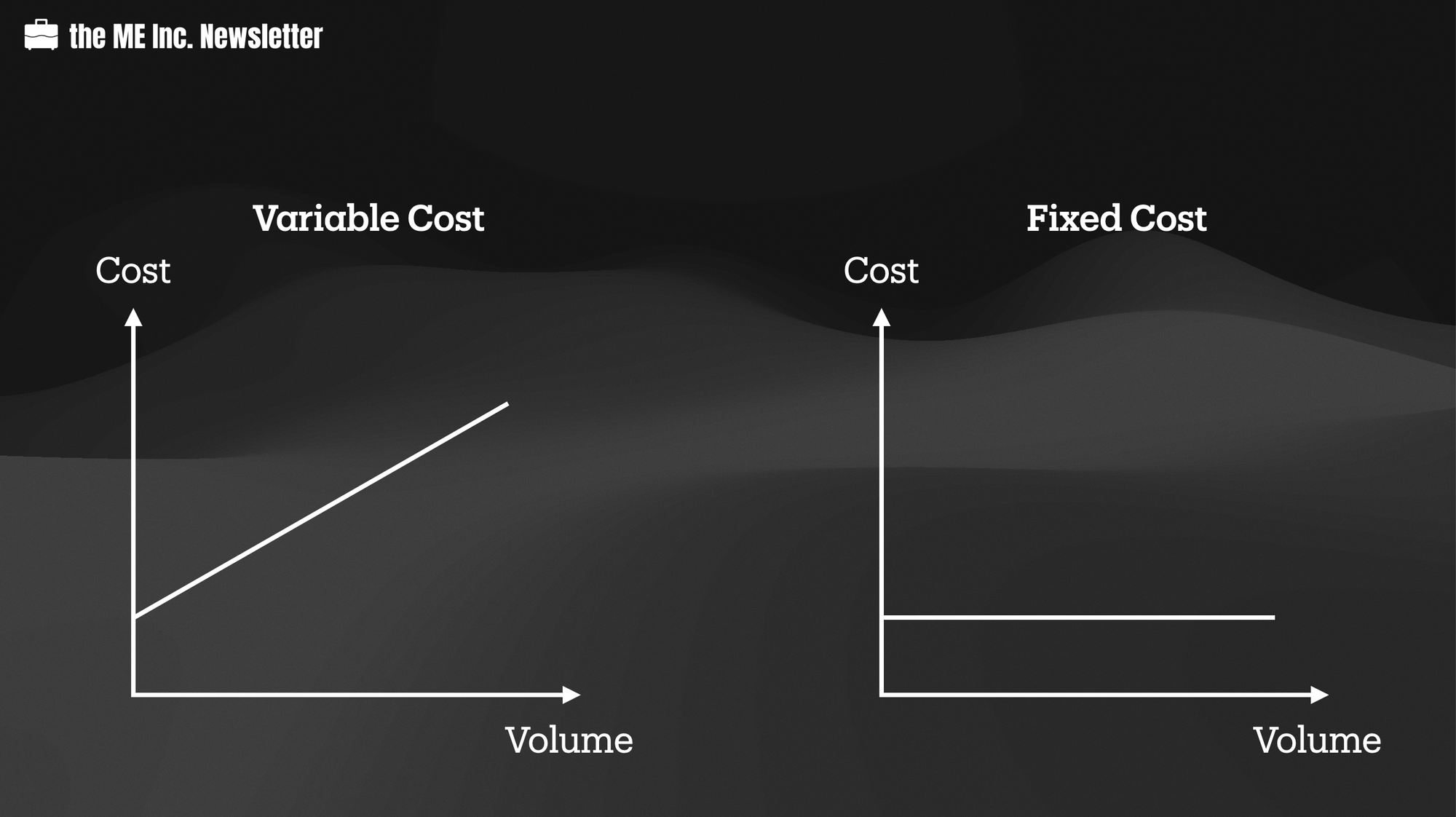

Manufacturing cost can be generally divided into two categories: variable cost and fixed cost.

variable cost vs. fixed cost

What is variable cost

Variable cost refers to costs that increase with production volume. In other words, to produce one more product, one more unit of cost occurs.

Obviously, raw materials belong to variable cost, because to produce one more product, we must invest one more unit of raw material.

What is fixed cost

Fixed cost refers to costs that stay the same no matter how many products are produced, to some extent.

It’s easy to find out that depreciation of plant and equipment belongs to fixed cost. No matter how many products are produced,

the expenses for the plant and equipment are always the same, and unless we produce significantly more products, they will not change as our plant produces more units of goods.

Direct labor

So we may say raw materials cost belongs to variable cost, while depreciation belongs to fixed cost. What kind of cost does direct labor belong to?

Well, it depends on how our company pays employees. If a fixed wage is paid regardless of how many units of goods are produced by a worker, direct labor is a fixed cost; if wage is paid per number of units produced, direct labor is a variable cost.

In practice, it is often partially fixed and partially variable.

The importance of dividing manufacturing costs into two groups

Dividing manufacturing costs into separate groups can have fundamental impact on the decision making of our company.

For example, suppose our company produces Stanley cups with a unit variable cost of 60 dollars. We further allocate 40 dollars of fixed cost to each cup. The average total cost per unit is then 100 dollars.

If a potential client places an order for 80 dollars per cup to our company, shall we accept the order?

From the surface, and from the perspective of costs, we should reject the offer because the average cost per cup is higher than the offer. We will lose 20 dollars each cup for the order. However, our alternative of declining the offer is actually losing 40 dollars:

since the fixed costs will always be there, regardless of our production status, every minute we are not producing anything is a minute of losing fixed cost. Even if my output is 0, the total fixed cost is still the same.

From this analysis, it might appears to you that accepting the order would result in a reduction of 20 dollars loss per unit (from -40 to -20). So obviously we should accept the order.

Form the above example we can conclude that it is important to differentiate variable cost from fixed cost. Now let’s look at another example.

Is higher gross profit always a good thing?

Our company produced 1000 products this year. Let’s assume this product is high-tech and high value, and it costs us 10,000 dollars of variable cost per unit, resulting in a total of 10 million dollars of variable cost. Additionally, we’ve also invested 10 million dollars of fixed cost, so our total manufacturing cost is 20 million dollars. We got really lucky and sold all 1000 pieces.

Now, let’s analyze what happened here on our financial statements.

Before we sold any product and after we manufactured all products, the 1000 units were recorded under inventory with a value of 20 million dollars, which is the cost incurred for producing the products. When the products were sold, the 20 million dollar worth of inventory got transferred from inventory (Balance Sheet) to cost of goods sold(Income Statement).

In the second year, we’ve decided to double down in this market. We predict that the market will keep growing and there will be even more demand, so we decide to produce 2000 units in the second year.

Our variable costs will increase to 20 million dollars this year as a result. Our fixed costs, on the other hand, will stay the same. Therefore, our total manufacturing costs have become 30 million dollars.

However, we’ve unfortunately predicted the market trend incorrectly, and have failed to sell the 2000 units of products. Instead, sales this year stay the same as last year at 1000 units. The other 1000 units of products stay as inventory in our warehouse.

Let’s do some analysis here. The 30 million manufacturing cost is originally recorded in inventory. At the time of selling the 1000 units, this portion of inventory is transferred from inventory to cost of goods sold. Because we’ve produced 2000 units and only sold 1000, exactly 50% of inventory will be transferred into cost of goods sold, which is 15 million dollars. And because our sales are still the same at 1000 units, assuming our unit price stays the same, our gross profit actually increases because of the lower cost of goods sold! To be exact, 5 million dollars more!

This result can be baffling to many. If we produce more products but fail to sell more, our gross profit is indeed increased. But any person with some level of common sense will know having too much inventory is bad, not good, for the company.

The explanation

By reading this post, you will be able to understand the reason, which is that because the fixed costs stay the same in both years, the per unit fixed cost got reduced with the increase of manufactured products. And because only 50% of products are sold, only that portion of fixed costs got transferred to cost of goods sold. The other 50% stays as inventory, until they get sold in the future. So even if our revenue stays the same, producing more units of products can actually increase our gross profit.

By now you might have found a problem: normally we think that our firm is more profitable if the gross profit is higher. However

the firm in the above example predicts the market trend incorrectly in the second year, and manufactures too many products, resulting in over-production. If you are asked to judge how the firm’s performance is in the second year, I am sure that you would say it is poor. However, its gross profit is indeed higher.

The conclusion is that we cannot simply take an increase in gross profit as sign of better performance. Growth in gross profit should be interpreted together with the value of finished goods inventory. If gross profit and finished goods increase simultaneously, the increase in gross profit does not necessarily mean a better performance, and we should take it with a grain of salt.

For the same reason, if gross profit and finished goods decrease simultaneously, it could mean that the company is selling lots of finished goods from the inventory, which is almost always a good thing.

If you have read my last post, you know that our fictional company has been created, and has procured land usage right and fixed assets such as manufacturing plant, equipment, etc. Now the company is ready to produce.

In this episode, we will keep following the economic activities and learn how they affect our balance sheet.

Raw Material Procurement

The first thing I want to do is to purchase raw materials. By negotiating with a supplier, I made a deal to purchase 24 million dollars of raw materials, and would need to pay 16 million dollars for the time being. The supplier agreed to give me a few months for the other 8 million dollars.

Raw materials belong to inventory, so I’ve accrued 24 million dollar worth of inventory under assets. I’ve paid out 16 million dollars of cash, so my cash position is reduced by 16 million, to 8.5 million dollars. I also owe the supplier 8 million dollars of accounts payable, which is a type of current liability.

After this economic activity we can see that our assets are increased by 8 million dollars, and our liabilities are also increased by 8 million dollars. The basic formula that assets equal liabilities plus shareholders’ equity is still followed.

Manufacturing Process

The raw materials will not produce products themselves. Instead, we need people to operate our equipment to manufacture those raw materials into finished products. To make it happen, our company paid another 12 million dollars in cash for the employee wages, water and electricity costs, etc. During the manufacturing process, our inventory – 24 million worth of raw materials – is also reduced to zero, assuming that we’ve used up all of them. The total cost of producing our products – 36 million dollars – will be recorded as finished goods, which are a type of inventory. Thus, our inventory actually increases from 24 million to 36 million dollars.

Raw materials, products in progress, and finished goods all belong to INVENTORY.

(You may have also noticed that we actually don’t have 12 million dollars of cash to spend on employee wages, water, and electrcity. Let’s imagine that we’ve struck a deal with the power company, which grants us another six-month relief for the 4 million dollar worth of electricity bills.)

After this, we’ve accrued an additional 4 million dollars of accounts payable, and cash is reduced to 500,000 dollars. Our inventory, as mentioned before, increases from 24 million to 36 million dollars.

The 36 million, including 12 million labor and utility costs, and 24 million raw material costs, are the manufacturing costs for our products. Intuitively, you may think of recording costs in the Income Statement. However, it is actually recorded under Assets as inventory.

What is the deal with that?

Well, if you recall in Income Statement, the item directly underneath Revenue is cost of goods sold. When we sell our products and obtain revenue, we automatically lose ownership of the inventory. In other words, we should only record the portion of finished products SOLD here. We can spend all the money on raw materials or on manufacturing, but if none of the products are sold, they don’t appear as cost of goods sold in Income Statement.

💡

Cost of goods sold is a subset of manufacturing cost. It represents ONLY the portion of manufacturing cost that’s already SOLD.

After we make a sale, our inventory actually decreases, because our finished goods decrease. We either increase our cash position or accounts receivable position, and should be able to increase our assets because of the sale.

Now if someone says that he could increase gross profit by just increasing manufacturing without increasing sales, would you believe that? We will analyze this case in the next episode.

As an entrepreneur, it is NOT our job to prepare the book, i.e. the financial statement. We can always outsource the job to an accountant.

However, what we cannot outsource is how to deal with the numbers given back by the accountant. Will you be able to make the right call when allocating resources based on your judgment?

To improve our judgment in resource allocation, building a financial mindset will be crucial. Once you get it, you will understand how economic activities affect financial statements, but furthermore, you will understand how different factors play their roles in value creation for a company. In other words, once you get the financial mindset, you can use finance as a language to understand how values are created in operating a company.

In this episode, we will discuss the preparation of financial statements in order to help us understand how economic activities affect financial statements.

Let’s start from the beginning of a company’s life cycle – the creation of a business.

Before Creation

Before we invest any money into the new company, the balance sheet is blank. There is no asset, no liability, and no shareholder’s equity.

Capital Injection

As the sole shareholder of the company, I’ve decided to inject 32 million dollars. At this point, the company has only one thing on the balance sheet – money. On the balance sheet, 32 million dollars worth of cash will be recorded under Assets. At the same time, 32 million dollars worth of equity will also be recorded under Shareholder’s Equity, balancing the financial statement.

At this point, there are only two items on the balance sheet, cash and equity, with the exact same value. The fundamental logic – assets = liability + shareholder’s equity – still applies.

Getting a Loan

After my initial capital injection, I’ve decided to take out a loan from the bank. The bank, generously, has granted a total 51 million dollars, and wired the total amount directly to the company’s bank account. All of a sudden, the total cash amount is increased to 83 million dollars.

Because the money is borrowed from the bank, there should be a 51 million dollar worth of liability under short-term borrowing, assuming that it is a 12-month loan.

After this, there are three items on the balance sheet by now, i.e. cash, short-term borrowing, and equity. The basic logic still applies.

Fixed Assets Procurement

By now, all capital is in place for the company. The company then gets ready for doing business, and the first thing is to purchase some fixed assets (assuming it’s in an asset-heavy industry such as manufacturing). The company then spends 57 million dollars on building a manufacturing plant, equipment and office furniture procurement, etc.

Our cash is then reduced by 57 million dollars, to 26 million dollars. At the same time, we’ve gained 57 million dollar worth of fixed asset.

The total of assets is still the same – 83 million dollars – but the percentage of each is changed.

Land Usage Right Purchase

The company also purchase a land usage right from the government for 1.5 million dollars, and because land usage right is an intangible asset, we will deduct the cash amount from our cash item, and put 1.5 million dollars under intangible assets.

Similar to the previous economic activity, the asset total is still unchanged, but our percentage of cash is once again reduced.

By now, the company has made all the necessary investments in infrastructure. Next it will start manufacturing, which will further change our financial statements. We will continue our learning in the next episodes.

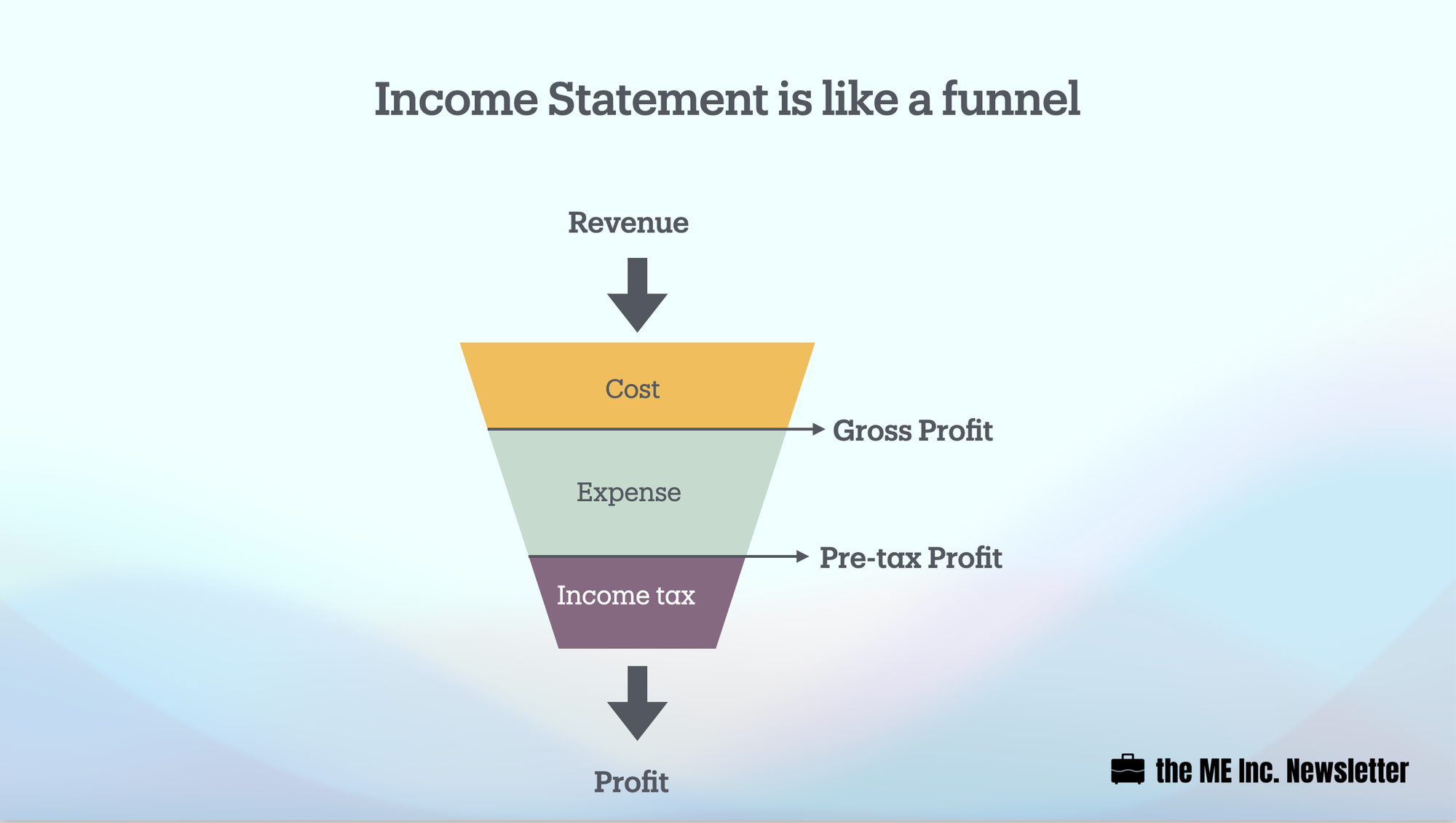

You put revenue in from the top of the funnel, and profit comes out from the bottom. In between the top and the bottom, costs and expenses will be taken out.

The sequence of taking out the costs and expenses is also pretty straightforward. First of all, we deduct the cost of goods sold from the revenue, the cost that is directly related to doing the sales. Doing so will gives us our gross profit. Then we need to subtract all kinds of expenses, some of which are related to doing the sales, and some to managing the company.

On the balance sheet, the fundamental logic is “asset equals liability plus equity”.

What is the fundamental logic on the income statement?

Well it is actually quite simple: when we subtract all the costs and expenses from revenue, what’s left is profit.

What information does the income statement tell us?

First, by looking at the net profit, we can conclude whether the company is profitable in the past fiscal year. If net profit is positive, the company is profitable; if net profit is negative, the company is not profitable.

But because income statement lists the company’s operating profit separately from its non-operating profit, we can, to an extent, conclude how predictable the company’s future profitability is.

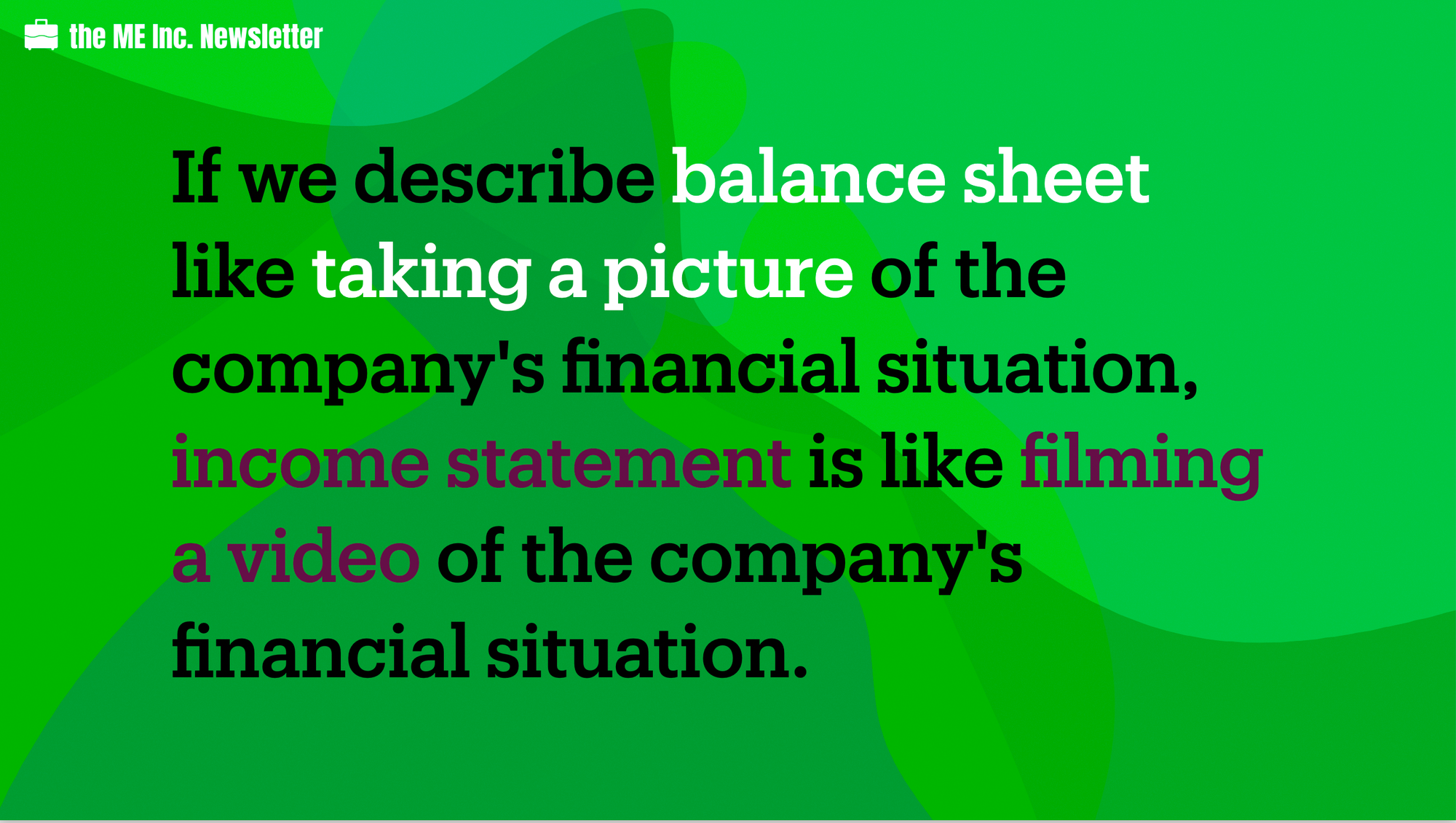

Balance sheet shows a company’s asset, liability and equity values at a certain time point. Different from the balance sheet, everything on the income statement is by a period. If we describe balance sheet like taking a picture of the company’s financial situation, income statement is like filming a video for the company’s financial situation.

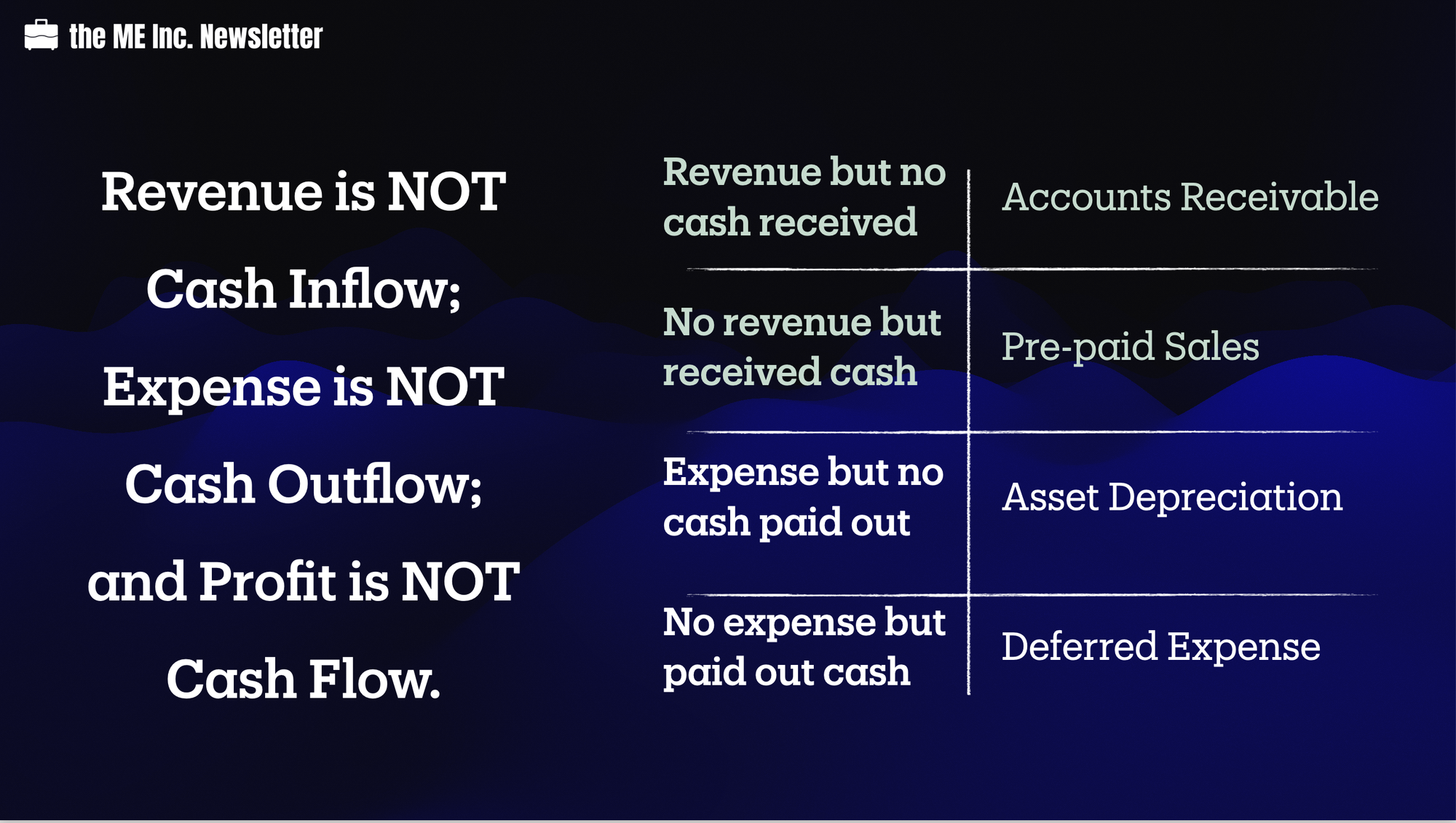

Does revenue equal cash received?

There is still one important concept to clarify: does revenue equal cash received?

The answer is NO. Revenue does not equal cash received. And Expense/cost does not equal cash paid out.

First, let’s look at the first statement – Revenue does not equal cash received.

Under what circumstance will we have revenue but do not receive cash? Well, you may have guessed it – when we make a sale on accounts receivable. Even though we have sold our product and got the revenue, we will NOT actually see any cash until the accounts receivable is collected.

On a second note, the reverse is also true: cash received does not equal revenue.

One possible situation is when we get pre-paid sales. We’ve sold the product but have not delivered yet, but have already received the money.

After that let’s look at the second statement – Expense/cost does not equal cash paid out.

Under what circumstance will we have an expense but have not paid out cash?

One common example is asset depreciation. Depreciation is used to describe the decrease in value of fixed assets. When calculating depreciation, we don’t need to pay cash to anybody, and it only shows on the books. We have to record such depreciation as an expense on the income statement, but we actually don’t need to pay cash to anybody.

On the contrary, when do we have cash outflow but no expense?

When we pay a large sum of money for an asset that’s for the future operations of the company all at once, that lump sum should NOT be accounted as expense for that period alone. Instead, if we think the asset can be used for a certain period, a portion of the total cost should be accounted each year. We’ve already visited this concept before in the balance sheet episode, and it is called deferred expense.

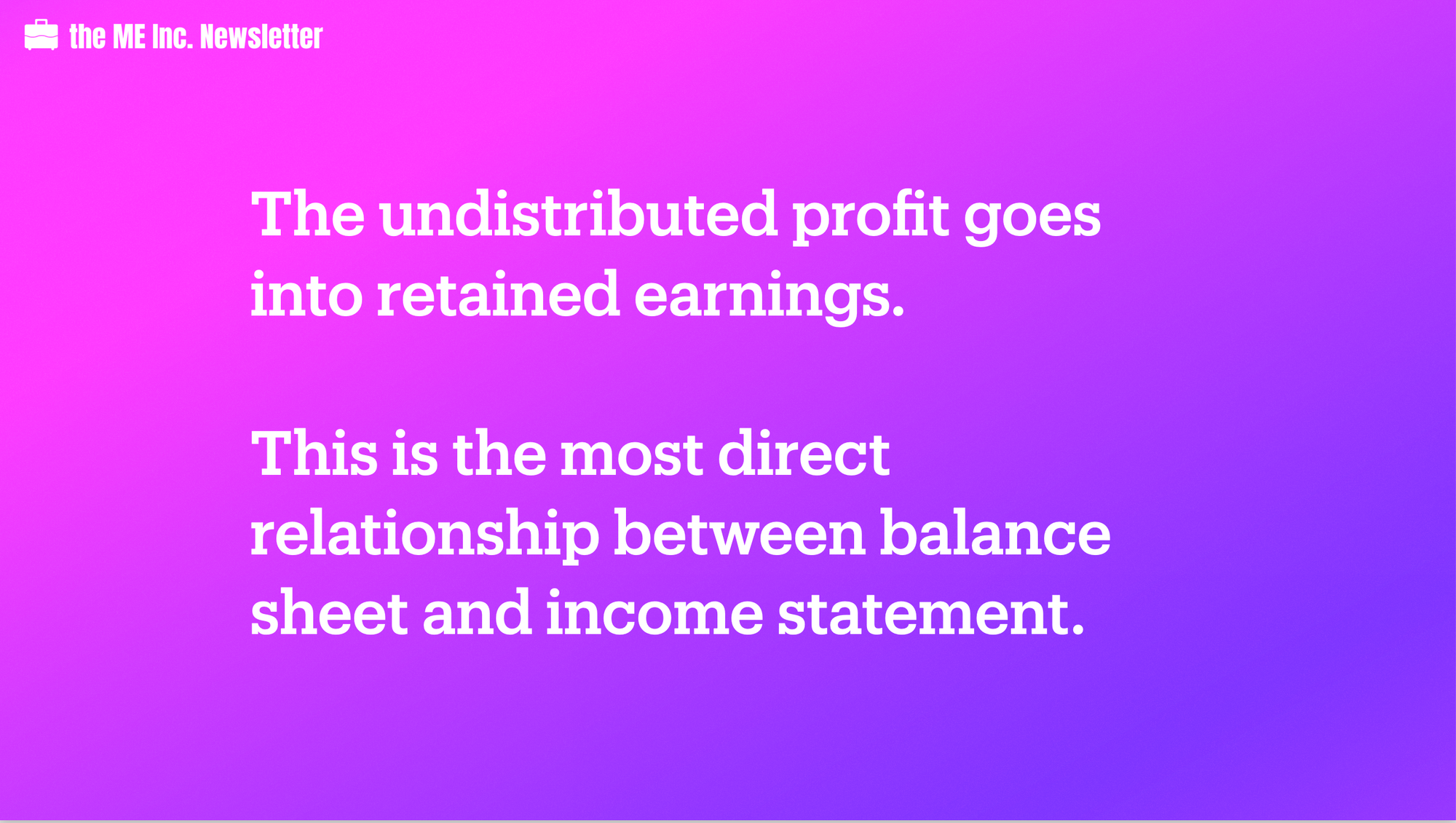

Relationship between balance sheet and income statement

Although individually, balance sheet and income statement have already provided us with lots of information on a company’s financial performance, the combination can often reveal insights that far exceed an individual statement does.

Let’s say if a company makes a net profit of 5.2 million dollars this year, and has decided to distribute 1 million in dividends to shareholders. The remaining profit is 4.2 million dollars.

This 4.2 million should go into our balance sheet to increase the retained earnings. In other words, it increases the value of shareholders’ ownership rights.

This is the most direct relationship between balance sheet and income statement, and this relationship is connected by retained earnings.

Of course, later we will see another financial report cash flow. After we learn cash flow, we will find that the three financial reports make up an interesting combination. It will help us paint a full picture about the company’s story.

In the balance sheet, we’ve already learned what our investment has become, and we can see if our initial investment’s value is guaranteed. But this is not enough – we want to know if we are making a profit.

That’s when the second financial statement comes in – Income Statement.

Within this process of money – things – money, the part that’s directly related to making money is when I sell my products. Once my products are sold, revenues are generated. Obviously, the revenue I receive comes at a price. When I sell a product, it no longer belongs to me; what I have lost here is the cost associated with acquiring the product.

In addition, in order to run a company I will need to pay for all kinds of bills, bills to keep the lights on, etc. These are called expenses.

As you can see, knowing if my company is making a profit is not easy. That’s why I need a report – the Income Statement– to help me understand it. Now, let’s see what a Income Statement looks like.

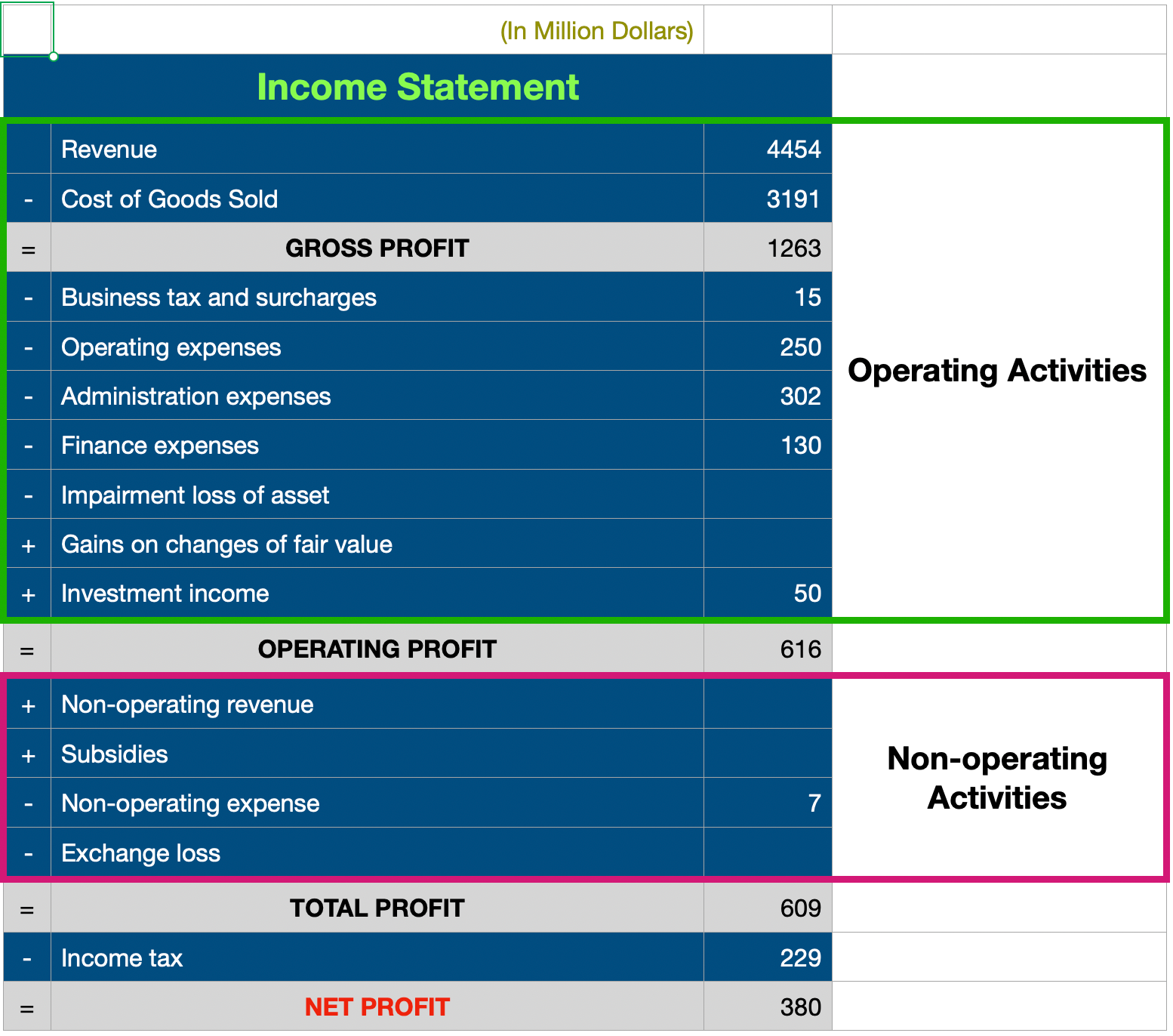

An income statement starts with the revenue and ends with the net profit. In between you will find numerous costs and expenses. The top of the income statement describes money generated or spent from the company’s operating activities, i.e. its main business operations, and the bottom describes that from the company’s non-operating activities. After going over this post, you will be able to understand all of them.

Operating Activities

Cost of Goods Sold

The first line item is revenue. When I sell a product, I will get revenue associated with the selling of the product, but I also lose the ownership of the product, therefore the cost of goods sold.

A commonly heard concept is gross profit. But what is gross profit? Well, revenue minus cost of goods sold is gross profit.

Business tax and surcharges

Now let’s look at the next item — business tax and surcharges.

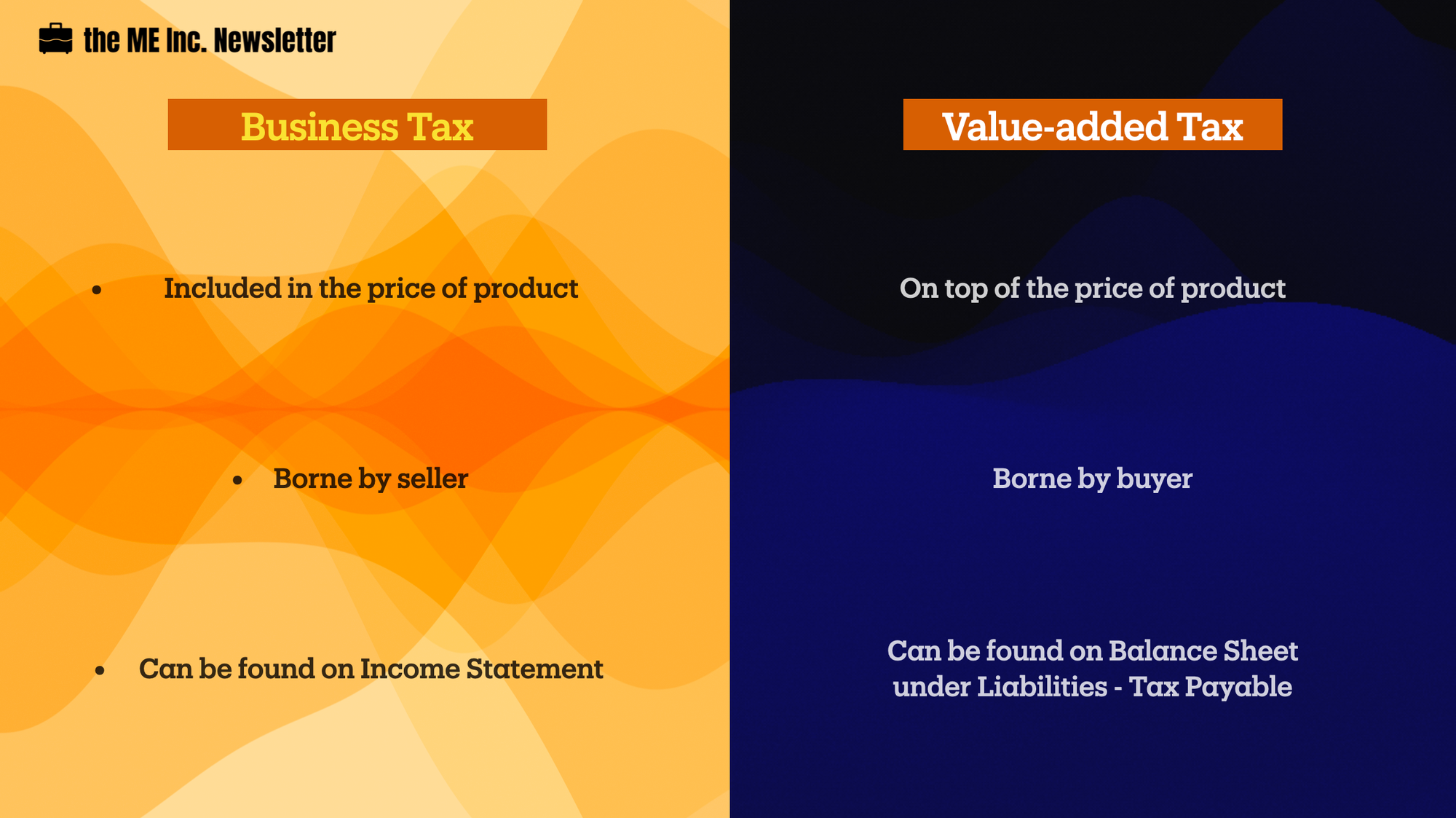

Generally speaking, there are several common corporation taxes, i.e. business tax, value-added tax (VAT), and income tax. Taxation is a complex topic individual to each country, so not everything you find here will apply to your home country. For example, not all countries have business tax and VAT, and some countries have additional types of taxes. However, you should get a basic feeling of what fits where after this.

Income tax should only apply when there is income, or profit. Therefore, it should appear only after total profits. When I subtract income tax from total profits, I will get my net profit.

Business tax and surcharges means if I am operating a business, regardless of whether I make a profit or not, I will need to pay for the tax and charges. Categorically speaking, these kinds of taxes are called turnover taxes.

Both business tax and value-added tax are turnover taxes.

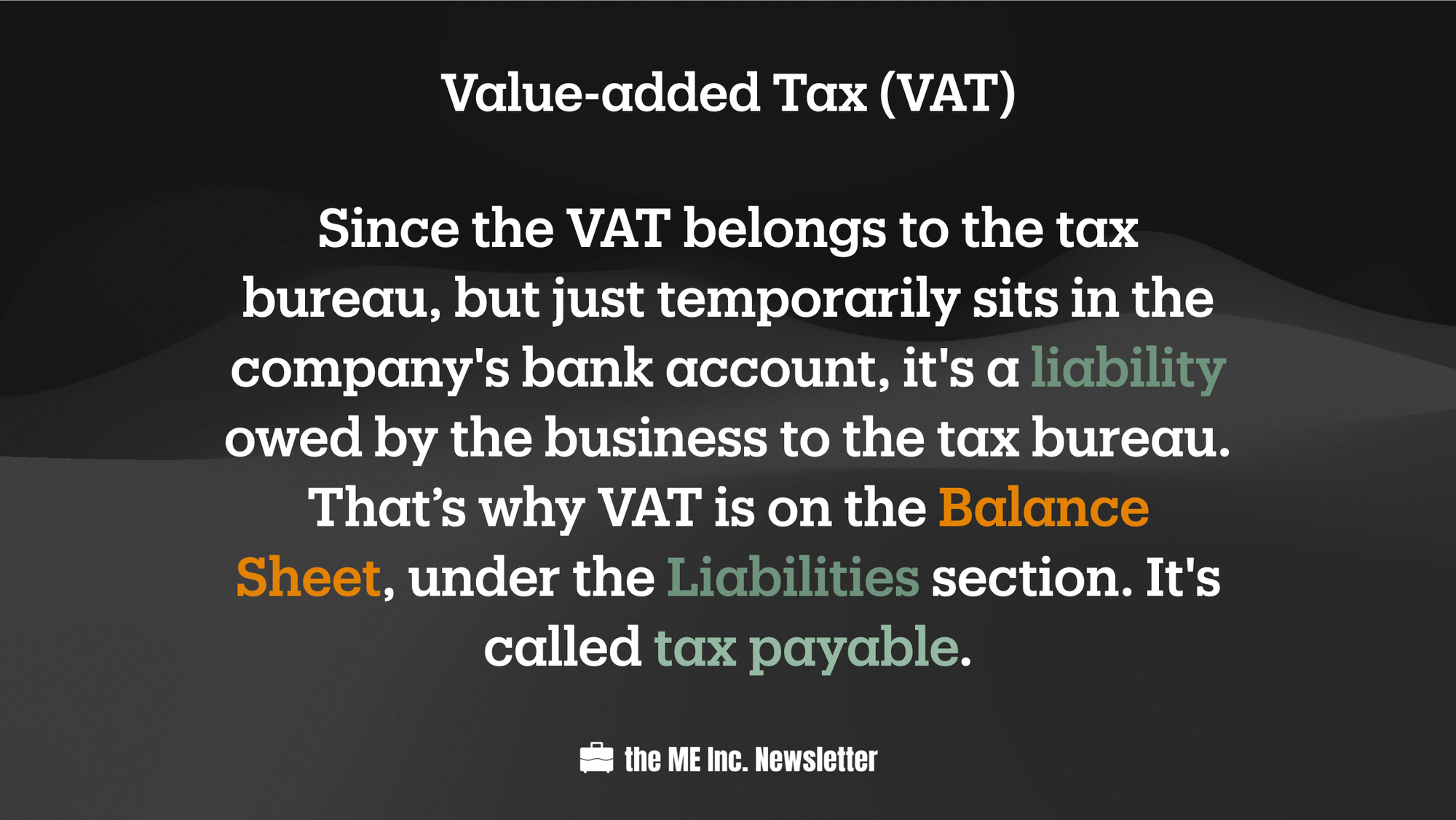

However, you may have noticed that VAT is nowhere to be found on the Income Statement. That’s because VAT doesn’t belong here.

Now why is that? Why is business tax on the income statement, but VAT is not, considering that both are turnover taxes?

One major difference between business tax and VAT is that business tax is included in the price of product, but VAT is on top of the price of product.

Let’s see an example.

If I order food at a restaurant and pay 100USD for the dishes, the restaurant needs to pay business tax on that money. Let’s say the business tax rate comes at 5%. I will not pay 105USD because of the 5% business tax, meaning that the restaurant’s take-home revenue of my 100USD is 95USD.The business tax is included in the price, borne by the restaurant (seller).

In certain countries, you will encounter situations where you will see the extra tax amount on top of your standard meal prices. However, those taxes are NOT business taxes; they are a form of consumption tax.

But VAT is different.

For example, if I go to buy a computer, there will be VAT incurred for this transaction. Before applying the VAT, the computer price might be 1,000USD. After applying the VAT, the price comes up to 1,170USD because of a 17% value-added tax. So if I only pay 1,000USD, the seller won’t give me the computer. I will have to pay 1,170USD so the transaction can come through.

For this transaction, who paid for the 170USD VAT?

The consumer.

The second major difference between business tax and VAT is that business tax is borne by the business, i.e. the seller, but VAT is borne by the customer, i.e. the buyer.

Now you should understand why VAT cannot be found on the Income Statement.

Because the company pays for Business Tax, but consumers pay for Value-added Tax, the VAT on consumers shouldn’t be a company’s cost. That’s why we cannot find VAT on the Income Statement.

In practice, we as consumers don’t go to the tax bureaus every day to pay VAT on everything we’ve purchased. Instead, we give the VAT to the seller, and the seller will periodically pay the VAT withheld to the tax bureau. From the seller, i.e. the business’s perspective, that VAT should never be accounted for revenue. On the other hand, since the VAT belongs to the tax bureau, but just temporarily sits in the business’s bank account, it’s actually a liability owed by the business to the tax bureau.

For this reason, we actually can find VAT on the Balance Sheet, under the Liabilities section. It’s called tax payable.

After this tax item, we see three expense items: operating expenses, administration expenses and financial expenses. These three items are what we usually call period expenses.

Operating Expenses

What is operation?

For a manufacturing company, its operations are manufacturing and sales. So what are operating expenses?

Operating expenses are related to the company’s operations, i.e. advertisement costs, transportation expenses, warehouse fees, etc.

Expenses of different departments could fit in the operating expenses. For example, cost of promotions, salary of sales people, and various marketing expenses make up the operating expenses of sales departments. Another example would be company stores if the company has retail spaces. If the stores are leased, the rent paid out is operating cost. If the stores are owned by the company, the depreciation counts as operating cost as well.

Administration Expenses

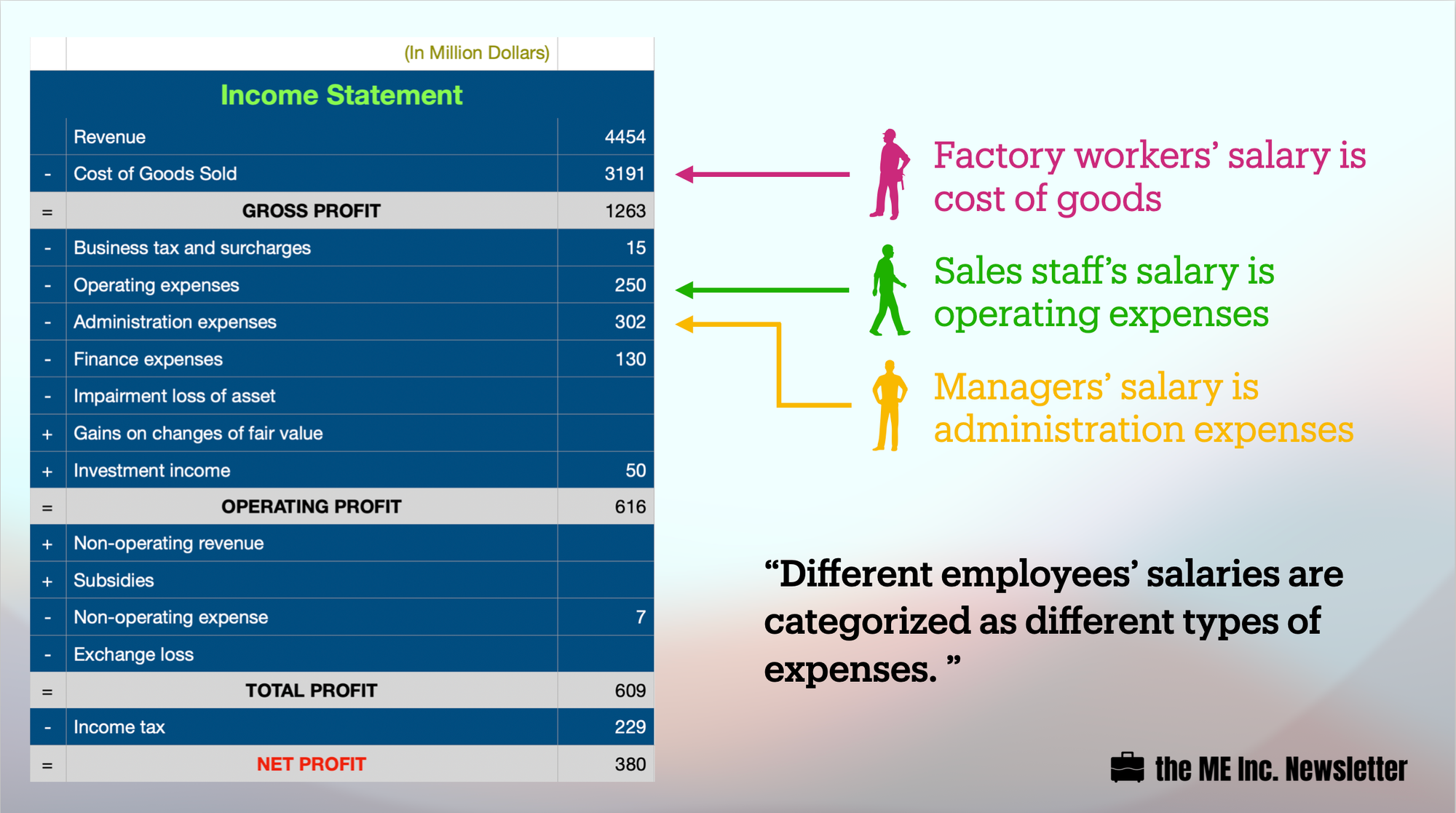

Everything related to the management of the company is Administration Expenses. For example, the salaries of managers, administrative expenditures and depreciation on office building, etc., are all administration expenses.

One thing you might have already noticed is that different employee salaries are categorized as different types of expenses. For example, salaries of marketing and sales employees are operating expenses, but salaries of managers are administration expenses.

But what about wages of workers (in the context of a manufacturing company)? Where should this item fit in? Workers wages are direct manufacturing costs, so it should be put directly in costs of goods sold.

Depreciation of fixed assets should also be recorded in costs of goods sold, since fixed assets are directly used for producing the company’s goods. If the purpose of different fixed assets is different, the depreciation will go to a different category. For example, the depreciation of the stores is a sale expense, or operating expense, while that of an office building is an administration expenses.

Financial Expenses

Financial expenses are pretty straightforward; they are basically interests. Whether the interests you owe to the bank when you borrow, or the interests you earn from deposit savings from the bank. Since we are recording expenses, the former will be positive, i.e. money going out, and the latter will be negative, i.e. money coming in. In other words, when you are paying interests to banks, interest expenses are positive; when you are earning interests from banks, interest earnings are negative.

💡

Rare instances when financial expenses are negative Say a company has raised a large amount of money from investors, and they are not going to spend all of the money immediately. The money left in the bank will generate interest revenue. What if the money is raised by selling stocks?

The company may have already paid off most of its debt, so there is little interests to be paid out. In this case, the interest expenses may become negative. In other words, the company is actually making money from money.

You may not always find three expenses in your Income Statement. In some countries, operating expenses and administration expenses may be combined as one item on the income statement.

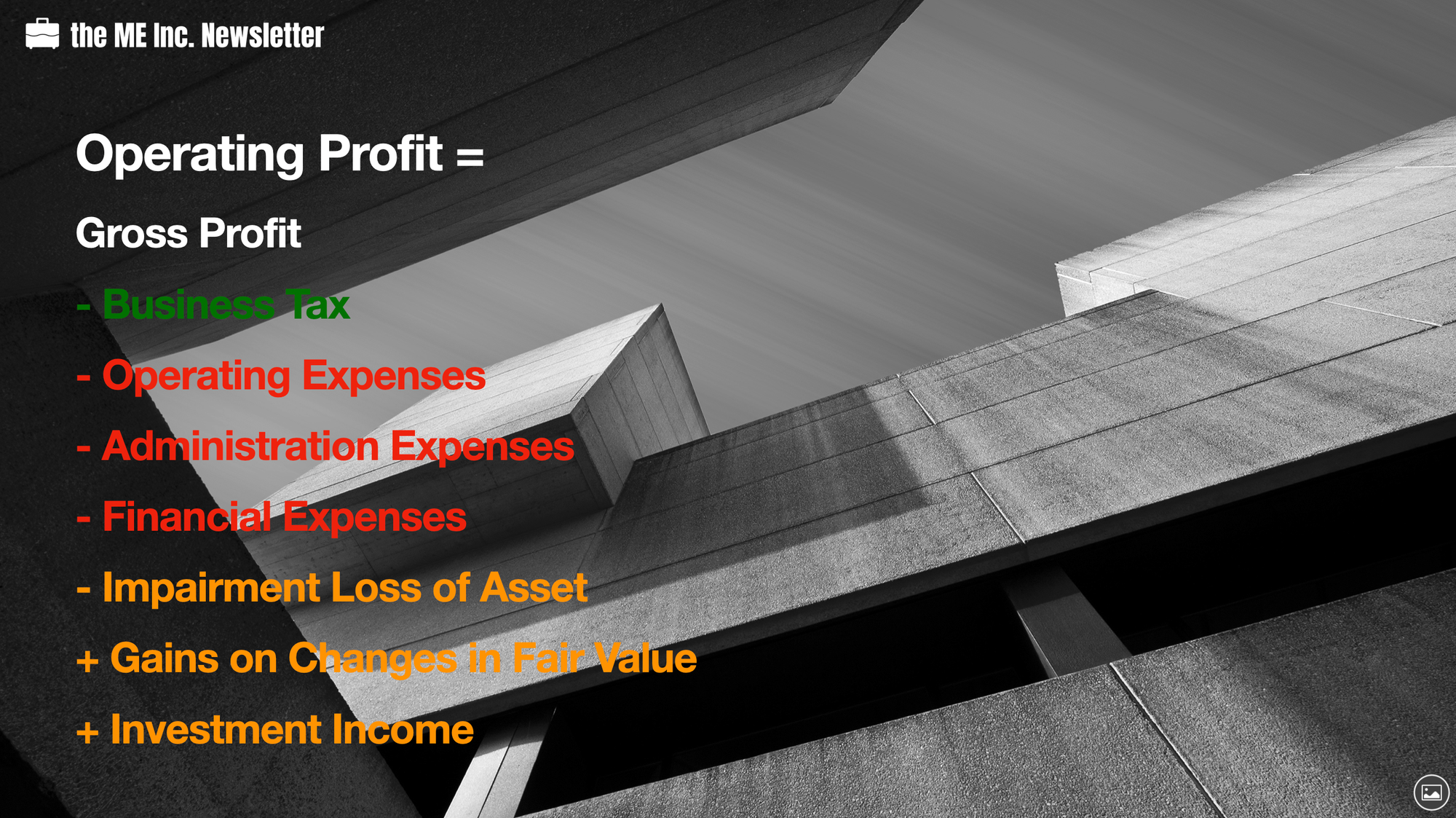

Recall that at the beginning we said that revenue minus costs of goods sold is equal to gross profit. Then we subtract the business tax and surcharges and the three expenses from gross profit, further closing in on our profit from operating the business.

However, between financial expenses and operating profit, there are still three items left, which are impairment loss of asset, gains on changes in the fair value, and investment income.

Investment Income

For small companies that haven’t made any external investments, there will be minimal need to worry about investment income. But let’s say my company has a subsidiary company, and the latter gives me a dividend. This dividend is my income from investment.

Investment is a special form of operating business, so we still consider it part as part of operating profit.

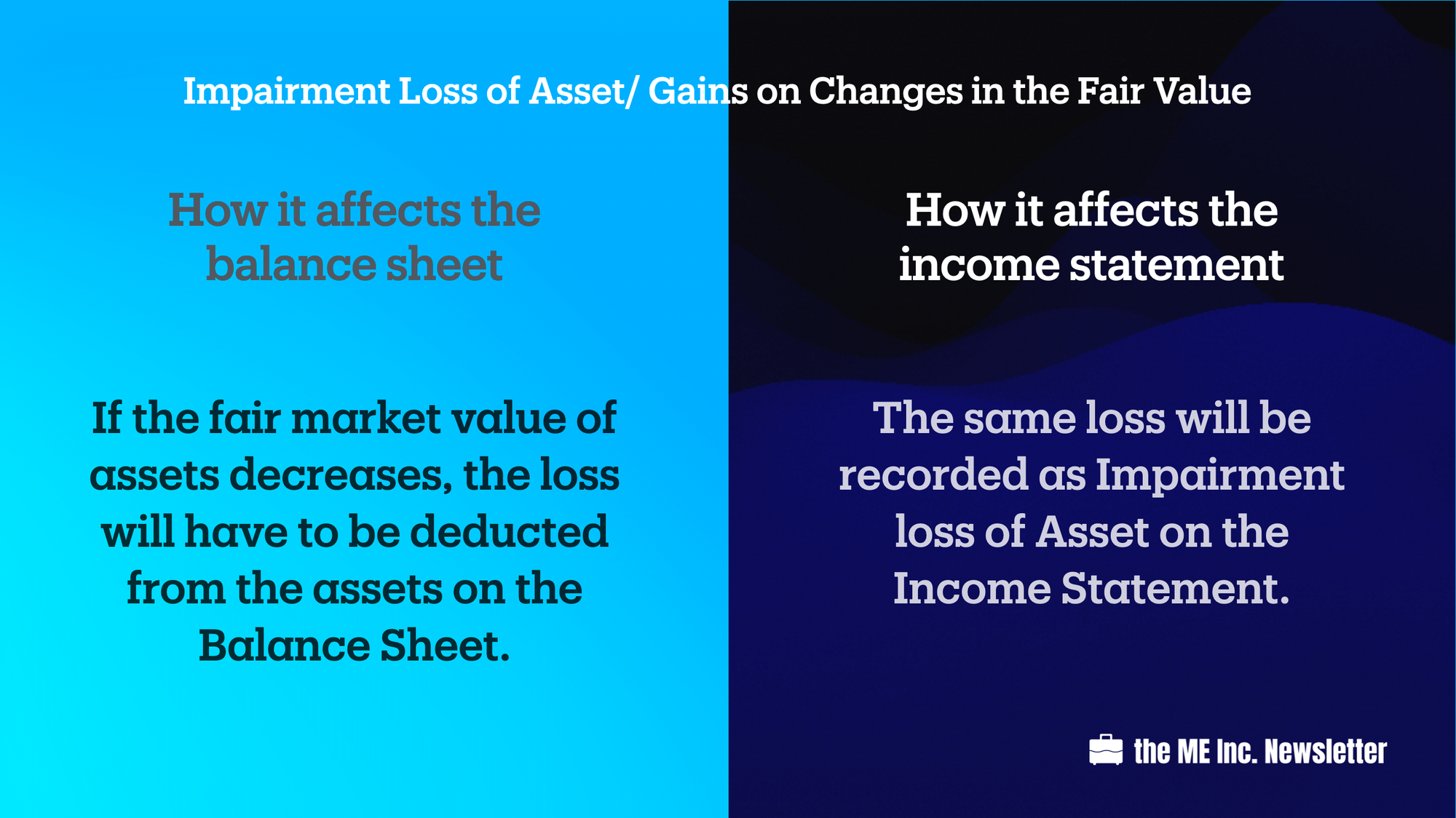

Impairment Loss of Asset/ Gains on Changes in the Fair Value

If you recall in assets valuation on the balance sheet, most assets are recorded with their historical costs, but financial investments and real estate investments are marked to market with their fair values. If the fair market value of any of the former two types of assets decreases, we will need to recognize the loss on the balance sheet.

To make matters worse, it also affects the company’s profits on the income statement.

💡

Let’s say on December 31 each year, we will need to check the fair values of our financial investment and real estate investments. By checking the market prices, we should be able to arrive at updated fair values of our assets.

If the asset price was 10USD last year and 15USD this year, I will get a 5USD gain. If it was 10USD last year and 5USD this year, I will get a 5USD loss. The new value of assets should be updated on the balance sheet, and the change (gain or loss) should be updated on the income statement.

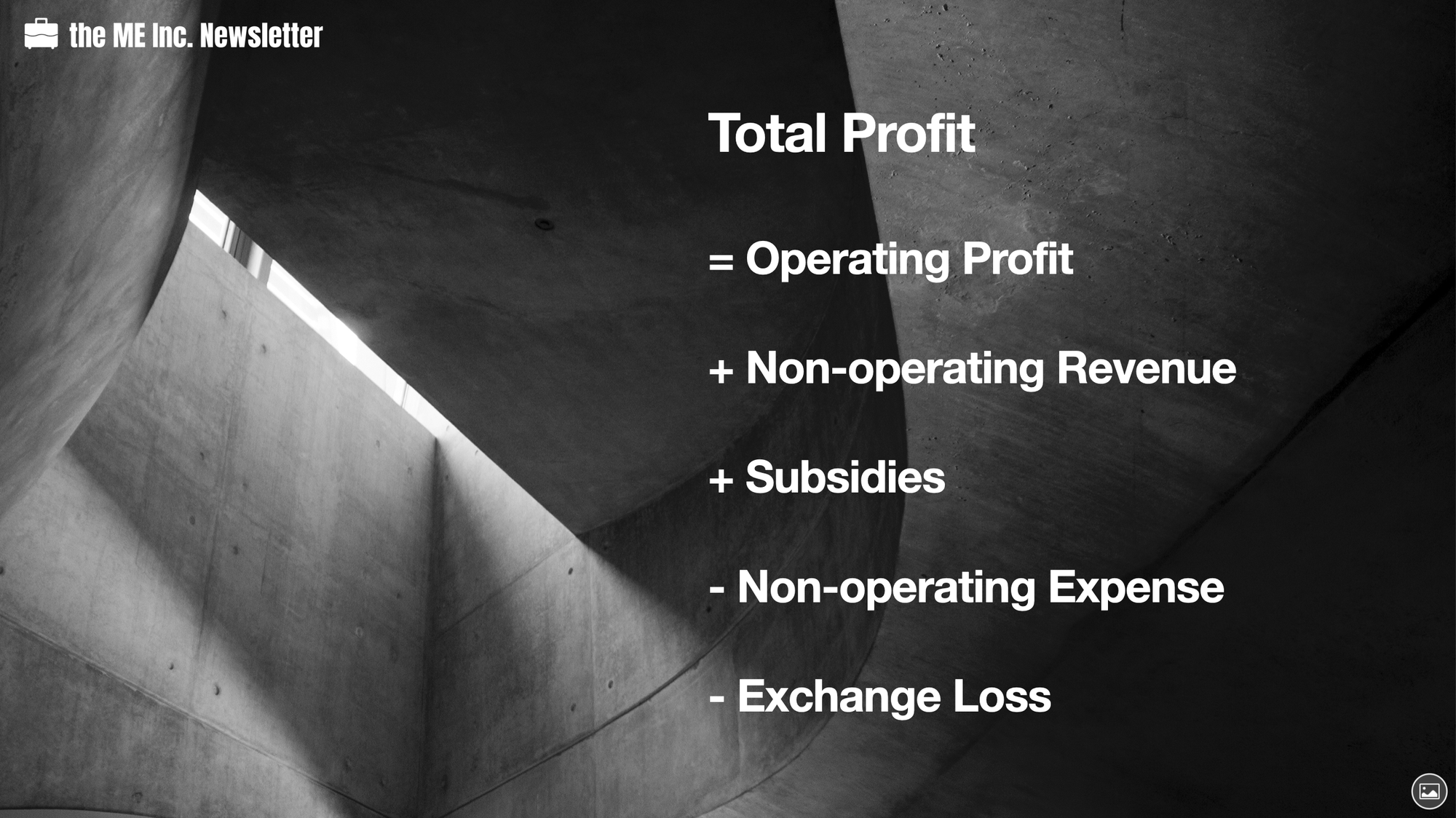

So far, we have subtracted the costs of goods sold from our revenue. We then paid the business tax and surcharges, as well as the operating, administrative, and financial expenses. After that we looked at our gain/loss from our investments and dividends generated from them. What’s left is our Operating Profit.

Non-operating Profit

The two items below Operating Profit are non-operating revenue and non-operating expenses. Let’s look at non-operating revenue first.

Non-operating Revenue

What is a non-operating revenue? The straightforward answer is any revenue generated from non-operating activities.

Let’s look at an example first.

A company checks its inventory and finds the actual inventory exceeds that on the books. This is called Excess Inventory. In this case, the excess inventory is a form of non-operating revenue.

Another example is when a company sells its fixed assets.

We know that the goal of a business is to sell products to earn profits. Its fixed assets are required to produce products. However, there might be instances when the company decides to sell part of its fixed assets on an ad-hoc basis, and when it does, the sale will generate a large sum of money. This will also be recorded as a form of non-operating revenue.

Non-operating Expenses

We just talked about excess inventory as a form of non-operating revenue. Similarly, when we check our inventory but it turns out our inventory is less than what we’ve recorded on our balance sheet, we say there is a shortage on inventory, which is a form of non-operating expenses.

Things like losses caused by accidents such as natural disasters, i.e. fire, flood, etc., are also non-operating expenses.

Why do we list Non-operating Revenues and Expenses separately?

Let’s look at what non-operating revenues and non-operating expenses have in common. They are both unrelated to the company’s operating activities. These activities happen by chance and don’t have continuity in the company’s plans.

What’s the benefit of listing non-operating revenues and expenses separately? Let’s look at this example.

Assuming that I have two companies. Both companies have a profit of 10 million dollars. For the first company, 9 million is operating profit and 1 million is non-operating profit. For the second company, 1 million is operating profit and 9 million is non-operating profit.

Which company would you like to invest?

For me, it is a no-brainer. I definitely will invest in the first company, even though both companies make the same amount of profit.

The reason is simple. I believe the first company will make at least the same amount of money the next year, but I highly doubt that the second company will manage to do the same.

Why?

Because the most profit the second company generates is from non-operating activities, i.e. projects that are not continuous.

This is the benefit of listing operating profit and non-operating profit separately. It not only tells you how much profit the company makes this year, but also provides information on whether the profit is dependable. In this way, we will be able to predict the company’s future profitability based on this year’s income statement.

Subsidies and Exchange Gain and Loss

In some countries, companies might be able to receive government subsidies for participating in certain economic activities as a way to boost investment in certain industries. These subsidies are also a kind of non-operating revenue. However, they should be listed separately, and we call it subsidies. Subsidies should also be recorded in the non-operating profit and loss section.

Some companies might operate in multiple countries, so they might receive payment in one currency but pay suppliers in another. However, currency exchange rates change every day, and when they do, my profits may suffer a loss or post a gain. This is called exchange gain (or loss). Exchange gain (or loss) should also go in the non-operating profit and loss section.

Getting Close to Our Actual Profit!

Total Profit

By subtracting our non-operating expenses and adding our non-operating revenues onto the operating profit, we have arrived at our Total Profit. Remember: subsidies and exchange gains or losses should also be taken account in the non-operating profit.

Net Profit

Now we’ve come to the final part. We have made some profit from the operations of the business, and have paid out our non-operating losses. After that, we still have quite some (total) profits.

Now there is still one thing left: income tax.

Depending on your country and industry, etc., business income taxes can range from 15% to 25%, or even more. For example, China has a business income tax of 25%, but can go as low as 15% for tech companies.

At this point, most people like me would assume that 75% of the total profit will be our net profit.

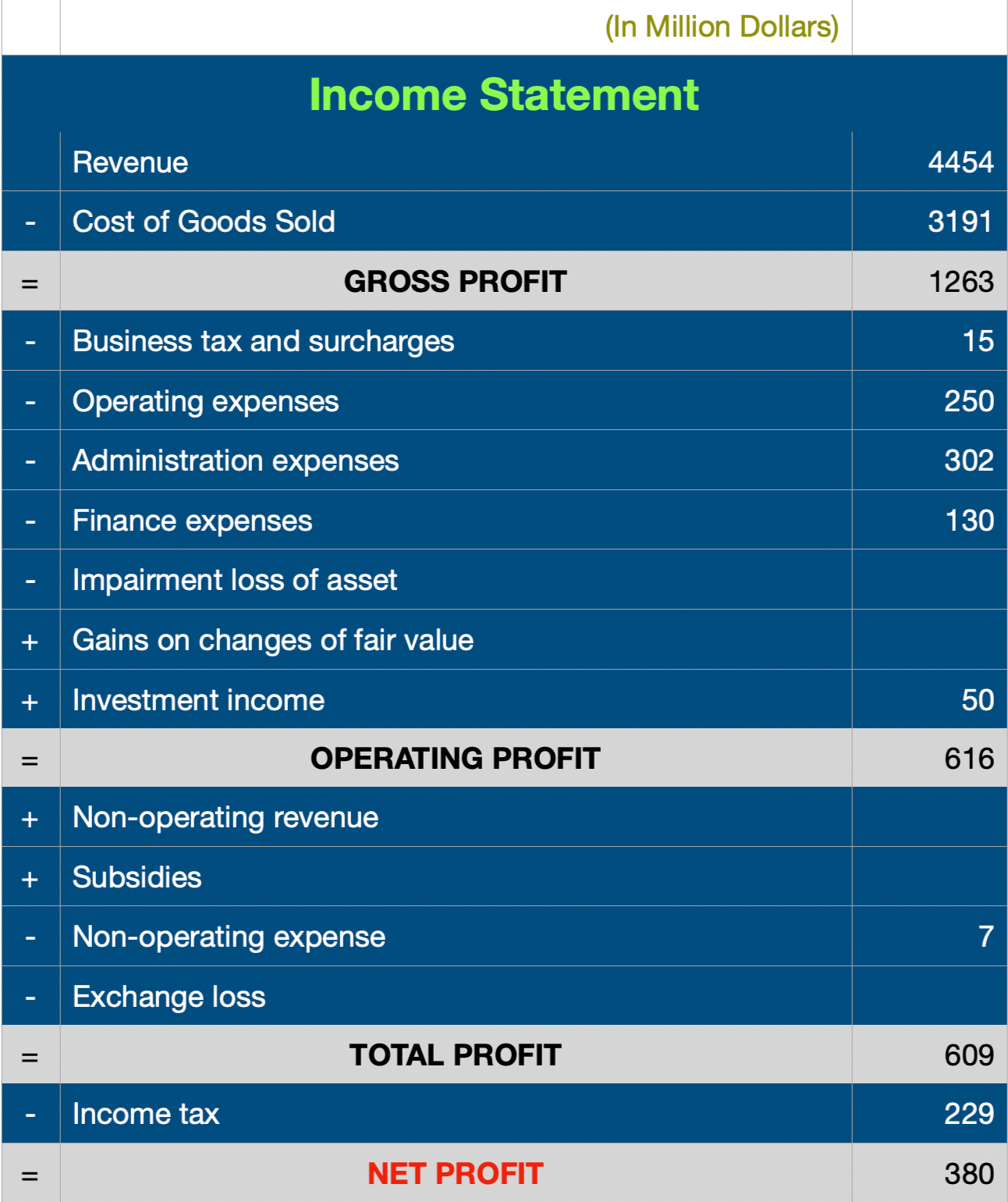

However, this is not the case. Let’s look at our Income Statement again.

Apparently, the net profit(380) is less than 75% of the total profit(609 times 75%=456.75). In other words, the company paid more taxes. But why?

To understand this, we first need to know where the 25% business income tax has been applied. Should it be applied to the Total Profit?

The answer is no. Actually the company will need to pay 25% of its taxable income to the tax bureau as its income tax.

Unlike total profit, which is calculated based on the accounting standards, taxable income is calculated based on the tax law. That is why our total profit is different from our taxable income. Here’s an example.

Let’s say our company buys some advertisement, which is a form of operating expenses. According to accounting standard, we should be able to record the ad costs on the Income Statement, regardless of how much we’ve spent. However, the tax law actually stipulates that if a company’s advertising costs exceed a certain percentage of revenue, the exceeding portion cannot be deducted from its taxes.

If we assume that this percentage cap is 2% and our company’s revenue is 100 million, our tax-deductible portion will be 2 million. However, we actually spent 20 million on advertising. So even though all 20 million should be recorded as operating expenses, we actually will have to pay income tax on 18 million of those advertising costs. The taxable income now exceeds total profit by 18 million.

This is what the income statement is all about. So what kinds of information does an income statement tell us from an economic perspective? We will go over it in our next post.